Well, yes and no Professor Krugman, yes and no

The economics of this is of course correct For Paul Krugman is indeed an extremely fine economist:

We may live in a market sea, but most of us live on pretty big command-and-control islands, some of them very big indeed. Some of us may spend our workdays like yeoman farmers or self-employed artisans, but most of us are living in the world of Dilbert.

And there are reasons for this situation: in many areas bureaucracy works better than laissez-faire. That’s not a political judgment, it’s the implicit conclusion of the profit-maximizing private sector. And people who try to carry their Ayn Rand fantasies into the real world soon get a rude awakening.

The political implications of this are less so, given that Paul Krugman the columnist is somewhat partisan.

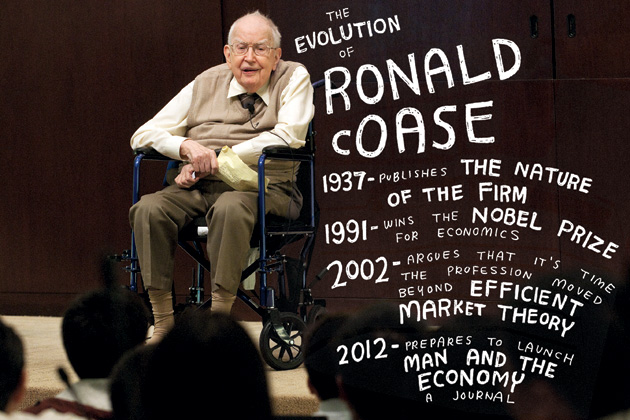

And of course that implication is that since that private sector (as Coase pointed out a long time ago) uses bureaucracy at times then we should all shut up and simply accept whatever it is that the government bureaucracy decides to shove our way.

Which is to slightly miss the point: yup there's command and control islands in that sea. Bit it's that sea that srots through those islands, sinking some and raising others up into mountains. Which is something that doesn't happen with the monopoly of government bureaucracy: they don't allow themselves to get wet in that salty ocean of competition.

That planning and bureaucracy can be the most efficient manner of doing something? Sure. That sometimes it's not? Sure, that's implicit, explicit even in the entire theory. How do we decide? Allow that competition. It's the monopoly of the government bureaucracy that's the problem, not that we somtimes require pencil pushers to push pencils.

RIP John Nash

In a Think Piece for the Adam Smith Institute, Vuk Vukovic pays tribute to the endlessly influential theorist John Nash:

It is with great sorrow we hear that one of the greatest minds in human history died this weekend in a car crash with his wife while they were returning home from an airport. John Forbes Nash Jr., was widely known as one of the founders of cooperative game theory whose life story was captured by the 2001 film "A Beautiful Mind", is truly one of the greatest mathematicians of all time. His contributions in the field of game theory revolutionized the way we think about economics today, in addition to a whole number of fields - from evolutionary biology to mathematics, computer science to political science.

You can read the whole piece here

In memoriam: John Nash

It is with great sorrow we hear that one of the greatest minds in human history died this weekend in a car crash with his wife while they were returning home from an airport. John Forbes Nash Jr., was widely known as one of the founders of cooperative game theory whose life story was captured by the 2001 film "A Beautiful Mind", is truly one of the greatest mathematicians of all time. His contributions in the field of game theory revolutionized the way we think about economics today, in addition to a whole number of fields - from evolutionary biology to mathematics, computer science to political science.

John Nash was born in 1928 in Bluefield, West Virgina. Even as a child he showed great potential and was taking advanced math courses in a local community college in his final year of high school. In 1945 he enrolled as an undergraduate mathematics major at the Carnegie Institute of Technology (today Carnegie Mellon). He graduated in 1948 obtaining both a B.S. and an M.S. in mathematics and continued onto a PhD at the Department of Mathematics at Princeton University. There's a famous anecdote from that time where his CIT professor Richard Duffin wrote him a letter of recommendation containing a single sentence: "This man is a genius". Even though he got accepted into Harvard as well, he got a full scholarship from Princeton which convinced him that Princeton valued him more.

While at Princeton, already on his first year (in 1949) he finished a paper called "Equilibrium Points in n-Person Games" (it's a single-page paper!) that got published in the Proceedings of the National Academy of Sciences (in January 1950). The next year he completed his PhD thesis entitled "Non-Cooperative Games", 28 pages in length, where he introduced the equilibrium notion that we now know as the Nash equilibrium, and for which he will be awarded the Nobel Prize 34 years later. It took him only 18 months to get a PhD: he was 22 at the time.

While at Princeton he finished another seminal paper "The Bargaining Problem" (published in Econometrica in April 1950), the idea for which he got from an undergraduate elective course he took back at CIT. It was Oskar Morgenstern (the co-founder of game theory and the co-author of the von Neumann & Morgenstern (1944) Theory of Games and Economic Behavior) who convinced him to publish that bargaining paper. The finding from this paper will later be known as the Nash bargaining solution. At Princeton he sought out Albert Einstein to discuss physics with him (as physics was also one of his interests). Einstein reportedly told him that he should study physics after Nash presented his ideas on gravity, friction and radiation.

Illness and impact

After graduating he took an academic position at MIT, also in the Department of Mathematics, while simultaneously taking a consultant position at a cold war think tank, the RAND Corporation. He continued to publish remarkable papers (his PhD thesis in The Annals of Mathematics in 1951, another paper called "Two-Person Cooperative Games" in Econometrica in 1953, along with a few math papers). He was given a tenured position at MIT in 1958 (at the age of 30), where he met and later married his wife Alicia. However, things started to go wrong from that point on in his personal life and career. In 1959 he was diagnosed with paranoid schizophrenia, forcing him to resign from MIT. He spent the next decade in and out of mental hospitals. Even though he and his wife divorced in 1963, she took him in to live with her after his final hospital discharge in 1970.

Nash spent the next two decades in relative obscurity, but his work was becoming more and more prominent. Textbooks and journal articles using and applying the Nash equilibrium concept were flying out during that period, while most scholars that built upon his work thought he was dead. It was not only the field of economics - where the concepts of game theory were crucial in developing the theory of industrial organizations, the public choice school and the field of experimental economics (among many other applications) - it was a whole range of fields; biology, mathematics, political science, international relations, philosophy, sociology, computer science, etc. The applications went far beyond the academia; governments started auctioning public goods at the advice of game theorists, business schools used it to teach management strategies.

Arguably the most famous applications were to the cold war games of deterrence that explain to us why the US and Russia kept on building more and more weapons. The Nash equilibrium concept explains it very simply - it all comes down to a credible threat. If Russia attacks the US it must know that the US will retaliate. And if it does, it will most likely retaliate with the same fire-power Russia has. Which will lead to mutual destruction of both countries. In order to prevent a full-scale nuclear war (i.e. in order to prevent the other country from attacking), the optimal strategy for both countries is to build up as much nuclear weapons as they can to signal to the other player what they're capable of. This will prevent the other player from attacking. If they are both rational (i.e. if they want to avoid a nuclear war and total destruction) they will both play the same strategy and no one will attack. Paradoxically, peace was actually a Nash equilibrium of the arms race!

Long-overdue recognition

Little did Nash have from all this. He had no income, no University affiliation and hardly any recognition for his work. But this all changed in the 1990s when he was finally awarded an overdue Nobel Prize in Economics in 1994, with fellow game theorists John Harsanyi and Reinhard Selten "for their pioneering analysis of equilibria in the theory of non-cooperative games".

His remarkable and actually very painful life story was perfectly depicted by his autobiographer and journalist Sylvia Nasar in her two books; "A Beautiful Mind" (on which the subsequent motion picture was based) and "The Essential John Nash", which she co-edited with Nash's friend from college Harold Kuhn (also a renowned mathematician). As Chris Giles from the FT said in his praise of the latter: "If you want to see a sugary Hollywood depiction of John Nash's life, go to the cinema. Afterwards, if you are curious about his insights, pick up a new book that explains his work and reprints his most famous papers. It is just as amazing as his personal story." The book contains a facsimile of his original PhD thesis, along with eight of his most important papers (from game theory and mathematics) reprinted.

After the Nobel Prize success things got better for Nash. By 1995 he recovered completely from his "dream-like delusional hypotheses", stating that he was "thinking rationally again in the style that is characteristic of scientists." Refusing medical treatment since his last hospital intake, he claimed to have beaten his delusions by gradually, intellectually rejecting their influence over him. He rejected the politically-oriented thinking as "a hopeless waste of intellectual effort". In 2001 he remarried his wife Alicia and started teaching again at Princeton, where he continued his work in advanced game theory and has moved to the fields of cosmology and gravitation.

The Phantom of Fine Hall, as they used to call him in Princeton due to his mystique and the fact that he used to leave obscure math equations on blackboards in the middle of the night, will never cease to raise interest, praise and awe. Nash was another perfect example of a thin line between a genius and a madman. Luckily, in the end, his genius prevailed.

So what is the Nash equilibrium?

The reason why this concept was so revolutionary was because it significantly widened the scope of game theory at the time. In the beginning, following the von Neuman and Morgenstern setting, game theory was focused mostly on competitive games (when the players' interests are strictly opposed one to another). These types of games were known as zero-sum games, limiting to a significant extent the scope of game theory. Nash changed that by introducing his solution concept so that any strategic interaction between two or more individuals can be modelled using game theory, where the most unique solution concept is the Nash equilibrium. Games are not zero-sum, they aren't pure cooperation nor pure competition. They are a mixture of both.

The idea of the Nash equilibrium resonates from the simple assumption of rationality in economics. The term rationality in economics is not the same as common sense rationality we all think about upon hearing this term. It refers to the idea that each individual will act to achieve his or her own objective (maximize their utility), with respect to the information the person has at his/her disposal. The concept of rationality in economics is therefore idiosyncratic - it depends on whatever a particular individual deems rational for themselves at a given point of time. It rests upon the idea that a person will never apply an action that hurts him/her in any way (lowers his/her utility).

The Nash equilibrium is the most general application of this idea. A non-cooperative game, according to Nash, is "a configuration of strategies, such that no player acting on his own can change his strategy to achieve a better outcome for himself". In other words, if there exists another strategy that can make an at least one individual better off, then the outcome does not satisfy the condition for a Nash equilibrium.

Let's look at an example. The most simplified example of how a Nash equilibrium solution concept works is the Prisoner's Dilemma game. Consider two robbers arrested for a crime. They are both being interrogated by the police in separate rooms. They are presented with two options (strategies): keep quiet (silent) or betray the other guy (betray). If they both remain silent, they both only get a light sentence of a year in prison for obstructing justice. If one betrays the other and the other guy keeps silent, the betrayer is released with zero imprisonment, and the other guy gets pinned for the whole crime and gets nine years in prison. If they both betray each other, they both get six years in prison. What's the optimal thing to do?

Applying the Nash equilibrium concept we need to find a strategy that is the best response of one player to whatever the other player may decide. When no players have any incentive to deviate from a set of strategies (strategies are always a pair in two-person games) we can say that this set of strategies is a Nash equilibrium.

Consider the game depicted in the table below:

It would seem that the best strategy they can apply is for both to keep silent. If they do, they both get only a light sentence. However this strategy set (-1,-1) is not a Nash equilibrium since at least one person has an incentive to deviate. In fact, they both do. If Prisoner 1 decides to defect and betray Prisoner 2, he gets 0 years in prison, while Prisoner 2 gets 9 years (third cell, with payoffs 0,-9). Prisoner 2 applies the exact same reasoning (second cell with payoffs -9,0). In the end since the better strategy is always to betray, they both play the same strategy (betray, betray) and end up with payoffs (-6,-6) which is the Nash equilibrium of this game. From this point no player can deviate and make himself better off. If Prisoner 1 decides to go for silent he risks getting 9 years in prison instead of 6. There is no way for them to reach a cooperative equilibrium in this simplified scenario.

Naturally, cooperative games do exist and they help us understand how game theory solves for example the free rider and the collective action problem. It was Elinor Ostrom (1990) who applied these concepts to reach her optimal solutions in solving the common pool resource problem in small groups with persistent interactions. Robert Axelrod (1984) is another, finding that even though the defection strategy is more rational, sometimes various other factors will result in a cooperative outcome between the players. The Nash equilibrium helped initiate a huge amount of research on these and many other problems within and outside the academia. The reason game theory is usually considered as the most applicable economic theory - in that it can be used to solve real-life problems - is purely thanks to John Nash.

Rest in peace.

Most notable papers:

"Equilibrium Points in N-person Games". Proceedings of the National Academy of Sciences 36 (36): 48–9. (1950)

"The Bargaining Problem". Econometrica (18): 155–62. (1950)

"Non-Cooperative Games". Annals of Mathematics 54 (54): 286–95. (1951)

"Real Algebraic Manifolds". Annals of Mathematics (56): 405–21. (1952)

"Two-Person Cooperative Games". Econometrica (21): 128–40. (1953)

"The Imbedding Problem for Riemannian Manifolds". Annals of Mathematics (63): (1956).

"Continuity of Solutions of Parabolic and Elliptic Equations". American Journal of Mathematics 80 (4): 931-954. (1958)

Do we need the FCA?

Students of the Financial Conduct Authority will appreciate the FCA’s Business Plan 2015/16 which mostly sets out what it does, but also touches on what it achieves and its value for UK citizens. It is as close to accountability as the FCA gets.

What does the FCA do?

The core business is the supervision “of about 73,000 financial services firms operating in the UK, and we prudentially supervise those that are not covered by the Prudential Regulation Authority (PRA). We look closely at firms’ business models and culture and use our judgement to assess whether they are sound and robust.” (p.63) Understanding each of 73,000 firms better than the manager of that firm is a Herculean task even with 3,060 staff and a budget of £460M. But that is only part of the FCA’s business.

Annex 2 lists 106 new EU regulatory initiatives in which the FCA is involving itself. It would be good to believe they were seeking to reduce the number, and simplify and reduce the burden, of the on the British financial sector and its consumers. There is no hint that such is the case. The FCA seeks “active engagement” which can be translated as assisting more rather than less.

In addition, the FCA has a programme of domestic regulation. Yet the FCA should not now be creating new financial regulations at all. Under the Brown administration’s agreement with the EU, Brussels is responsible for all new financial regulation leaving the UK solely with supervision. For the FCA to add new rules is not merely piling Pelion upon Ossa, it is undermining the City’s competitiveness and unnecessary. In a single market, a regulation is either needed everywhere or nowhere.

In June 2014, the Chancellor created a Fair and Effective Markets Review (FEMR) of financial services, co-chaired by the Bank of England, FCA and HM Treasury. The report is due next month but has been widely trailed. Before we see that review (due July), and in an effort to keep itself busy, the FCA has announced a further review (due spring 2016) covering some of the same ground, the Investment and Corporate Banking Market Study (ICBMS): “We are examining issues around choice of banks and advisers for clients, transparency of the services provided by banks, and bundling and cross-subsidisation of services.”

In addition Annex 1 lists 30 “current and planned market studies and thematic work” not all of which will lead to new regulation. Perhaps the most significant is the “Culture review”. There is no mention of whose culture, nor how and why it should be reviewed. Reassuringly the start and finish dates have yet to be decided.

So far as one can see from the business plan, the FCA has no central guiding principle to determine what it should do. The Financial Ombudsman Service deals with consumer complaints and the Competition and Markets Authority deals with policing fair markets and competition. By contrast, the FCA seems to involve itself without restraint in anything it feels like doing. It is no surprise that its costs are growing at 6% p.a.

Measuring performance against the statutory objectives

The Chairman, in his foreword to the plan, highlights the FCA’s “principal tool [for measuring success], our outcomes-based performance framework” (p.7). As searching that description did not reveal such a framework, he presumably is referring to the table below.

It is unusual, to say the least, to have a set of performance measures without a single number. And there is no discussion about whether these objectives, for that is all they are, can be attributed to the FCA or not. Most of them are what the firms do but it is impossible to know whether the firms’ performance improved, or quite possibly deteriorated, as a result of the FCA intervention. It may be hard for the firm to keep the consumer at the centre of its attention if the FCA is knocking on the door.

The paperwork I now have to complete for my stockbroker has multiplied two or three times as a result of “compliance” which I also have to spend £20 a time for. In all other respects, the service is exemplary, but this has tipped my stockbroker experience from satisfaction to complaint.

The “respected regulatory system” will let only the good firms know where they stand, leaving the miscreants, presumably, in the dark. Is low financial crime an indication of the FCA doing well or failing to detect crimes or, just possibly, the police deterring crime and catching criminals?

The Business Plan refers the reader to their quarterly data bulletin for the actual figures but, guess what?, these have little to do with the table above. They are:

-

Monthly number of people contacting FCA about consumer credit.

-

Outcomes of upheld complaints.

-

Annual volume of “approved persons”. There are about 20,000 p.a. and, in the last two years, not a single application has been rejected.

-

Attestations “are a supervisory tool used to ensure clear accountability and a focus from senior management on putting things right in regulated firms.” Basically they are individual senior executives promising to put things right. There were 74 of those in the year to March 2015.

-

Skilled person reports. There are 50-60 cases a year of consultants being called in to investigate matters more closely. The great majority are conducted by accounting firms at a cost of over £150M p.a. The quarterly data simply give the number, not the cost nor whether they are value for money, still less whether the FCA adds any value.

-

The number of financial promotions. The relevance of this item to FCA performance measurement is opaque.

The simple bottom line of this section is that there is no performance measurement of the FCA. It is an elaborate charade.

Value for Money?

In his Foreword, the Chairman also stated “We are also committed to working as efficiently as possible with firms to deliver value for money, as well as the right outcomes for consumers and the financial markets.” (p.7). This topic next arises, in any substantive way, on p.37: “We remain focused on the principles of good regulation and advancing our objectives in the most efficient and effective way. We will continue to measure and evaluate our impact and report publically [sic] on this. Our aim will be to be as effective as possible and focus our resources on the front line of regulation. In 2015 we will launch an Efficiency and Effectiveness Review, which will look at the value for money of areas of higher expenditure. As part of this we will review our governance and decision-making processes. To embed this we will have a new structure,”

This good intention is repeated a number of time in the pages following, e.g. “We will achieve this by delivering year-on-year improvements in effectiveness, efficiency and economy. One of the key drivers of our strategy is to increase our efficiency and effectiveness.” (p.72).

Nowhere does the plan indicate how the FCA’s effectiveness, efficiency and value for money should be measured, still less what the numbers are or should be. The nearest we get is the p.37 quote above. As some army wag wrote on a Berlin wall in the 1940s: “we tend to meet any new situation by reorganising; and a wonderful method it can be for creating the illusion of progress while producing confusion, inefficiency and demoralisation.”

There is no evidence of the FCA providing value for money or even understanding how that might be measured.

Conclusion

All the things the FCA does could be done as well, if not better, by other agencies:

-

Consumer complaints have vastly increased since the FCA and Ombudsman services were created. In the year to Match 2015 the FCA had 150,000 consumer contacts (almost all complaints) and the Ombudsman contacts have risen from 62,170 in 2003 to 512,167 in 2014. One has to wonder about cause and effect. There are undoubtedly too many cases coming to the FCA and Ombudsman Service but the answer to that is not to increase these quangos, and allow malpractice to grow, but to take systemic action to minimise malpractice and when it does not arise, pressure the firms to deal with the complaints themselves, e.g. by massively increasing the penalties on complaints upheld by these two quangos, including gaol sentences.

-

Consumer complaints do, and should, go to the Financial Ombudsman Service which has 2,400 staff of its own. The FCA deals with only about 25% and is not now needed.

-

As noted above, the FCA should not now be creating new financial regulations at all. It should be helping the EU deregulate, simplify and reduce the burden of financial regulation, not assisting the EU in undermining the City’s competitiveness. In a single market, a regulation is either needed everywhere or nowhere.

-

Much of the wholesale side of the FCA’s supervision is purely “prudential” because it overlaps with supervision by the Bank of England through the Prudential Regulatory Authority. The BoE should be left to get on with it.

-

About one third of the cost of the FCA relates to the investigatory work contracted out to professionals, largely accounting firms. It should not take more than a couple of people to choose the firms, the terms of reference and make out the cheques. This, and all remaining FCA functions, could be handled by the Competition and Markets Authority. Indeed that would be a better solution anyway to bring consistency to markets and competition policy.

It is hard to resist the conclusion that the FCA is not simply redundant but a drain on the effectiveness, resources and efficiency of the vital financial services sector. It should be abolished.

When a fossil fuel subsidy is not a subsidy

You may have seen an IMF report in the news last week claiming that fossil fuels are subsidised to the tune of over five trillion dollars every year. This made good headlines, but only because the IMF chose to describe untaxed externalities as 'post-tax subsidies'. This is unusual and misleading. I wrote about why in The Daily Telegraph:

The IMF’s idea of “subsidies” to fossil fuels refers to something completely different. They have taken the indirect costs to society of using energy – air pollution, traffic congestion, climate change – and, if governments haven’t imposed special taxes on one, called it a “subsidy”. The problem is, we already have a word for these things: externalities. And there is something rather Orwellian about describing a failure to tax something as a subsidy. Here’s an example of what we’re talking about: when my neighbours play loud music at night, it makes me worse off. I’d pay, maybe, £20 for them to shut up, if it wasn’t so awkward to go to the flat downstairs, knock on their door and start negotiating prices. Economists would say that they are imposing a £20 externality on me, and that in a perfectly efficient world, my building would charge residents around that much to play music, and give it to sleep-deprived neighbours like me. But, in the absence of that charge, nobody would say that those neighbours are being subsidised by me. It’s just not what the word means. Except, apparently, to the IMF.

That isn't to say that externalities should never be taxed, if a private solution can't be found. But we already have high fuel taxes in most of the developed world, and in the developing world these taxes will hold back growth. Since economic development has positive externalities, it's not obvious that the negative externalities of fossil fuels outweigh the positives. You can read the whole piece here.

Spotting Worstall's Fallacy in the wild

In a discussion of Joe Stiglitz's new book in The Observer we see this:

Back in 2008 the top 20% of households in the country were estimated to be worth 92 times more than the bottom 20%. The latest estimate puts the gap at more than 100 times. And a further £12bn of welfare cuts are planned by the new Conservative government. The gap between rich and poor is unquestionably widening.

That conclusion may or may not be right but it's most certainly not supported by the evidence which is given of the contention. That evidence coming from this ONS report:

Total net wealth is defined as the sum of four components: property wealth (net), physical wealth, financial wealth (net) and private pension wealth . It does not include business assets owned by household members, for instance if they run a business; nor does it include rights to state pensions, which people accrue during their working lives and draw on in retirement.

It's known as Worstall's Fallacy simply because our own Tim Worstall bangs on about it so often. We cannot measure inequality (or poverty, any number of other things) without taking into account the things we do to reduce said inequality (or poverty, or any other problem). It's only when we look at the post-attempt to solve the problem situation that we can turn our minds to whether we should be doing more, or possibly less, to try to solve this problem.

So, note that our definition of wealth there does not include that state pension: something we do to reduce the wealth and income disparities between those who can save for a private pension and those that cannot. Note that it includes private housing equity but not the capital value of a below market rate tenancy for life ("social housing"). It does not include the capital value of health care, or education, free at the point of use, for all the citizenry. It does not include whatever capital value we might ascribe to the social insurance policies that will provide us with an income in the case of economic misfortune.

We do all of these things because they make people wealthier. Perhaps not as wealthy as other arrangements might make them, but the essential driving point is that we consider health care, education, social insurance and so on make people wealthier. Thus, in our discussion of wealth we must include them. We cannot look solely at the market distribution of purely market wealth and even attempt to decide whether more or less should be done to try to change that distribution. We must look at the post- all the redistribution we already do situation to be able to make a decision.

To switch from wealth to income to make this point. The TUC has done the calculation about income inequality. Between the top 10% and bottom 10% the market inequality is about 30:1. Maybe that's too high, maybe that's not high enough, your moral choice. When we take account of taxation and benefits that falls, and when we take account of government provided services, that health care and eduation and so on, it falls again. To 6:1. Again, you can say that this consumption inequality is still too much, or not enough, your moral choice. But 6:1 is very definitely different from 30:1.

And what is the relevant ratio to be looking at if we want to make a decision upon whether to do more redistribution or less? Quite, it's obviously that 6:1 one, not the 30:1. And so it is with wealth or poverty or so many other problems. The number we need for our decision is the extent of the problem on the ground, not the extent of the problem before all of the things that we already do.

Assigning reasonable capital values to the effects of both the welfare state and government provided services brings the 10/90 wealth ratio down to anywhere between 20:1 and 5:1. We could and would defend anywhere in that range dependent upon assumptions. Is that too much? Not enough? Entirely up to your moral choices. But it's very different from that 100:1, isn't it, and it's also the relevant number we need to use when thinking about what to do next.

A glorious example of political naivety

There's any number of lessons that we might take from the past few years. Fragile banking systems aren't a good idea perhaps. We seem to have shown that monetary policy is still effective at the zero lower bound, therefore fiscal policy isn't the only thing we can turn to in recession. The eurozone is giving a useful empirical lesson in optimal currency areas. There's all sorts of things we can and should learn from recent times. But then it's also possibly to be hoplessly naive about all of this:

The biggest surprise for me, and perhaps it shouldn't have been, is the degree to which politicians are willing to put political interests ahead of helping people in need. Watching the political/policy reaction to the Great Recession was both disappointing and eye opening.

Well, no, it shouldn't have been. Ourselves we waver between thinking that public choice theory is the right way to think of this (politicans and bureaucrats are subject to the same incentives of self-interest as everyone else) and the pronouncements of Mancur Olson (all governments are bandits exploiting the population and about the best we can hope for is a stationary bandit, not a roving one) dependent upon the crust of our liver on any particular day. But either insists that we cannot look to the political class as being interested in either what we want or what we need: not unless it's going to directly impact upon our propensity to vote for them so that they get to stay part of that political class.

The idea that a professional economist should believe that politicians would ever put helping people in need above political interests strikes us as simply hopelessy naive. However, this is still a good outcome: the next politician promising that we're going to run the world off kisses and unicorn parps is less likely to be believed now, eh?

Don't fear the trade bill

We do admit we find this all rather amusing. We've all been shouted at for months now that the transatlantic trade deal (and various others under discussion) will allow such evils as tobacco companies suing if they are deprived of their intellectual property as a result of plain packaging. Thus we must reject said trade deals. And then this happens:

One such measure is the introduction of plain cigarette packaging – a policy that David Cameron’s successful spinmeister and tobacco lobbyist, Lynton Crosby, thankfully failed to block. But now the tobacco companies are fighting back, suing the government for up to £11bn on the basis that it would constitute “deprivation of a highly valuable intellectual property”.This is an absurd example of how the law values property over people. Our government is democratically elected. Yes, that rightly means there have to be checks and balances, and policies must abide by the existing framework of the law. But if the law enables tobacco companies to extort £11bn from the government – money, ironically enough, that could be used to treat people suffering from tobacco-related illnesses – then the law is wrong. If the law does not value people’s lives and wellbeing over the rights of tobacco companies to make profit from cancer sticks, then the law is morally bankrupt.

This privileging of corporate interests over democracy is only going to get worse. The Transatlantic Trade and Investment Partnership – a treaty being hammered out between the EU and the US with woefully little scrutiny – could grant companies the same legal rights as nation states, enabling them to sue elected governments in secret courts to block policies that dent future profits. And sure enough – using a similar treaty – Philip Morris sued the Australian government for the same policy. It used the same tactic against Uruguay’s government for enlarging health warnings on cigarette packages.

How it is going to get worse if these provisions are already in domestic law?

At which point we can point out the two important points here.

The first is that the law, rightly, contains provisions on such things as eminent domain, just as it contains provisions of rights to property. The government can indeed confiscate property on the grounds of greater national need. It can force you to proffer up your house for the building of a railway line. It can force you to give up your business to the government. That is, nationalisation is entirely legal under both domestic and international law. However, that right to property part also means that the government must pay full market value for that property that it is taking (and the Americans have it even more anchored in their law as "a taking").

This is of course as it should be. If the value of that railway line, that nationalisation, even that imposition of plain packaging, is sufficiently large in the national interest then there must be, from the value added by the scheme to make it sufficiently large in the national interest, enough to compensate the original values of the properties. Moving an asset from a lower to a higher valued use is the very defintion of wealth creation after all: so, if we are indeed adding that value then some can be used to compensate.

This argument also works in reverse: if there is not the value being added to compensate those original owners at that original price then the scheme is not in fact value adding. If that plot of land as a place for a house is worth £200,000, but it's only worth £20,000 as part of a railway line then that railway line is not value adding: it is value subtracting, thus something that makes us poorer.

So too with plain packaging. We've no idea whether the £11 billion is a realistic number or not: but we do insist that if plain packaging is in fact value adding then it must be possible to compensate those having their property confiscated to reach that goal. Otherwise, if the value isn't there, then the scheme itself is not value adding. If that's true, then why are we doing it?

Which is one of the values, over and above the civil liberty of secure property rights, why such a legal position is so useful. It insists that those who talk up the value of a scheme actually have to prove, by providing the cold hard cash, the value of that scheme.

The second point is about those tribunals and so on. Given that these rights already appear in UK domestic law there's nothing to fear from our signing a treaty that also includes them. It would be like our signing a treaty that insists that murder is a crime. Yes, we agree, so why not sign?

However, there are places out there not so blessed with a largely honest and largely reasonable legal system. And treaties are always reciprocal: what we agree to domestically the other side is also agreeing to in their domestic arena. So, the real value of the treaty (ies) is that it extends those rights which we have, as Britons, to those who have the unfortunate circumstance of not being Britons. And quite why this is a bad idea escapes us.

What excellent news about British social mobility

This isn't the way that anyone intends we should read this ONS report of course but it is also a true and valid way of reading it.

Almost a third of the UK population experienced income poverty in at least one year between 2010 and 2013, official data shows.The figures, published by the Office for National Statistics (ONS) on Wednesday, show that approximately 19.3 million people had a disposable income of below 60% of the national median at some point during the four-year period.

Word. And the actual ONS figures:

In 2013, the UK persistent poverty rate was less than half the overall poverty rate of 15.9%. By comparison, in many other EU countries, the persistently poor make up a higher proportion of those in poverty.

Since 2008 (the first year for which comparable EU longitudinal data are available), the UK has consistently had a persistent poverty rate lower than the EU average.

Almost a third (33%) of the UK population experienced poverty in at least one year between 2010 and 2013, equivalent to approximately 19.3 million people. In contrast, across the EU as a whole, a quarter (25%) of people were in poverty at least once during that period, with a larger proportion of people in the UK experiencing poverty at least once over those 4 years than in many other EU countries.

Worth noting one point: this is relative poverty. So, it's against median income. Further, it's against median income in each country. So we are not, not at all, stating that people in Britain have a lower living standard than those in, say, Romania.

Note first that that persistent poverty is half the average rate. That's pretty good, don't we think? And note also something else. Britain has greater variability in poverty. Variability in income is also known as economic mobility (or as the phrase has become these days, social mobility). For us to have more people who slip into poverty for a time, but not have more people in poverty overall, means also that more Britons must rise up out of poverty. That is, we really do have greater social mobility.

We doubt very much that anyone else will make this point.

Discrimination and the free market: hardly a piece of cake

We read this week that a judge has ruled that a Christian-run bakery discriminated against a gay customer by refusing to make a cake with a pro-gay marriage slogan. I’m uncomfortable with this particular legislation. Some people have been claiming that such a ruling is a victory for anti-discrimination proponents. The irony seems lost on them – that there is still discrimination going on – it’s just that in this case the discrimination is against the Christian couple running the cake shop. The Christian couple’s view on homosexuality isn't one I share, but I defend their right to choose to run their business according to their own religious beliefs and values, and in this case the State should do likewise.

Disapproving customers are free to walk away and shop elsewhere. They are even free to share their disapproval on social media and encourage others to join them in shopping elsewhere. Such responses are powerful in business, because they put pressure on socially undesirable behaviour, and they penalise discriminatory business owners with lost custom, diminished profits, and in extreme cases, bankruptcy.

Any law that makes it illegal to run a business according to your religious beliefs is a law that infringes on the liberties of the business owners in a way that is, in my view, socially undesirable. Saying that, however, doesn’t mean I think all anti-discrimination laws are undesirable - far from it. They just need to be applied more prudently.

As always, society involves tension between a) accommodating people's right to hold views and beliefs, and b) protecting others from unwanted discrimination. It is probably socially desirable for a racist café owner who wants to put a 'No Blacks' sign on his door to be forced not to discriminate. But at the other end of the spectrum it is also socially desirable for another café owner to be allowed to discriminate against under 65s by offering a pensioner discount on Wednesdays and Thursdays. In this case, I prefer the café owner's right to introduce pensioner discounts over any societal claims that under 65s are being discriminated against.

The question the cake shop case elicits is where on that spectrum do religious views sit? I think people's religious views should not be legislated against in business such that their freedoms are encroached upon in ways that are unacceptable. It's quite clear to me that if the choice is between a) forcing a businessperson to make/sell a good they do not wish to, or b) compelling a dissatisfied customer to use another business, it's a no-brainer that society should prefer the latter. A law that effectively wants to commandeer someone's bodies and cake-making facilities is to me far more repugnant than the offence these Christian bakers are supposed to have committed.

One final point: the market does a very good job of weeding out discrimination. Suppose racist Jim opened up a shop in 1960s apartheid South Africa but wouldn't serve any of the majority blacks - he obviously shoots himself in the foot because his restricts his trade options to a minority few and excludes the majority of potential customers.

In short, in a free market it pays not to unfairly discriminate, because whether on large scale or a small one you're going to limit your potential custom. The more socially undesirable your discrimination, or the more people your discrimination negatively impacts, the worse it will be for you. It is no coincidence that the time at which humans started to trade was also the time that we started to become more civilised and improved our methods of co-existence.

To be able to trade in any age, and in particular, the modern age, you need to be able to think of others; firstly, by coming up with something (goods, services, entertainment) that others want; and secondly, by being honest, ethical, friendly, and developing a good reputation for your business. Far from being a vortex of selfish, uncaring and unethical behaviour, free markets necessitate qualities that make trade conducive, with your success dependent (in most cases) on your being a reputable person who welcomes all and treats everyone well.