Mariana Mazzucato, is there no beginning to her knowledge of economics?

It is, of course, becoming increasingly irritating to see Mariana Mazzucato being lauded for her stunning finding that the only reason we have nice things is because of government. Especially when one considers that this finding came from a research program funded by government. Biting the hand that feeds is really very terrible economics after all. The latest irritant is this, in her acceptance speech for an award:

The point is not to belittle the work of Jobs and his team, which was both essential and transformational. But we must be more balanced in the historiography of Apple and its founders, where not a word is mentioned of the collective effort behind Silicon Valley. The question is this: who benefits from such a narrow description of the wealth-creation process in the hi-tech sector today?

...

If policymakers want to get serious about tackling inequality, they need to rethink not only areas such as the wealth tax that Thomas Piketty is calling for but the received wisdom on how to generate value and wealth creation in the first place. When we have a narrow theory of who creates value and wealth, we allow a greater share of that value to be captured by a small group of actors who call themselves wealth creators. This is our current predicament and the reason why progressive parties on both sides of the Atlantic are struggling to provide a clear story of what has gone wrong in recent decades and what to do about it.

She seems entirely unaware of the basic paper on this subject. Those "wealth creators", those "entrepreneurs", how much do they get from their innovations?

The present study examines the importance of Schumpeterian profits in the United States economy. Schumpeterian profits are defined as those profits that arise when firms are able to appropriate the returns from innovative activity. We first show the underlying equations for Schumpeterian profits. We then estimate the value of these profits for the non-farm business economy. We conclude that only a minuscule fraction of the social returns from technological advances over the 1948-2001 period was captured by producers, indicating that most of the benefits of technological change are passed on to consumers rather than captured by producers.

The answer is a little under 3% of the total value created by the innovations. Almost all of the rest ends up as consumer surplus being enjoyed by the great unwashed citizenry out there. Which is great, as it should be perhaps, the aim and point of this whole having an economy game is to make the average Smith and Jones as rich as they can possibly be without bursting with the pleasure of it all.

The complaint is that Professor Mazzucato seems to be entirely ignorant of all of this. Sure, Steve Jobs ended up with a pile of money that Scrooge McDuck would blush to surf down. But we don't actually care because Jobs ended up with a trivial amount of the value created. It is quite seriously being said that another 10% of the people in a developing country with a smartphone adds 0.5% to GDP growth (and no, not 0.5% of extant growth, an entire 0.5% of GDP more) in said developing economy. Whether Jobs ended up with $5 or $50 billion for sparking that amount of value creation is an entire irrelevance compared to that value creation.

And no, we don't insist that Jobs "earned it", nor "deserved it". It's a purely utilitarian calculation. If someone who innovates (for Mazzucato would insist Apple and Jobs did not "invent") something that adds entire percentage points of growth to the developing economies of the world then gets to have hot and cold running private jets for the rest of his life, well, that's just fine. Because we think that would be a pretty good incentive for the next person who is going to make the poor of the world richer to buckle down and get on with it.

The first point of economics is that incentives matter. So it would appear that there is no beginning to Professor Mazzucato's understanding of the subject.

Challenging Shapiro on involuntary unemployment

A particularly famous efficiency-wages model was the one devised by Shapiro & Stiglitz (1984) - a ‘shirking’ model. The main assumption is that there is imperfect, asymmetric information and that workers have a choice to work or ‘shirk’ (exert little or no effort) and that there is a probability that employers catch them and that they don’t catch them. From this simple assumption, Shapiro & Stiglitz conclude that the wage-rate paid in the market will be an efficiency-wage that is higher than the market-clearing wage. The model predicts that there will necessarily be involuntary unemployment in equilibrium which supposedly acts as a ‘worker discipline device’ since it discourages workers from shirking because their being fired would mean that there is a possibility that they may not find another job. For those who are interested in a graphical representation, the graph below depicts the Aggregate Labour Demand (ALD) curve, the Aggregate Labour Supply curve (ALS – which also presumes a competitive labour supply), the Non-Shirking Condition (NSC) and the Efficiency Wage (EW) at equilibrium. Several of the underlying assumptions can be challenged, however. For example, since the state of technology enters the Aggregate Labour Demand relation and the state of technology is not static but it actually improves over time, when we take a dynamic view of the Shapiro-Stiglitz model, we find that the positive technology shocks consistently shift the ALD curve outward.

Furthermore, Shapiro & Stiglitz make a simplifying assumption that the worker believes the likelihood of finding another job (if fired) is equivalent to the proportion of unemployed people – this simplification means that, at the limit of full employment, the Non-Shirking Condition (NSC) cannot intersect with the Aggregate Labour Supply (ALS) – this means that full employment is a theoretical impossibility. In reality, however, people have individualised estimates with respect to how likely they are to get another job if they are fired (based, for example, on their estimation of their own ability, how well their skills match to vacancies and other variables) – this more realistic assumption makes full employment possible.

Remember, how the Aggregate Labour Demand curve experienced constant positive technology shocks over time? Well, this subsequently means that there would be full employment since the NSC and the ALD would intersect at or beyond the ALS curve as time progressed. However, the outcome of full employment here presumes static population growth. In reality, the population changes over time (generally, the ALS might shift right over time to signify an increase in the population over time) and, because of this, the conclusion of the model becomes ambiguous.

Simplified models yield nice conclusions whilst more complex models yield ambiguous results. With Shapiro & Stiglitz’s initially realistic assumption, one may have thought that involuntary unemployment was going to be an inevitable labour market outcome even in a competitive labour market. However, when relaxing the accompanying unrealistic assumptions, it’s not so straightforward.

Bankers earn more than medics: what can we do?!

A common criticism leveled against the financial services industry concerns their remuneration compared to those from more ‘noble’ professions – such as Medical Doctors. Proclamations such as “it’s ridiculous that the average Doctor earns less than the average investment banker” are not unusual to hear in common parlance; Doctors cure ailments and save lives whereas Investment Bankers supposedly wreck households and exploit taxpayers. It is, therefore, unfair that Bankers are paid more than Doctors. The oft-proposed solution is heavier taxation and regulation on Investment Banks. However, these critics conveniently forget the other side of the coin – the inadequate remuneration for noble professions. Increased taxation and regulation on Investment Banks does nothing to address the inadequate gratitude expressed to them (which these same critics seem to implicitly believe is measured purely by financial compensation).

For Doctors to be remunerated fairly, we need only look at the USA to find that, on that side of the Atlantic, it’s Medics (Anaesthetists, Gynaecologists, General Practitioners etc.) who dominate lists of the most highly paid professions. Their average pay in the USA is higher and their hours worked less than average Investment Bankers. Freer markets ensure fairer, more just remuneration.

Nursing and teaching are also considered noble professions (though they are often undervalued, and wrongly so, relative to Doctors). Fair remuneration and freedom with which they can care and teach in an appropriate, effective and efficient way is only viable in a mostly (if not, completely) free market.

In Higher Education, the phenomenally high research activity of US Universities is unrivalled. This can be attributed to the flourishing mix of private alternatives, the relatively generous remuneration of Professors and the abundance of private funding opportunities available for academic pursuits.

One might argue that healthcare and education must be universally accessible and it would greatly harm society if we repealed the public healthcare available via the NHS. However, a pragmatic compromise would be issuing healthcare vouchers so that individuals are given the money that they can spend freely on their own healthcare. In this way, the public can choose between public and private alternatives with their vouchers.

Free markets lead to an improvement in welfare for all those involved by providing the consumers with more choice (whether they be patients or students) and higher quality products through competitive mechanisms whilst ensuring the fair remuneration of producers - whether they are medical professionals or involved in education.

Maybe Keynes was right after all?

It has to be said that we're not great fans of macroeconomics around here. Not enough good data from enough different places to definitively answer most questions: and that's before we get onto Hayek's point about simply not being able to calculate the economy without using the economy itself to do so. However, this makes us think that Keynes might well have been right on one point: It took far too long but Britain’s traumatic national pay cut is coming to an end. Even on the somewhat crude median earnings measure, pay is finally going up again, even after accounting for the effects of price rises. Wages are rising a little faster and inflation has collapsed, a golden combination for employees across the country.

Ever since the Industrial Revolution and the spread of capitalism, gradually rising wages have been the norm, apart from in wartime and during brief periods of extreme economic dislocation. The fact that this process went into partial reverse over the past few years despite the recovery came as a shock and helped to explain why so many people began to fall out of love with capitalism. It is therefore excellent news that normality is finally re-establishing itself.

One view of unemployment is simply that it happens when labour is more expensive than people are willing to pay for it. That's obvious in that one sense of course. The question becomes then well, how quickly will the repricing happen if we do ever get to that stage? There are those who insist that it happens immediately and thus unemployment and recessions cannot happen. Not an entirely convincing view. There are also those who insist that it can take forever and this justifies all sorts of interventions. And then we've got the evidence of the past few years.

It could be argued that labour in the UK did become too expensive. We had just had the largest and longest peacetime expansion of the economy after all. So, a repricing was necessary. And this is where Keynes could be said to be correct. It takes time because nominal wages are sticky downwards. People really, really, don't like lower numbers on their paycheques. They'll grumble about their real wages falling if it's disguised with a little bit of inflation but they'll riot if the equivalent fall were at a steady price level.

We don't say that the past few years prove it: only that what evidence we have is consistent with this explanation. And, given the paucity of our evidence base, that's probably the best we can do.

As we've been saying, there isn't really a gender pay gap

But there is a motherhood pay gap. Interesting research:

Studies from countries with laws against discrimination on the basis of sexual orientation suggest that gay and lesbian employees report more incidents of harassment and are more likely to report experiencing unfair treatment in the labor market than are heterosexual employees. Gay men are found to earn less than comparably skilled and experienced heterosexual men. For lesbians, the patterns are ambiguous: in some countries they have been found to earn less than their heterosexual counterparts, while in others they earn the same or more.

The results for the UK are that gay men earn less than hetero, lesbians more than hetero women. In fact, lesbians earn around what men do and gay men earn around what hetero women do.

We could, as this report does, speculate about societal standards, the idea that lesbian women have, in some manner, "male traits" which lead to that higher pay.

A much simpler observation of the evidence would be the influence of children. We know that fathers earn more than non-fathers among hetero men (yes, even after adjusting for age and education etc). Also that mothers earn less than non-mothers. Gay men tend not to be fathers (this is not being categorical of course, "tend") as lesbians tend not to be mothers.

If the so-called gender pay gap were simply the influence of children upon earning patterns, as we largely think it is, then we would expect to see what we do see when looking at the earnings of non-hetero society. This does not prove we are correct of course, but it is supportive of our view.

Free movement and discrimination: the case of football

The more you open markets up, the less discrimination you get on grounds of 'taste' (racism). The stuff left over is usually 'statistical' (i.e. where certain groups are different in their average levels of job-relevant criteria). There was already a great paper showing this for the Fantasy Premier League (which I play avidly), but now there's also one for the real Premiership! Pierre Deschamps and José de Sousa look at the impact of the 1995 Bosman Ruling on the gap between black and white footballer wages in the English league. They find that when only 20 clubs competed for their skills, black players were underpaid relative to white ones, indicating that owners were able to indulge their preference against non-whites (or indulge their fans' preferences).

But once the whole of Europe were effectively on an equal footing, blacks became highly mobile and garnered equal pay for their efforts:

This paper assesses the impact of labor mobility on racial discrimination. We present an equilibrium search model that reveals an inverted U-shaped relationship between labor mobility and race-based wage differentials. We explore this relationship empirically with an exogenous mobility shock on the European soccer labor market. The Bosman ruling by the European Court of Justice in 1995 lifted restrictions on soccer player mobility.

Using a panel of all clubs in the English first division from 1981 to 2008, we compare the pre- and post-Bosman ruling market to identify the causal effect of intensified mobility on race-based wage differentials. Consistent with a taste-based explanation, we find evidence that increasing labor market mobility decreases racial discrimination.

The figure below shows how the 'turnover' (i.e. churn between clubs) of black English players jumped when European markets opened up. Market freedoms; exit; a sort of 'voting with their feet', outperformed voice in bringing equality. And we know from ASI research that this did not harm the English national team.

This is in line with a lot of what we have been saying recently—markets are a good way to bring about justice!

People respond to incentives

That people respond to incentives is an obvious point but I feel like every reiteration is worth it. One of the clearest examples of where people respond strongly to incentives is retirement. If you raise the retirement age, many people who'd otherwise be eligible continue to work. Since retirement probably increases life satisfaction/happiness and perhaps even health we obviously want it to happen at some point, but since it's also very costly in terms of benefits paid and productive activity not done, we want to be mindful of both costs and benefits.

A new paper in The Review of Economics and Statistics by Kadir Atalay and Garry F. Barrett at the University of Sydney adds to a large literature:

Governments around the world are reforming their social security systems in light of the challenges posed by population aging. We study the 1993 Australian Age Pension reform, which progressively increased the eligibility age for women from 60 to 65 years. We find economically significant responses to the reform. An increase in the eligibility age of one year induced a decline in the probability of retirement by 12 to 19 percentage points. In addition, the reform induced significant program substitution, with increases in enrollment in other social insurance programs, particularly the disability support pension, which effectively functioned as an alternative source of retirement income.

Raising the retirement age for women led to lots more of them working, but also more of them claiming other benefits.

Every single paper I've ever seen on the topic has found a similar result. For example in the UK raising the pension age from 60 to 61 led to 7.3pp more women in employment at age 60 (separate paper with more evidence). In Spain, people with worse health were more responsive to financial incentives. Less generous pension payouts in France (normal retirement rather than disability insurance retirement) meant 14% higher total work hours, on average, between the ages of 55 and 64. Another paper found that pensioners respond to incentives in a different way: if they stand to gain more by waiting before they claim then they are more likely to wait.

The point of all this is not to say that we should pack the elderly off to the workhouse until they're 90, but more to note that incentives matter, against the common claims that the homo economicus model is rarely or never a good approximation for real humans.

The income inequality obsession

There is undoubtedly a persisting obsession with income inequality, whether this comes from the likes of Thomas Piketty or Russell Brand (whom Kate Andrews very recently wrote an article on), this obsession is unhealthy and, actually, upon closer scrutiny, counter-productive. The focus on income inequality places emphasis on income being the most important component of inequality. Income, however, is only useful as a means to an end, rather than as an end in itself. It is a way of measuring and attaining a form of freedom in modern society. It derives its value from affording the individual who possesses it with capabilities. Ludwig von Mises wrote in a Theory of Money and Credit that money is money by virtue of the fact that it is a medium of exchange (rather than it being legal tender or a store of value, for example).

The obsession with relative income rather than focusing on advancing one’s own, absolute capabilities (and/or others’, for that matter) helps perpetuate the frictions of class differences (the income component of them, at least). Income, whether absolute or relative, is not an end-in-itself for the vast majority of people.

Delving more deeply into the real value of money, we find that freedom and the inequality of freedoms enjoyed by people is at the real heart of the problem. Those who obsess over income inequality shy away from addressing the legally imposed inequality of freedom; the right to use one’s labouring capacity as one sees fit, to spend one’s time as and when they want and for the price they will, the right to interact with our fellows to our mutual advantage without third-party interference, the right to speak freely, think freely and live freely – don’t these legal iniquities require more urgent addressing?

The focus on income inequality is the smoke and mirrors of well-intentioned rhetoric. The focus on wealth redistribution rather than the opportunity to engage freely in wealth creation, on compulsory, ever-more rigid education instead of free thought, on dividing society according to income instead of encouraging social cohesion… this focus provides supposed justification for the legal privileging and normative elevation of income pursuit and, therefore, enables subtle homogenisation and, ultimately, degradation of peoples’ capacity for free thought. Addressing income inequality through redistributive policies is, as is all too often the case with such proposals, conservatism in the guise of social liberalism.

A miracle cure for central bank impotence

Are central banks ever unable to create inflation? The question may seem absurd – why would we ever want them to create more inflation? The typical answer is that deflation can be a lot worse than inflation. But this ignores the fact that prices can fall simply because we can produce things more cheaply. Falling oil prices mean cheaper production, which should mean cheaper consumer products. That's 'good' deflation.

But 'bad' deflation, caused by tight money, can be very harmful, and indeed is what Milton Friedman blamed the Great Depression on. A variant of this view, which looks at market expectations, blames expectations of deflation for the crisis in 2008. Those of us who think that nominal GDP is what matters – since contracts and wages are set in nominal terms – recognise that deflation can knock NGDP off-course and cause widespread bankruptcies and unemployment that would not have taken place in a more stable macroeconomic environment. (Free banking, say.)

So if inflation is sometimes desirable, when it prevents deflation (or collapses in NGDP), the power of the central bank to create it really does matter. That's where Paul Krugman and the Telegraph's Ambrose Evans-Pritchard have clashed. In response to Krugman's claim that central banks are impotent when their interest rates are zero, Evans-Pritchard writes:

Central banks can always create inflation if they try hard enough. As Milton Friedman said, they can print bundles of notes and drop from them helicopters. The modern variant might be a $100,000 electronic transfer into the bank account of every citizen. That would most assuredly create inflation.

I don’t see how Prof Krugman can refute this, though I suspect that he will deftly change the goal posts by stating that this is not monetary policy. To anticipate this counter-attack, let me state in advance that the English language does not belong to him. It is monetary policy. It is certainly not interest rate policy.

The piece is worth reading in full. I'm less convinced that 'helicopter drops' are actually needed now – if central banks said that they'd do as much conventional QE as it took to raise the inflation rate or NGDP level to x%, that may well be enough. But Evans-Pritchard's basic point that central banks are never 'out of ammo' is what counts.

Maybe we should like patents

For a long time I was very sceptical of the benefits of patents. For one thing, they seemed to interfere with other types of property—Apple's patents over certain shapes for phones mean Google cannot use its factories, materials, etc. in certain ways. For another, I coincidentally had come across work suggesting their benefits are overstated, including Against Intellectual Monopoly (appropriately available in full online) by Michele Boldrin and David K. Levine.

But three recent papers exploiting a novel source of data have made me reconsider, since they throw cold water on one of the popular alternatives to patents: innovation prizes. All three are by B. Zorina Khan, an economics Professor at Bowdoin College and fellow at Stanford University's august Hoover Institution.

The first looks at annual industrial fairs in 19th century Massachusetts and finds that (relative to patents awarded over the same period) prizes were mainly used for advertising purposes, were awarded unsystematically and unpredictably, and did not vary in line with how useful or popular an invention or innovation ended up being. What's more, prizewinners were typically from a more privileged class than patentees. This all implies that patents are more market driven and better at incentivising creative innovation, Khan says.

The second looks at similar data (American Institute of New York annual fairs) from a different angle. One argument against patents is that they limit what others can do on top of a given innovation, or how much they can be inspired by a particular breakthrough, because they might have to license the patent or risk infringing it. One argument in the other direction is that patents allow people to bring their information out into the open because others will not use it to jump ahead, so it encourages openness. What's more, all of their info surrounding the innovation is written down and easy to find.

Khan finds that the second effect predominates; patents encourage 'spillover' innovation more than prizes:

In keeping with the contract theory of patents, the procedure identifies high and statistically significant spatial autocorrelation in the sample of inventions that were patented, indicating the prevalence of geographical spillovers. By contrast, prize innovations were much less likely to be spatially dependent. The second part of the paper investigates whether unpatented innovations in a county were affected by patenting in contiguous or adjacent counties, and the analysis indicates that such spatial effects were large and significant. These results are consistent with the argument that patents enhance the diffusion of information for both patented and unpatented innovations, whereas prizes are less effective in generating external benefits from knowledge spillovers. I hypothesize that the difference partly owes to the design of patent institutions, which explicitly incorporate mechanisms for systematic recording, access, and dispersion of technical information.

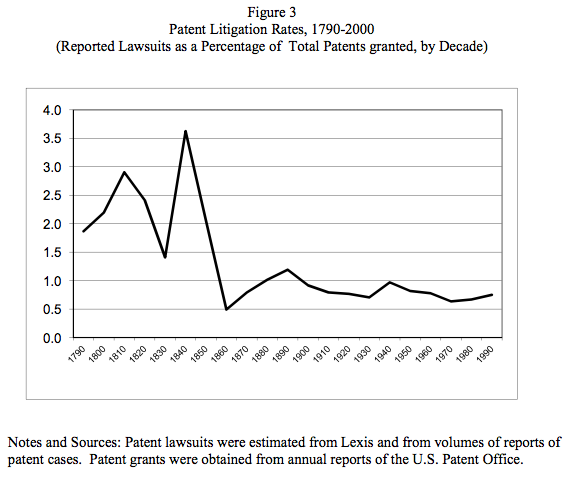

Finally, her 2013 paper “Trolls and Other Patent Inventions: Economic History and the Patent Controversy in the Twenty-First Century” (the argument is given in less length in a Cato Unbound essay) argues that if you take a long historical view, current patent controversies around non-practising entities, patent thickets, litigation and so on are not new. She says they are part of a well-functioning and successful intellectual property system.

So maybe we should like patents. After all, we support regular property rights because the institution has been proven to lead to a wealthy, successful society, even if messed with substantially. If patents are the best tool we have for generating innovation—a key ingredient of continued social progress—then we should support them too.