What tax dodging?

It's somewhat unlike us to come to the aid of any politician at all but we do think that this David and Ian Cameron story has got just a tad out of hand. As far as anyone can tell from the information we've got the allegation seems to be that Ian Cameron checked with lawyers to see that he was obeying the law. And David Cameron has, as his father did, obeyed every jot and tittle of said law.

That we live in a country where the powerful do indeed obey the law is something that we should all be rather happy about we feel.

As to the details of the arrangements Jerry Hayes tells us this:

Today I can tell you the truth about Blairmore Holdings. Not from any contact in Number 10 nor any friend of Cameron, but an old friend who is one of the leading tax specialists in London. This is not his opinion, it is a set of facts. This is what he texted me. I put it in direct quotes to show that I am not putting a personal spin on it.

“Blairmore Holdings was a perfectly legitimate offshore investment fund. It’s underlying investments were very largely if not exclusively non UK. The fund was registered with the UK revenue as a ‘distributer fund’ which meant that it had to pay out to investors at least 85% of its income each year. The investors would be liable to UK income tax on those payments if UK resident. Equally, if they sold their investment they would be liable to capital gains tax”

So we know that the fund was legitimate. Question one. Was Ian Cameron a UK resident? Yes. Was David Cameron a UK resident? Yes. This really is a no brainer. Their can be nor could have been any possible tax be benefit under this fund for the Camerons. End of story.

That "men pay taxes due" becomes a film at 10 story makes us concerned for the metal health of society as a whole.

It's necessary to understand the details when discussing the steel industry

Of course, it's necessary to understand the details when discussing anything at all as well. Which is precisely what Gareth Stace does not do here. Stace being the head of UK Steel, the industry association.

Of course, it's necessary to understand the details when discussing anything at all as well. Which is precisely what Gareth Stace does not do here. Stace being the head of UK Steel, the industry association.

In recent weeks we have seen further losses and we are now in a position where a substantial section of what’s left of the steel industry is up for sale. The big question now is how we ensure that everything that can be done is being done by all parties - the Government, businesses and the unions – to support the future of steel-making in Britain, and the successful sale of Tata steel’s assets.

Politicians of all persuasions have spoken of the importance of the steel industry as a national asset, and a strategically important part of our manufacturing capability. Ministers are right to say the steel industry is strategically important and the foundation of many of the UK’s most important manufacturing supply chains, including aerospace, automotive, defence and construction. Steel is used in every part of modern day life, from the building you are sitting in to the car you drive.

It carries on like that for the rest of the piece: steel's great, wonderful, save our steel. And at no point at all is the important underlying issue mentioned here. The British steel industry is indeed going through some tough times. But there's both a cyclical element here and also a structural one. That structural one being the one that both has to be considered and which Stace is glossing over.

This is: should we "save" the Port Talbot blast furnaces when blast furnaces are, to a great extent, a 19th century technology now surpassed by the 20th century one of arc furnaces?

This is the issue under discussion: for we've people lining up to purchase (at current rock bottom prices of course) rolling mills and the other downstream accoutrements of the industry. And absolutely everyone who has expressed an interest in doing so has said that the blast furnaces have got to go.

What does slightly irritate is that one of us has been on the radio with Stace a couple of times now and made exactly this point to him. We would therefore hope that it would be one that he might address: but of course as a lobbyist that's not quite what he's going to do, mention something not quite helpful to the case he is lobbying for.

FCA in Wonderland

The Financial Conduct Authority’s latest attempt to justify its own existence should be datelined 1st, not 5th, April. Their 2016/17 Business Plan is primarily addressed to risk. For example, the Chancellor’s decision to allow pensioners to spend their own money carries the risk that they will not do so as the FCA would like them to do. This is clearly intolerable. Fortunately “Our intelligence-led [sic] approach allows us to bring together information both externally derived and from across the FCA to develop a cohesive view of the risks, issues, challenges and opportunities in a particular sector, viewed through a number of different lenses.” (p.12) Not a lot of pensioners can do that.

These lenses do not seem to include the problem the FCA itself has created by driving so many Independent Financial Advisers out of business and thereby depriving future pensioners of the advice they need. They do, however, recognise that their hounding of banks and others, e.g. for mis-selling, has led to larger financial institutions “de-risking” their products, thereby reducing consumer choice and competition.

“We know that de-risking by banks is causing problems for some groups of consumers. While we do not control this process, we are undertaking work to help address the issue. We will complete our de-risking impact assessment in Q1 2016, giving us a clearer picture of the nature, scale and drivers of de-risking. We will work with Government, firms and others to create a proportionate strategic response.” (p.27).

The word “strategic” in that does not accord with the FCA’s continuing efforts to micro-manage the sector. The strategy we need is to return the sector to being a normal competitive market with brands, variety, innovation and consumer choice. By all means let us have a Which?-type organisation to critique and compare offerings and of course the financial sector should be included within the remit of the Competition and Markets Authority (CMA) to ensure fair trade. What we do not need is non-stop fiddling with detailed rules no one understands.

The risk-averse FCA 2016/17 plan contrasts with the speech of 6th April by Alex Chisholm, CEO of the CMA. The latter is broad in concept, technologically up to date and welcoming of innovation.

UK financial services are less at risk from Brexit, or remaining in the EU, than from the FCA’s preoccupation with risk, much of it created by the FCA itself. The only strategy it needs is self-immolation.

Legally Bonged: Why The Psychoactive Substances Act should go up in smoke

Cannabis is the biggest player in the EU drugs market, outstripping cocaine and heroin to snatch up 38% of the estimated 24 billion euro industry, and yet the UK police force have this week revealed under a Freedom of Information request that their officers are making half the arrests for possession they did five years ago.

Despite arrests dropping from 35,367 in 2010 to 9,115 arrests in 2015, consumption has stayed stable at around 7% of the population during that period.

Numerous studies have shown, including one from the Home Office back in 2014, that it is not clear that decriminalisation has an impact on levels of drug use and that decriminalisation can significantly reduce the burden on criminal justice systems. With Durham police admitting that they are no longer targeting or investigating cannabis users “so as to free up staff to deal with things that are more important” you should rightfully question why yet another restrictive drug law was planned to come into force today.

The Psychoactive Substances Act, whose debut was scheduled for today, would make it an offence to produce, supply or offer to supply any psychoactive substance if it is likely to be used for its psychoactive effects and regardless of its potential for harm.

However, the legislation has been delayed as the European Monitoring Centre for Drugs and Drug Addiction (EMCDDA) warned that it was unlikely the Act would go any way towards stemming the flow of designer drugs onto the market, partnered with continuing confusion about what the term ‘psychoactive substances’ actually covers and a worry that under the current definition of a psychoactive substance, or lack of, the Act is not enforceable by the police.

We urgently need an honest discussion of the law’s limitations. Our ABC classification system is far too simplistic, failing to differentiate between drugs in terms of overall harm or addictiveness, with extremely harmful drugs like heroin grouped together with ecstasy, which is statistically less dangerous to users than horse riding.

Beyond the limitations of imposing our drug laws, drug prohibition hands criminals an underground market worth over £200bn annually worldwide, and is responsible for deaths of thousands of people every year.

Just as incredibly destructive drugs like crystal meth and crack cocaine emerged from a clampdown on less risky drugs, so legal highs fill a void for the recreational drug user. A 'blanket ban' on psychoactive substances may eliminate high street 'head shops', but will push trade underground and encourage a slew of new, even more dangerous alternatives.

The fact that everyday substances like caffeine, alcohol and tobacco will be covered by such a ban (and have to be exempted) just shows how all-encompassing and heavy-handed such an approach is. To reduce harm from drug use the government should instead legalise recreational drugs like cannabis, ecstasy and cocaine so they are available with rigorous safety controls. This unworkable new Act will merely push the industry further into the dark, and frankly they’d be wise to put it in their pipe and smoke it.

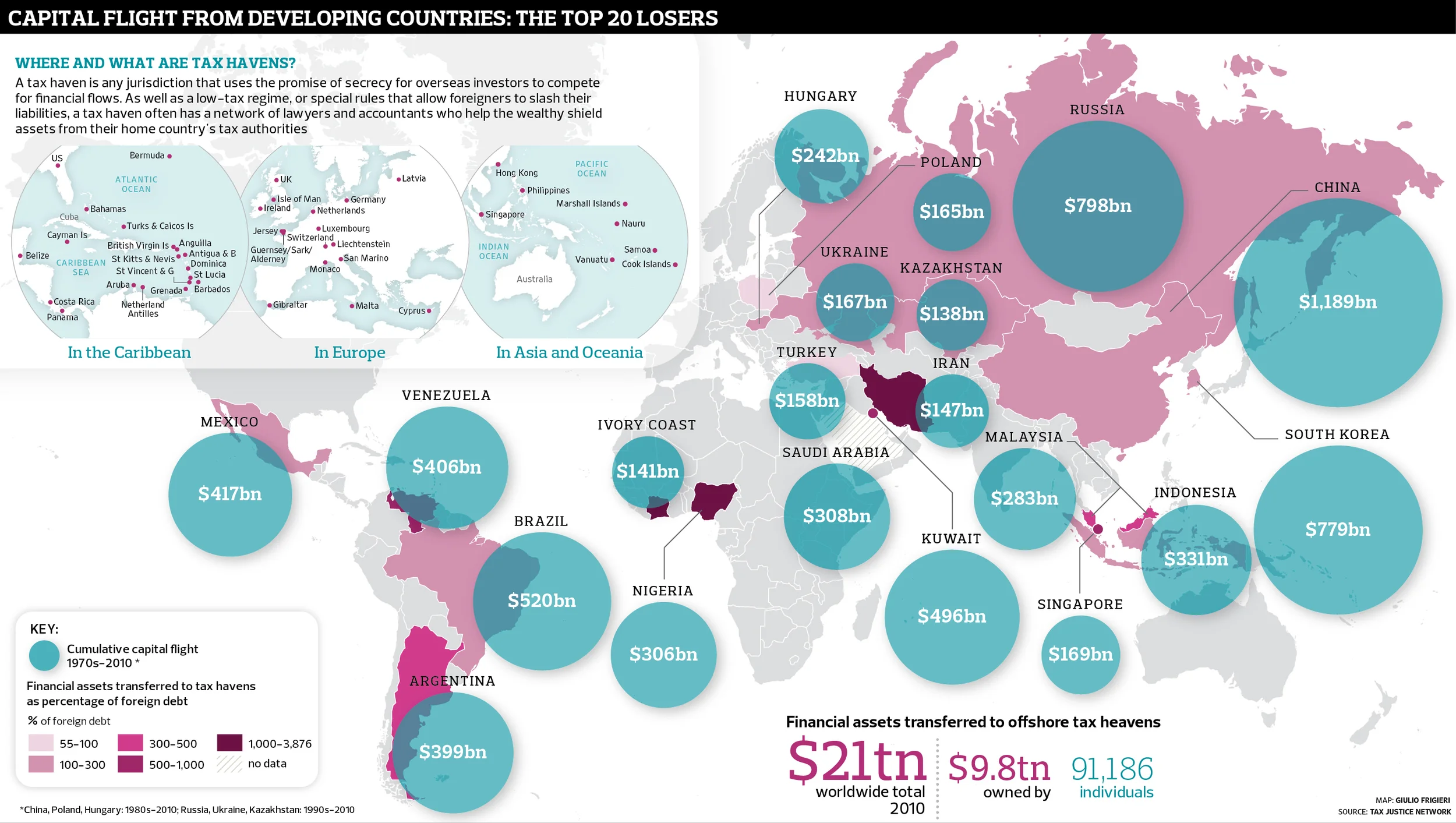

People are losing their minds over Mossack Fonseca

Or perhaps we can take this as evidence that The Guardian lost its collectively long ago:

Or perhaps we can take this as evidence that The Guardian lost its collectively long ago:

David Cameron’s father ran an offshore fund that avoided ever having to pay tax in Britain by hiring a small army of Bahamas residents – including a part-time bishop – to sign its paperwork.

Ian Cameron was a director of Blairmore Holdings Inc, an investment fund run from the Bahamas but named after the family’s ancestral home in Aberdeenshire, which managed tens of millions of pounds on behalf of wealthy families.

Clients included Isidore Kerman, an adviser to Robert Maxwell who once owned the West End restaurants Scott’s and J Sheekey, and Leopold Joseph, a private bank used by the Rolling Stones.

The fund was founded in the early 1980s with help from the prime minister’s late father and still exists today. The Guardian has confirmed that in 30 years Blairmore has never paid a penny of tax in the UK on its profits.

Just ponder on that for a moment. It is now a news story that a not British firm, which did not operate in Britain and does not, which is not resident in the UK, domiciled in the UK, has no permanent establishment in the UK, did not and does not pay tax in the UK.

Err, yes, yes. That bloke selling tea outside the mosque in Samarkand is also blissfully free of forcible contributions to the British state, that burger stand in Trenton NJ seems similarly unburdened, sales and purchases of breadfruit on Caribbean islands do not contribute to the British government's advertising budget in The Guardian. There is no reason at all why a non-British firm on some Caribbean island which sells investment advice should be contributing either.

British taxpayers who receive an income from such a firm should of course be, under the current rules, paying British tax. As they do if they own some business which sells tea in Samarkand, burgers in New Jersey or breadfruit anywhere. But no one is suggesting that those who should have been have not been. We just have the "news" that "not British business does not pay British taxes" and we're all supposed to be outraged.

It's just possible to start believing that people are losing their minds over this offshore tax matter.

Haven Is A Place On Earth

The BBC is making (not reporting) the news again, to the delight of high-taxing politicians. The fact that some chum of Putin has parked (presumably) ill-gotten millions in Panama provides a convenient excuse to close down low-tax jurisdictions. And the idea that rich folks like David Cameron’s dad save tax by sending their cash abroad stimulates enough public envy to provide the support.

The two are different, of course. Theft, fraud, tax evasion and money-laundering are rightly illegal: any firm or country that helps mafia bosses or dictators conceal stolen millions should be exposed and punished. But if you work within the rules and find ways to cut your tax bill, or invest your money in some place where it won’t be taxed within an inch of its life, that is legal and should remain so. Indeed, low-tax jurisdictions act as a safety valve that makes it harder for politicians to oppress their citizens with crippling taxes.

But it is too easy for those politicians to lump together the illegal evasion with the legal avoidance and say that both should be swept away.

In fact, criminals generally launder money at home, because it's far riskier to move it across borders; tackling that problem should start at home. The stock in trade of the low tax jurisdictions is actually ordinary people who put their modest lifetime savings into a respected insurance company based in Jersey, or the Isle of Man, or Luxembourg, or Switzerland. Then their savings can grow without being constantly eroded by the tax authorities.

That is why politicians hate them. They know that if other places have lower taxes, people will move their money (or their businesses, or even themselves) abroad – so their citizens can no longer be taxed with impunity. It’s pure tax protectionism: governments don’t produce widgets, so they are all in favour of free trade in widgets; but they do produce taxes, so they want to keep out the competition.

Low taxes encourage enterprise, investment, growth and freedom. So low-tax jurisdictions don’t need to flout the rules, and it is insulting to suggest that they do: in fact, many have financial sectors that are better regulated than ours. Rather than try to bully them out of existence, the big countries should ditch their tax protectionism, square up to the competition, lower and simplify their own taxes.

Can prediction markets replace politics?

Marc Andreessen, the Silicon Valley entrepreneur who co-founded Netscape, points out that markets don’t seem to be adjusting prices to reflect future costs from climate change.

Premium coastal vacation real estate prices are skyrocketing, he says. It's an interesting point that suggests that markets may think the dangers of climate change are overblown, although it’s important to try to compare this to the counterfactual. Maybe they’d be even more expensive if climate change wasn’t happening – or maybe there’s a scramble of demand for them now, so people can enjoy them before they're underwater!

But markets can be good ways of predicting the future. To the extent that they are a form of betting on the future, they can be a ‘tax on bullshit’:

I am for betting because I am against bullshit. Bullshit is polluting our discourse and drowning the facts. A bet costs the bullshitter more than the non-bullshitter so the willingness to bet signals honest belief. A bet is a tax on bullshit; and it is a just tax, tribute paid by the bullshitters to those with genuine knowledge.

As this paper outlines, markets generate good predictions for three reasons:

First, the market mechanism is essentially an algorithm for aggregating information. Second, as superior information will produce monetary rewards, there is a financial incentive for truthful revelation. Third, and finally, the existence of a market provides longer-term incentives for specialization in discovering novel information and trading on it.

The empirical evidence (outlined in that paper) is that markets generate good predictions for these reasons, and are difficult to manipulate – even if someone is willing to spend a lot of money to bet on a particular outcome, other participants’ judgment about the outcome will not change, and there is a significant profit opportunity for them to bring the price back to the equilibrium level. Of course they’re not infallible – good incentives cannot always overcome sheer ignorance – but at least when people are wrong there, they lose out.

Futures markets are essentially large-scale betting exchanges for predictions about the future, aggregating all the individual bets people are willing to make. So to scrape out the confounding factors in the example Andreessen gives, why not set up a pure futures market on climate? What will the average global temperature be by 2030, 2040, 2050 and so on?

Here there may be a role for government. It would be very socially useful to know what the aggregated best guess about global temperatures in 2050 is, but there isn’t any demand for this so far. There are not enough 'noise traders', who subsidise other futures markets by betting stupidly, for our fantasy climate markets to exist.

So, in order to generate enough volume for the market to be worthwhile, we need to subsidise it: the government pays a premium on top of the standard, market-driven pay-off for winning contracts when the time comes. This may cost several million pounds or even more – a small fraction of the current climate change budget.

We could use this for other purposes as well. Scott Sumner has long advocated an NGDP futures market so that central banks can target the monetary policy variable that really matters, for instance. And we could set up ‘conditional’ markets on policy questions too: “if the government cuts disability benefits this year, how many more people registered as disabled will be below the poverty line next year?” If the government doesn’t do the cuts in the end, all bets are cancelled, so we have a reliable 'what if?' window into the future.

Heck, if we could agree on some end-goal everybody wants, like average wealth levels weighted by the wealth of the bottom decile with red-line rules about freedom of speech and so on, we could replace the legislature with conditional markets. (We could hold regular referendums on what this 'end-goal' should be.) Robin Hanson calls it futarchy. Anyone could propose a policy, and if conditional markets implied that it would raise long-term wealth levels (or whatever we said the end goal was), it would become law.

It’s far-fetched, perhaps, but if it meant we could abolish politics I wouldn’t bet against it. I guess that makes me a noise trader.

How to solve the obesity crisis: turn the central heating down

We have long been, well, how to say this, umm, somewhat unconvinced, of the standard explanations for rising obesity. As we've mentioned just recently, that more people seem likely to die in some decades from popped fat pustules is less of a problem than our older now solved problem of people dying next week from lack of food. But it is still true that rampant obesity, if for no other than aesthetic reasons, isn't to be greatly welcomed.

Yet we just cannot bring ourselves to believe the standard explanations. That it's all to do with increased sugar consumption is obviously nonsense given that sugar consumption per capita has been falling. That it's about increased calorie consumption is also obviously wrong: the average diet today is lower in calories (and significantly so) than the standard WWII ration at which weight would be lost. So, it must be some other cause here, something else is going on.

We have leapt from there to the idea that the major use of energy in mammals is maintaining body temperature. Something of a leap to be sure but that epidemic of obesity is at least correlated with the widespread adoption of central heating across time and countries.

Now we learn that our leap is not simply fanciful:

Elderly adults are bigger around the middle when they turn up the heat inside their homes during the cold season and have smaller waistlines when their homes stay cool, new research finds. Investigators from Japan presented their study results Friday at the Endocrine Society's 98th annual meeting in Boston.

"Although cold exposure may be a trigger of cardiovascular disease, our data suggest that safe and appropriate cold exposure may be an effective preventive measure against obesity," said the study's lead investigator, Keigo Saeki, MD, PhD, of Nara Medical University School of Medicine Department of Community Health and Epidemiology, Nara, Japan.

Cold exposure activates thermogenesis, to generate body heat, in brown fat. This type of fat is the good calorie-burning fat that prior research found most humans have. However, Saeki said the association between the amount of cold exposure and obesity in real life remains unclear.

We can thus junk all the currently fashionable nostrums. It's not killer sugar, not the food industry ramming doughnuts into our gobs, all that is required it to turn the central heating down. Sure, there's no plaudits to be won in fighting against The Man here, no tax revenue to be collected, no social justice warriors to be employed in 5 degrees today outreach. But it does have the advantage of being consistent with the empirical evidence we have.

We're eating less, consuming less sugar, keep our homes much warmer than ever before and are getting fat. Given the increase in weight it's likely to be the thing that we've increased, not that we've reduced, to blame.

Logical, evidentially supported, it'll never catch on as public policy, will it?

The question is not how to save Port Talbot but whether to

There's an excessive amount of thrashing around being done over the question of Port Talbot and the Tata steelworks there. And there's very few managing to ask the right starting question. Which is not "How will we save Port Talbot" but rather "Should we save Port Talbot?"

There's an excessive amount of thrashing around being done over the question of Port Talbot and the Tata steelworks there. And there's very few managing to ask the right starting question. Which is not "How will we save Port Talbot" but rather "Should we save Port Talbot?"

As many are pointing out, there are indeed times when government can and should step in to "save" something: an industry, a system, perhaps even a company. As many are again pointing out a few years ago much was done to stop the financial system collapsing into a heap of smoking rubble. If that and then, why not this and now? Do though note that not all of that financial system was saved, rescued nor did we even try to do so. Lehman, Northern Rock, the Dunfermline, Chelsea and other building societies, Alliance and Leicester slightly differently, all were allowed to go their own way into distress sales or outright bankruptcy. Even in such extremis we did indeed select between those who needed to be saved and those who did not (our own opinion being that rather fewer of those who were saved should have been so but that's another matter).

Which brings us to that Port Talbot plant. Various people are muttering various things about which bits of the business they might like to take over. But all are saying the same thing about the major plant at the heart of it all, the blast furnaces on the site. No one wants them. And the truth of it is, as one of us has been saying for near five years now, that the world simply needs fewer such plants for we all recycle much more steel now than we used to. Recycling happening in an entirely different technology, arc furnaces. Well over 50% of Europe's steel comes from this process now. And there's not really any good argument as to why blast furnaces should be in the UK either. Sure, there are some times when entirely new, virgin, steel is necessary but we import the coking coal, the iron ore, to make that at present. There is no good reason why we should import the raw materials and lose £1 million a day processing them instead of just importing the virgin steel itself.

Which brings us to a good example of that thrashing about:

The scale of the challenge, though, means that no private investor is likely to be willing to take on the entirety of the risk. We need other investors to bridge that gap, but this investment could come from a range of sources and take a multiplicity of forms. Tata’s environmental liability – which could run to as much as £1bn at Port Talbot alone – converted into an “exit dowry” could be reinvested by the Welsh government as an equity stake in a new joint venture company. The workforce could do the same, perhaps via Tata’s contribution to the pension fund deficit, trading accrued rights for employee shares. Local authorities could invest through the City Deal in a research and development centre for new hi-tech steels or the kind of process and business model innovation that Liberty Steel’s Gupta has promoted as a possible medium-term solution.

The UK government could also become a stakeholder, perhaps holding the heavy-end blast furnaces as a strategic asset – or, if its ideological aversion was too strong, simply providing very large, very long-term and very soft loans.

What is strategic about holding something that no one wants to use? What is asset-like about something which has a negative value? And look at the financial prestidigitation being suggested there! The debts for the environmental clean up are to be declared an asset, pensions are to be converted into equity in an asset that has a negative value and the taxpayer invited to spray cash all over the result as a beneficience.

This is not sensible. We must ask the correct question in the first place. Is there any good reason to "save" a blast furnace in the UK today? We would say no, others might differ in their views on that. We do have the advantage that we actually understand the technology of the steel industry but we would not claim omniscience on this specific point.

However, we are entirely adamant that that is the first and important question to be asked and only an answer to that then leads to what should be done next. And sadly, as far as we can see, we're the only people actually asking that question before some billions of your and our money is sprayed around to quite possibly no good purpose.

We'll chalk this up as a victory for free markets, capitalism and globalisation then

The Lancet tells us, in shocked and disapproving tones, that there are now more fatty lardbuckets on the planet than there are undernourished people. We simply cannot bring ourselves to think of this as being a bad thing. Rather, we consider it to be a massive victory for the economic policies of the last few decades. A victory for capitalism, free markets and globalisation.

The Lancet tells us, in shocked and disapproving tones, that there are now more fatty lardbuckets on the planet than there are undernourished people. We simply cannot bring ourselves to think of this as being a bad thing. Rather, we consider it to be a massive victory for the economic policies of the last few decades. A victory for capitalism, free markets and globalisation.

There are now more adults in the world classified as obese than underweight, a major study has suggested.

The research, led by scientists from Imperial College London and published in The Lancet, compared body mass index (BMI) among almost 20 million adult men and women from 1975 to 2014.

It found obesity in men has tripled and more than doubled in women.

Lead author Prof Majid Ezzat said it was an "epidemic of severe obesity" and urged governments to act.

It's possible that action is required or even desired. But first we should have a little pause for celebration, a few turns of that victory dance. As the paper itself says:

Implications of all the available evidence

The world has transitioned from an era when underweight prevalence was more than double that of obesity, to one in which more people are obese than underweight.

So what, actually, has happened? Well, the essential heart of it is that we all started buying stuff made by poor people in poor countries. This made them richer and led to the solution to what PJ O'Rourke has called the species-long human problem: what's for lunch? Closely followed by that other rather already solved one, how do I not be lunch?

That history of our species has been the struggle to try and work out how to gain enough calories to see the next day: as it actually is for all other species. We're the one that has worked out farming, economy, trade, to solve it. And we're here in this happy day when it is actually all coming to fruition.

Consider what is the complaint. Instead of people dropping dead of starvation next week we're now facing the idea that people might drop dead in a few decades or more from an excess of food availability. That second, in and of itself, may not be all that desirable an outcome. But compared to what went before we do indeed insist that this is a vast, joyous, victory.

So, happy dance! With, of course, lashings of ginger beer, burgers, milkshakes, fries, donuts, ice creams and syrup covered waffles to sate the appetites so created.