Isn't Will Hutton's logic here just so lovely?

We'd probably have to invent Will Hutton if he didn't already exist for his logical twists and turns are something of a national wonder to behold. On the subject of FIFA he's noticed that it's not the purest of organisations, not as white as the driven snow:

This is a disgrace. Based in Zurich, Fifa is the governing council of world football, with 209 national member football associations. Yet even though it has global reach, power and income, earning $4.5bn this year from the World Cup alone, it is run with less transparency than a car boot sale. Football, and the world, needs better.

The president is elected by a simple majority of the 209 members. There are no checks and balances; no accountability to a governing board; no transparency over key issues such as pay; no protocols for the publication of reports like those of the former New York district attorney, Michael Garcia. Once elected, the president of Fifa can run the organisation like a tribal chieftain, dispensing favours to seek ongoing support from the tribe’s varying factions and brushing off criticism. His position is unassailable.

Well, yes, OK, perhaps being part of an organisation where not everyone accords with the British notions of fair play and honesty might not be all that wise a decision. Possibly we migfht leave then, or refuse to deal with it until it starts to live up to those values we deem important.

It underlines the larger point: we have to live up to our values and make common cause with those who share them. Yet the Conservative party is gearing up to fight the election on a nativist programme of leaving the European Convention on Human rights (ECHR) and moving ever closer to exiting the European Union.

But we mustn't leave an organisation that doesn't accord with British notions of fair play and honesty. Actually, doesn't even agree with the basic and fundamental underpinning of our system of law (as Lord Woolf so notably pointed out). If Hutton didn't exist we would have to invent him, wouldn't we? Otherwise where would we find our logical equivalent of the Red Queen, where an argument means whatever he says it does rather than that plain and honest meaning.

Getting it entirely wrong on fatcat CEO pay

An interesting little piece of research over at the Harvard Business Review. What do people think the difference between worker and CEO pay is and what do they think it should be? The research is interesting it's just that the conclusions people are likely to draw from it are entirely mistaken. The result won't surprise many:

We’re currently far past the late Peter Drucker’s warning that any CEO-to-worker ratio larger than 20:1 would “increase employee resentment and decrease morale.” Twenty years ago it had already hit 40 to 1, and it was around 400 to 1 at the time of his death in 2005. But this new research makes clear that, one, it’s mindbogglingly difficult for ordinary people to even guess at the actual differences between the top and the bottom; and, two, most are in agreement on what that difference should be.

“The lack of awareness of the gap in CEO to unskilled worker pay — which in the U.S. people estimate to be 30 to 1 but is in fact 350 to 1 — likely reduces citizens’ desire to take action to decrease that gap,” says Norton.

It really shouldn't surprise that an awful lot of people are remarkably ignorant about the world that they inhabit.

The error though is in what is then assumed should be done about it. For of course you can already hear the screams (from people like the High Pay Commission) insisting that as the average voter doesn't want there to be this income disparity therefore there should not be this income disparity. The error being that what the CEO of a large company gets paid is none of the damn business of the average voter.

It's the business of those doing the paying: and if the shareholders in a company wish to pay the person managing their business handsomely then that's entirely up to them. Nothing to do with the jealousy of the mob at all.

There is a small coda: some argue that it's the same old interlocking boards that keep raising the CEO's pay, knowing that their own will get raised in turn. The theory that the managerial class is ripping off the owners, the shareholders. It's true that this could happen, principal/agent theory is true. However, if this were true then private equity would be paying their managers considerably less than public companies do as they would not be subject to this rip off. Given that in reality, out here in the world, private equity pays very much better than public companies do then this isn't true either.

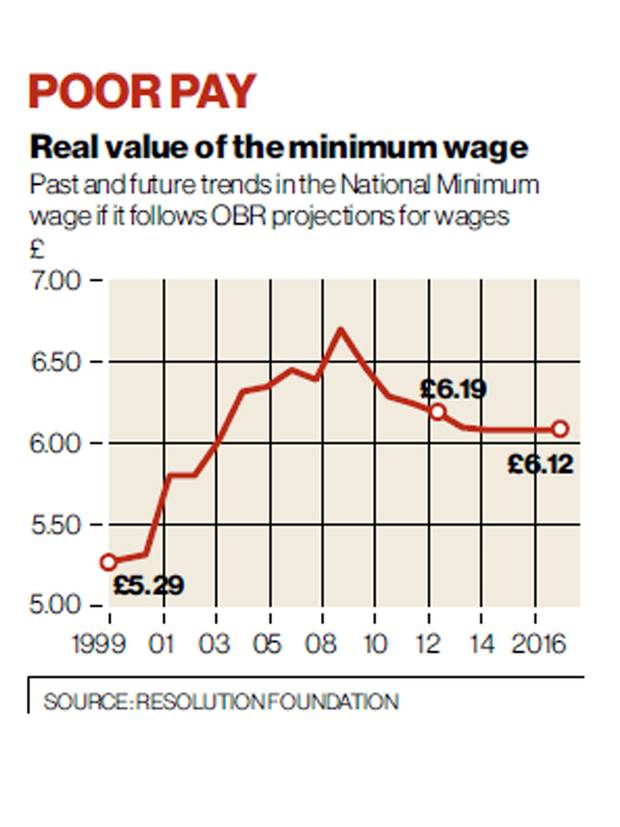

On Unite's demand for a £1.50 rise in the minimum wage

Howard Reed has done this particular piece of pencil sucking research for Unite to back up their demand for a rise in the minimum wage of £1.50 an hour. They're very proud of the fact that this would increase the amount of tax paid. Which doesn't really strike us as being all that good an idea really. Hoovering more money out of the wallets of the lowly paid never does sound like a good idea to us but we assume that things are seen differently over in unionland. But in the report they also say this about the macroeconomic effects:

A £1.50 per hour increase in the National Minimum Wage has three potential multiplier impacts on UK GDP: • The wages impact: the increase in net incomes arising from the increase in gross wages should lead to increased consumer demand which has a positive multiplier impact on GDP. • The profits impact: the reduction in net incomes arising from a decrease in profits may lead to reduced consumer demand which would have a negative multiplier impact on GDP. • The public finances impact: the increase in income tax, expenditure tax and NICs receipts and the reduction in benefit and tax credit spending leads to an improvement in the public finances even after taking into account increases in the public sector wage bill and reductions in corporation tax revenue. This means that government spending does not need to be cut as badly as current plans suggest. If the improvement in the public finances is matched by an increase in government departmental and investment spending – so that the overall government fiscal position is unchanged – then there should be a positive multiplier impact on GDP.

Reed also looks at the number of jobs that will be lost from that rise in the minimum wage and, hey presto, finds that more will be created than lost. He manages this by taking the lowest estimate of unemployment to be created he can find and the highest one for the number of jobs to be created available.

Hmm. Think we'll file this report in the policy based evidence making file, that round one under the desk, shall we?

UKIP is on the right track to beat low pay

In the kick-off to their party conference, UKIP has also announced that its general election manifesto will raise the personal allowance threshold by £3,500 pounds:

At its party conference, which has begun, UKIP will also promise to raise to £13,500 the amount people can earn before paying any income tax.

In a plan to win the "blue-collar vote", Nigel Farage's party will pledge to fund the changes by leaving the EU and cutting UK foreign aid by 85%.”

(At present, the) 40p rate is payable on income from £41,866 to £150,000, with the "additional rate" of 45% paid on anything over £150,000.

“Under UKIP's plans, everyone earning between about £44,000 and £55,000 would pay income tax at 35p. Those earning more will pay 40p, with the additional rate scrapped. “

Despite other policy failings, UKIP's commitment to raising personal allowance surpasses the coalition's and should be heavily applauded.

This is the first policy of 'party conference season’ that properly addresses the root of the cost-of-living crisis and provides a simple, effective solution to relieve the tax burden on low-income earners.

For years, the Adam Smith Institute has illustrated the pointlessness in taxing workers out of a living wage, to then compensate their low income with government handouts and benefits. The Labour party’s recent pledge to raise the minimum wage to £8 an hour threatens to put more young, unskilled workers out of jobs, while still taking away a substantial potion of income from anyone who happens to benefit from the small pay raise.

A hike in minimum wage is a symbolic gesture at best, that continues to tax away - or destroy - low-earner incomes. A raise in the personal allowance threshold, however, gets more money into the pockets of those earners, creating no dangerous side effects in the jobs market.

With both the Liberal-Democrat and Conservative Party Conferences ahead of us, we can only hope both party leaders will continue to embrace an increase in personal allowance and match UKIP’s threshold; or maybe even one-up them. (National Insurance cuts, anyone?)

Colin Hines and the Magic Money Tree

It had to happen of course: once people started talking about unconventional monetary policy then there was always going to be someone who espied the Magic Money Tree. And it's Colin Hines who has:

It was heartening to hear Ed Miliband say in his speech that tackling climate change is a passion of his and that solving it could be a massive job-generating opportunity (Report, 24 September). The inevitable question of how to pay for this can be tackled by writing to Mark Carney, the governor of the Bank of England. He is on record as saying that if the government requested it, then the next round of QE could be used to buy assets other than government debt. Miliband said that the Green Investment Bank would be used to fund green economic activity and so Labour should allow it to issue bonds that could then be bought by the Bank using “Green QE”. Similarly, local authorities could issue bonds to build new energy-efficient public homes funded by “Housing QE”.

The Bank has already pumped £375bn of QE into the economy, but with little tangible benefit to the majority. Imagine the galvanising effect on the real economy of every city and town if a £50bn programme of infrastructural QE became the next government’s priority. This could make every building in the UK energy-tight and build enough highly insulated new homes to tackle the housing crisis. It would provide a secure career structure for those involved for the next 10 years and beyond, massive numbers of adequately paid apprenticeships and jobs for the self employed, a market for local small businesses, and reduced energy bills for all. Such a nationwide programme would generate tax revenue to help tackle the deficit, but in an economically and socially constructive way. Best of all it would not be categorised as increased public funding, since QE spending has not and would not be counted as government expenditure. Colin Hines Convener, Green New Deal Group

Wonderful, eh? We can have everything we want, and a pony, without ever having to pay for it!

Hurrah!

The problem being that Hines (and there are others of that ilk out there too) hasn't grasped the difference between the creation of credit to reduce interest rates (what QE does) and the creation of base money to spend into the real economy. That second has rather different effects: as the Germans found out post WW I, the Hungarians post WW II and the Zimbabweans more recently. It creates hyperinflation, those last having it to such a bad extent that they kept printing until they'd run out of the real money necessary to buy the ink to print the play money.

I do not, note, claim that £1 billion or £50 billion or even £500 billion of this "Green QE" will inevitably produce inflation of 1000 % a day. I do however claim that use of this Magic Money Tree will, given the way that politics works (which politician doesn't like spending money she's not had to find through taxation?) will inevitably lead to hyperinflation. For the thing is we've tried this experiment before, many a time, and that is always what does happen.

Simply not a good idea.

Trying to explain the American academic jobs market

Something's clearly not right about the academic jobs market in the US. The actual process of applying for a job seems to take forever and as one of the more recent Nobel Prizes pointed out such search frictions and inefficiencies do prevent markets from clearing. This is, you know, a bad thing. Further, we've got the fact that American academia is pumping out huge numbers of Ph.Ds who then can't find jobs as tenured professors: but also can't find them elsewhere in the economy as the only thing they've really been trained to do is to try and become tenured professors. They thus end up trying to survive on less than minimum wage as adjunct professors.

So this isn't what we might want to hold up as an example of a successful part of the jobs market. But the question then becomes, well, why is it like this? What's gone wrong?

One possible answer being that this is what happens when you let the left wingers try to run a market. It's not actually much of a surprise to anyone, or at least it shouldn't be, that the US professoriate runs largely leftish. 90% to 10 D to R is the usual number bandied about. It also wouldn't be a surprise to find out that those who do the academic administration tend further left than that: there does have to be an explanation for the various diversity policies around the place.

The end result being extraordinarily strong union protections (that tenure means that, roughly, absent raping the Dean in his office no professor can get fired), vast overtraining of would be market entrants and the majority not actually being able, they being excluded from those union protections, to gain a living. Oh, and the end product becoming ever more expensive as the providers layer themselves with ever more orgies of bureaucracy.

Sounds just wonderful really: or perhaps we might want to use it as a warning. This probably isn't the way that we want the entire jobs market to work so let's not attempt to add more of those job protections, unionisation and so on.

Everything's coming up monetarist!

In "QE and the bank lending channel in the United Kingdom", BoE economists Nick Butt, Rohan Churm, Michael McMahon, Arpad Morotz and Jochen Schanz tackle the popular creditist view that movements in lending drive overall activity, and that quantitative easing works by stimulating lending, and find "no evidence to suggest that quantitative easing (QE) operated via a traditional bank lending channel". Instead, their evidence is consistent with the monetarist view, that "QE boosted aggregate demand and inflation via portfolio rebalancing channels." They find this result by looking at the difference between banks that dealt directly with the Bank of England when it was buying gilts (UK government bonds) with new money in its QE programme. If the creditist view held, these banks would be more able to expand their lending with the extra deposits created when the BoE hands over new money for gilts.

Our first approach exploits the fact that, for historical and infrastructural reasons, it is likely that not all banks are equally well placed to receive very large OFC (other financial corporation) deposits. We use historical data on the share of banks’ OFC funding (relative to their balance sheet) to identify a group of banks that are most likely to have received deposits created by QE, which we call ‘OFC funders’. We use this variable, along with variation in banks’ OFC deposit funding to test whether there was a bank lending channel by comparing the lending response of such OFC funders to that of other banks during the QE period.

They check their result by looking at gilt sales that commercial banks had no control over, since they were obliged to carry them out on the behalf of their clients. This makes them random with respect to those banks' separate funding and lending decisions, and isolates the effect of extra deposits created by QE on those banks' credit activity.

Our second approach makes use of the fact that while most gilt purchases were from OFCs, these had to be settled via banks who were market makers in gilts. As these gilt sales were likely to be unrelated to banks’ lending decisions, we can use data on gilt sales to remove the endogenous variation in banks’ OFC deposit holdings and so test for a bank lending channel using an instrumental variables approach that controls for the interrelatedness of the bank’s decision.

This paper only adds to a welter of recent studies supporting the monetarist perspective on the macroeconomy. "Institutional investor portfolio allocation, quantitative easing and the global financial crisis", another BoE paper released earlier this month found, like Butt et al., that pension funds and insurers rebalanced their portfolios in response to QE, moving away from gilts and into corporate bonds relative to what they would have done without the programme.

If firms rebalance their portfolios to reflect their preferences, then relative prices would not appear to be 'distorted' by the programme, and markets would still be performing their chief function—aggregating information so everyone can economise effectively and create wealth.

Another BoE paper, from April, "What are the macroeconomic effects of asset purchases?" found that:

Our results suggest that asset purchases have a statistically significant effect on real GDP with a purchase of 1% of GDP leading to a .36% (.18%) rise in real GDP and a .38% (.3%) rise in CPI for the United States (United Kingdom).

Finally, another new paper tells us that even the good old quantity theory of money is pretty good at forecasting post-war US inflation. Looks like everything's coming up monetarist!

It really is the planning system that's harming us

It really is the 1947 Town and Country Planning Act that is causing our housing problems:

Britons live in the smallest homes in Western Europe because of draconian planning laws restricting house building, a report found yesterday.Residential floor space in Britain is on average just 66 square metres (710 square feet) per household, compared to a spacious 118 square metres (1,270 sq ft) in Ireland, 115 square metres (1,238 sq ft) in Denmark or 110 square metres (1,184 sq ft) in Italy, according to data compiled by the Institute of Economic Affairs.

‘All the evidence suggests that years of tight planning controls restricting house building has led to us having the smallest space per household in Western Europe.’ The figures were compiled as part of a report which confronted some of the most widely-held views about the cost of living crisis.

We have some of the most expensive housing in Europe and some of the smallest. Those two logically go together of course: people tend to consume less of something the more expensive it becomes. But is it actually desirable?

If we were facing a shortage of land upon which to build then perhaps so. If something does have to be rationed then rationing by price is the way to do it. But there isn't any shortage of land. Housing takes up some 3% of England all urban areas no more than 10%. Famously, more of Surrey has golf courses than housing on it. What we do have though is a shortage of the pieces of paper that allow building a house on a piece of land.

Many say that this is a problem that government should solve. Build more council houses for example, force the private sector to do so. And the aim is correct, the government should solve this problem. But not by actually doing anything of course. That shortage of planning permissions is an active action by government: and the solution is therefore for them not to try to do something but to stop doing something.

Simply liberalise that planning system. After all, the last time the private sector built houses in the sort of volumes we need today was the 1930s. And it built all those houses where people wanted to live, in sizes they desired: those semi-urban semis are exactly what people find desirable today as well, judging by their prices. And all of this was done without much restriction on what could be built where.

We know this solution works because the last time we had a reasonably functional housing market was when we had an absence of that planning.

The visa and the sausage

The policy making process is a messy business. It is widely and fairly quoted that “laws, like sausages, cease to inspire respect in proportion as we know how they are made.” Think tanks sit at the very start of the policy process – writing recipes for politicians to feed to the public (as well as writing recipes for the public to feed to politicians). However, polices can become adulterated as they are funnelled through the sausage machine of government. Some policies are just bad ideas – such as the creeping reintroduction of incomes policies, which dramatically and unequivocally failed in the 1970s – but some good policies fail in their implementation. At least one is failing because nobody knows it exists: the Tier 1 Exceptional Talent Visa for tech.

As Sam Shead explains at TechWorld:

As part of an effort to get more of the world's best tech entrepreneurs and software engineers to come to the UK, prime minister David Cameron announced last December that the government was going to allow Tech City UK to endorse 200 of the 1000 slots. At the time, Cameron said more overseas talent was needed if the UK wanted to overcome the skills gap that exists in the tech sector.

The Tier 1 Exceptional Talent Visa should be a fast-track for tried and tested entrepreneurs to enter the UK, but even though Tech City UK has been free to endorse entrepreneurs since April, the policy is struggling to get off the ground.

The failure is largely the result of so few people knowing the visa route even exists. I’ve spoken with plenty of entrepreneurs, recruiters and lawyers – all of whom are needed to make this policy work in practice. Most haven’t heard of this visa route and none has the information required to understand the process. There is plenty of blame to go around but Tech City UK and UKTI probably deserve the brunt of it.

The failure of the Tier 1 Exceptional Talent Visa tech demonstrates how government departments and quangos are falling short in their job of communicating policy to so-called stakeholders (for want of a better word). We can’t rely on MPs to spread the word. In a recent poll commissioned by The Entrepreneurs Network it was discovered that they are largely ignorant of current policies to support entrepreneurs.

Based upon the evidence (and my cosmopolitan biases), fiddling with the Tier 1 Exceptional Talent Visa doesn’t go nearly far enough in liberalising the immigration system. But before this great battle of ideas is won – which will encompass cultural as well as economic clashes – every failing policy is a setback.

Philip Salter is director of The Entrepreneurs Network.

On Ed Miliband's new tax on tobacco profits

Ed Miliband has decided that there should be higher taxes on the profits of cigarette companies. The argument being that smoking costs the NHS money and that thus some cash should come from the one activity to cover the other. However, that activity of smoking already more than covers the public costs associated with it. As is helpfully pointed out here:

Estimates for the amount spent on tobacco in the UK in 2011 range from £15.3bn to £18.3bn. The cost of smoking to the NHS is put at between £2.7bn and £5.2bn.The Treasury earned £9.5bn in revenue from tobacco duties in the financial year 2011-12.

When even The Guardian is pointing out the mathematical difficulties with a Labour Party leader's promises then it would be fair to say that it's not really going to fly, wouldn't it?

And that is rather the point about smoking. The activity is already sufficiently taxed that it pays for all of the public costs associated with it and more (and that's to ignore the fact that shorter lifespans as a result save the NHS money). There are substantial private costs of course: but public taxation isn't the correct way to deal with such private costs either.