The problem is that what Trevor Nunn believes about inequality isn't true

Trevor Nunn is touting this new play he's involved with which is - wait for it - on the subject of the gross inequality of today. The problem being here that what he believes about inequality just isn't true.

And yet, even in our enlightened social democratic western world, we remain utterly unequal – probably more so now than at any previous time.

This simply isn't so. Not in any sense that matters of course. It's well known that two of the three richest people on the planet, Bill Gates and Warren Buffett, are partial (Lord knows why) to a Big Mac on occasion. There are almost none of us in the rich world who do not have equal access to those. Nothing by Maccy D's might not be healthy but it's financially out of reach of very few of us. And it's extremely doubtful that this has even been true before, that the entire society has equal access to the food desired by the richest. The plebes didn't get access to those lark's tongues after all.

That is, of course, being tendentious, as is pointing out that we've all entirely equal access to Facebook and WhatsApp on the same terms.

Yet when we do these calculations properly, as the TUC once did, we do indeed find that the only form of inequality that matters, that of consumption, is low, very low. Using quintiles of households the TUC found that the 5 th (ie, the top) earned 12 times the 1st. After we subtracted taxes, added benefits, levered in the value of public services like the NHS and education, the consumption inequality came down to 4 to 1.

It is extremely difficult to think of any previous version of human society which was as equal as this.

Not that the inequalities which remain are also of rather less import. Not too long ago poverty meant no shoes, now it means off brand sneakers. Inequality meant empty bellies, unto the point of death - yes starvation existed in England up into the 19th century. Now such inequality, or if you prefer, poverty,. appears to mean a greater propensity to obesity.

I have to presume that the motive for acquisition is competition: that driving force, that god in Margaret Thatcher’s universe, the market. Competition to defeat all your rivals, competition to be able to declare you have more wealth than anybody except Bill Gates, competition to get more than Bill Gates.

Which is also grossly wrong. Competition is what limits that wealth that can be amassed. Monopolists do tend to be rich, the competition from Steve Jobs, Linus Torvalds, Larry Ellison and all the rest is precisely what has limited the fortune of Bill Gates.

No doubt the play will be a success given how many share these delusions. But it is a delusion, we are more equal today than almost all human societies since the invention of agriculture.

The terrors of the patriarchy in tech

A worry expressed in The Guardian. AI more generally, the use of big data to train it more specifically, risks coding into the systems the attitudes of the current society:

But this can create problems when the world is not exactly as it ought to be. For instance, researchers have experimented with one of these word-embedding models, Word2vec, a popular and freely available model trained on three million words from Google News. They found that it produces highly gendered analogies. For instance, when asked “Man is to woman as computer programmer is to ?”, the model will answer “homemaker”. Or for “father is to mother as doctor is to ?”, the answer is “nurse”. Of course the model reflects a certain reality: it is true that there are more male computer programmers, and nurses are more often women. But this bias, reflecting social discrimination, will now be reproduced and reinforced when we engage with computers using natural language that relies on Word2vec. It is not hard to imagine how this model could also be racially biased, or biased against other groups.

Yes indeed, that will happen. If you train something (anything, this applies to guide or gun dogs as much as it does to a translation program) to operate within what exists then it will operate by the rules which currently exist.

The important part here being of course that part about the world not exactly as it ought to be. This starts to smack rather of New Soviet Man, that luscious planned economy would start working right around the time that we've changed humans so that they work within that luscious planned economy. Which isn't, quite, how it turned out, was it?

But perhaps it should be different this time? To which there is an answer, the answer being the same even as the questions differ. We use markets and competition to work this out. Some section of society would prefer to see all such structured genderism not incorporated into those AIs. Other (very few perhaps) would like to see more of it, most possibly just wanting it to reflect the real world not the dreamed one. All of which is absolutely fine. There is no shortage of capital out there, there are no legal of cultural constraints upon anyone building an AI absolutely any way they wish to.

We'll find out which people really prefer when they use the various available alternatives and, well, use them. That's what we've done with every other invention and innovation in history after all and look how much better off we are than those societies which didn't - New Soviets for example.

At which point:

Products that are more responsive to the needs of women would be a great start.

Well, get on with it then. For surely you're not insisting that the men should do it for you, are you?

Universities and incentives

Eamonn Butler's latest blog looks at Adam Smith's time at Oxford and Glasgow where he learned first hand that incentives matter - especially in Education.

On this day, in 1740, Adam Smith—who would later become the pioneering economist who authored An Inquiry Into The Nature And Causes Of The Wealth Of Nations, set off for Bailliol College Oxford. This young man from the rural port of Kirkcaldy on Scotland’s east coast had already distinguished himself as a student at the University of Glasgow and now, aged just 17, had won a scholarship, the Snell Exhibition, to attend one of the most distinguished centres of learning in the world. Or so it seemed.

It took the young Smith a month on horseback to get to Oxford from his home in Kirkcaldy. That in itself was something of a revelation to the budding economist. He had already noted how much grander and livelier was Glasgow, compared to his childhood home. Kirkcaldy’s export trade in coal and other goods was fading; the larger and safer harbours of Dundee to the north and Edinburgh to the south were better placed. And Glasgow, being the recently-unified Great Britain’s closest great port to the Americas, was developing a thriving trans-Atlantic trade in tobacco, cotton and other new goods. All the more so because of regulations that forced the colonies to trade only with Great Britain, and not its enemies and competitors in the Netherlands, France and Spain. But now, as he rode the 400 miles through the Borders and down through England, he was struck by the steadily increasing prosperity. The cattle were better fed, the living more opulent, than anywhere in his native Scotland.

Perhaps these experiences stimulated his interest in economics, though he had come to Bailliol to study the classics. Bailliol College, indeed, had what was reckoned to be perhaps the finest library in terms of classical authors, and Smith—an avid reader even as a schoolboy, and in later life a man of whom it was said he could never resist buying a book—would be in his element.

Up to a point. What Smith actually found at Bailliol was that few if any of the teachers had any interest in helping him further his education. “In the University of Oxford.” he would write much later, “the greater part of the public professors have, these many years, given up altogether even the pretence of teaching.”

Why? Well, it was Adam Smith’s first lesson in incentives. Oxford professors were paid whether they taught students or not. So why bother?

It was very different from Smith’s own experience, two decades later, when he himself taught at his other alma mater, the University of Glasgow. There, the teachers were actually paid by the students. So when Smith—by then a sort of intellectual rock-star thanks to the success of his book The Theory Of Moral Sentiments—was induced away from teaching his course, with the offer of a fabulous lifetime salary, to tutor the 12-year-old Duke of Buccleuch, he worked out how much he owed each of his students for the lectures he would miss, and prepared little pouches of money for each of them. But the students refused to take the refund, and mischievously put them back into his pockets. They thought they had already had great value, even with the course incomplete.

The difference in the two systems, and the incentive effects on the teachers, was not lost on Smith, and became a major theme in The Wealth Of Nations. “Public services are never better performed,” he wrote, “than when their reward comes in consequence of their being performed, and is proportioned to the diligence employed in performing them.”

Having exhausted everything the great Bailliol library had to offer, Smith returned home to Scotland a year earlier than planned. He had educated himself. Remembering the experience, he wrote: “The discipline of colleges and universities is in general contrived, not for the benefit of the students, but for the interest, or more properly speaking, for the ease of the masters.”

In the UK today there is a debate on whether universities should return to being free to students. In other words, teachers would get paid, by the state, just for being there. And the students, with no financial leverage over them, would have little way of punishing bad teaching. If we could ask Adam Smith, he would no doubt have much to say on that subject.

So just why are companies sitting on vast lakes of cash?

It's not an unusual complaint these days, companies sit on vast lakes, reservoirs' worth, of cash and don't seem to do much with it. Something must have changed so what is it? At least part of the answer, accounting for just under a third of it, is that the world of business has changed. Well, obviously, but we've identified one of the ways that it has:

I explore the role of the just-in-time (JIT) inventory system in the increase in cash holdings by U.S. manufacturing firms. I develop a model to illustrate the mechanism through which JIT affects cash and quantify its impact. In the model, both cash and inventory can serve as working capital. As firms switch from the traditional system to JIT, they shift resources from inventory to cash to facilitate transactions with suppliers. On average, this switchover accounts for a 4.1-percentage-point increase in the cash-to-assets ratio, which is approximately 28% of the change observed in the data.

Back decades a company might sit on months of inventory, today perhaps hours. That needs less working capital to finance the inventory of course, but also more ready cash to pay suppliers. What happens to the net investment position depends upon the balance of those two effects.

Our own guess at it, and it is a guess, would be that the reduced working capital demands outweigh the greater liquidity demands. Thus rather neatly explaining something else people seem to worry about, the decline in corporate use of capital itself.

There is also a larger point to make here, we must always be very sure that we are distinguishing cyclical changes from structural. It is possible, for example, that people might use corporate demands for cash or working capital as a measure of the state of the economy. OK, fine, why not do so? But when we do so we've got to make sure that as the underlying technology, and thus the structural demands, change we do not confuse the two, the structural and the cyclical.

Our favourite example of this error was a measure of business software investment. That this is static was used to argue that there was no great technological revolution going on and therefore we faced secular stagnation. The problem being that business increasingly rents its software, not buys it. Office and Office 365 both do the same thing, but Office is an investment, 365 a current expense. Business was indeed therefore "investing" more in software, by the amount of the size of the software as a service market, but this was completely missed by the use of the investment statistic.

Or, as we like to say, it's no use looking at an economic statistic unless you understand, in detail, what it is actually measuring and why

The Fiction of the ‘Great Capital Rebuild’

The central element of the Bank of England’s narrative on the UK banking system is the ‘Great Capital Rebuild’. To paraphrase Governor Carney’s comments when the 2015 stress tests were released: the post-Global Financial Crisis (GFC) period and the long march to higher capital are over. The message – which he has repeated since – is that UK banks are now more or less fully capitalised.

Unfortunately, the ‘Great Capital Rebuild’ is a fiction.

Let’s look at the evidence. Exhibit A is the following chart (Chart B.2) from the BoE’s November 2016 Financial Stability Report.

Major UK Banks’ Leverage Ratios

Sources: PRA regulatory returns, published accounts and Bank calculations.

(a) Prior to 2012, data are based on the simple leverage ratio defined as the ratio of shareholders’ claims to total assets based on banks’ published accounts (note a discontinuity due to introduction of IFRS accounting standards in 2005, which tends to reduce leverage ratios thereafter). The peer group used in Chart B.1 also applies here.

(b) Weighted by total exposures.

(c) The Basel III leverage ratio corresponds to aggregate peer group Tier 1 capital over aggregate leverage ratio exposure. Up to 2013, Tier 1 capital includes grandfathered capital instruments and the exposure measure is based on the Basel 2010 definition. From 2014 H1, Tier 1 capital excludes grandfathered capital instruments and the exposure measure is based on the Basel 2014 definition.

This chart shows some of the BoE’s own estimates of UK banks’ leverage ratios spanning 2001 to 2016: the leverage ratio is the ratio of some measure of capital to the total amount at risk. This chart indicates that UK banks’ leverage ratios are a little higher than a decade ago – maybe 25% on this measure, but certainly no multiple – and a decade ago the banks were on the eve of an almighty crash.

Now comparing leverage ratios before the GFC and after is a tricky business because of definitional changes made by Basel III. Yet the Bank itself publishes figures for two leverage ratios known as Simple Leverage Ratios (SLRs): the ratio of shareholder equity to total assets. One refers to the book value of shareholder equity and the other to the market value of shareholder equity. These series give average SLRs across the banking system and span the period from before the GFC until recently. [2] To the extent that we can rely on these to give us a before and after comparison, the average book value SLR was just under 4.1 percent in 2006 and 6.2 percent in the first half of 2016, representing an increase of 51 percent. [3]

The corresponding market value SLR was 8.0 percent going into 2006 and 5.28 percent in November 2015, representing a decrease of 34 percent. [4] By this latter measure, UK banks are more highly leveraged now than they were going into the crisis.

I would suggest that it would be prudent to pay attention to these market value figures: the market values being less than book values is a signal that the market perceives problems with the book values.

Then consider that the big four banks’ total Common Equity Tier 1 (CET1) capital was about £205 billion by the end of 2016q3. This figure is barely £90 billion higher than the £116 billion Tier 1 capital that they had going into 2007, although one must acknowledge that this £90 billion difference does not allow for the considerable improvement in quality between Basel II Tier I capital and Basel III CET1.

The 2016q3 £205 billion CET1 number is a book value figure, however, and the corresponding market value of its CET1 capital was about £149 billion.

We should also assess these numbers against the sizes of the banks’ balance sheets, and it is traditional to use Total Assets as such a measure. Given that their Total Assets were just under £5 trillion at the same date, their average CET1 leverage ratio (or ratio of CET1 capital to total assets) was 4.0 percent if we go by book values and just under 3 percent if we go by market values.

By the first measure, UK banks are leveraged by a factor of 1 divided by 4 percent or 25: they have £25 in assets for every £1 in capital; and by the second measure, they are leveraged by a factor of over 33. These are high levels of leverage that leave the banks vulnerable to shocks – and high levels of leverage aka inadequate capital were a key factor contributing to the severity of the GFC.

Putting all this together, the evidence for a ‘Great Capital Rebuild’ is not there – especially if one pays attention to the market value numbers.

As a further confirmation, Chart B.3 in the Bank’s November 2016 Financial Stability Report states that “Most capital rebuilding to date has reflected falls in risk-weighted assets” – a delightful piece of duckspeak – and then gives a breakdown of this ‘rebuild’ in terms of its constituent components. The rebuild it is referring to is not quite what it might seem, however: it refers to the rebuild in the banks’ average ratio of CET1 capital to risk-weighted assets (RWA) relative to 2009. Now the CET1 ratio was 6.92 percent in 2009 and had risen to 12.61 percent by end-2015. That increase breaks down into 0.45 percentage points in new equity raised, 1.02 percentage points in retained earnings and 4.22 percentage points in reductions in risk-weighted assets. Therefore, only 1.47 percentage points of that increase in the capital ratio represents actual increases in capital; the rest, the 4.22 percentage points decrease in risk-weighted assets merely reflects the decrease in the denominator. I would suggest that the chart should have stated “Most of the increase in the ratio of capital to RWAs to date has reflected falls in risk-weighted assets” but that doesn’t quite convey the same message. The increase in the capital ratio from 6.92 percent to 12.61 percent might seem impressive at first sight – an increase of 82 percent – but the actual capital rebuild was only from 6.92 percent to 8.39 percent, an increase of about 21 percent.

A big increase in a regulatory capital ratio is one thing, but a big increase in actual capital is quite another.

Let’s face it: the ‘Great Capital Rebuild’ is not there in the data.

[1] Kevin thanks Sir John Vickers for helpful inputs to this posting.

[2] These figures will overstate the leverage ratio and understate true levels of leverage because they use the larger Shareholder Equity measure rather a narrow core capital measure such as Core Tier 1 or CET1, but they give some sense of the trends over time.

[3] These figures are to be found on p. 57 of the Bank’s November 2016 Financial Stability Report.

[4] These figures come from the BoE Excel workbook ‘ccbdec15.xlsx, spreadsheet ‘9. Bank equity measures’ under the C column, ‘Market-based leverage ratio (%)’. This workbook was accessed on March 9th 20616 but appears to have been removed from the BoE website since the time I accessed and downloaded it.

Britain's very real Magic Money Tree

Britain has a real source of income lying unused.

Dr. Madsen Pirie, President of the Adam Smith Institute, has the solution.

The government faces a dilemma: it is under heavy pressure to row back on austerity without losing its hard earned reputation for fiscal responsibility.

Fortunately Dr. Madsen Pirie, President of the Adam Smith Institute, has come up with an idea that manages to bypass the objections that are seen of the classic ways of funding deficit spending: raising taxes, printing money, borrowing and the political problem of cutting tax to pursue growth.

A fifth way is to raise money from selling things.

‘This time it would mainly be land that was sold, partly land already owned by government, but overwhelmingly land acquired for the purpose.

‘Local authorities should be empowered to buy land in their areas, land without planning permission for development. They should be authorised to grant it planning permission, and sell it on for development.’

Read the whole paper relating to this idea here, and his words in the Telegraph here.

This is how it works, first you redefine poverty then you find lots of it

Over the decades the definition of poverty has changed, from meaning someone not having very much to someone having less than others. That move from measuring poverty to relative poverty turns it from a measure of actual poverty into one of inequality. The reason this was done is obvious, Britain abolished absolute poverty in the 1930s and where would the left be without something to whine about?

We are fortunate to be witnessing an attempt to again redefine:

More than a million people in the UK experienced destitution in 2015, including 312,000 children, according to a groundbreaking study by Heriott Watt University academics for the Joseph Rowntree Foundation published last year. It defined destitution in two ways: experience of at least two of six poverty measures over the previous month, including eating fewer than two meals a day for two or more days; or a weekly income after housing costs of £70 for a single adult or £140 for a couple with children. This was an income level below which people “cannot meet their core material needs for basic physiological functioning from their own resources”.

A definition of destitution which defines it as only two meals a day twice a month is rather co-opting a word with a very strong meaning to cover something really quite different.

We should also note, as we so often do, that this definition is before the things which people other than the state do to alleviate such distress.

What we are seeing here is an attempt to float another redefinition, like that to relative poverty measures, in order to show that there is some vast problem which needs more tax to solve.

Incentives matter, yea even unto death

The first and prime lesson of economics is that incentives matter - grasp that there are always opportunity costs and with those two you've got the basics of the subject nailed - and this extends even to the timing and manner of death:

A bizarre trend is said to be afoot in villages bordering the Pilibhit Tiger Reserve (PTR). Authorities suspect local families are sending older members into the forest as tiger prey, and their bodies then relocated to fields, to feign attacks and claim lakhs in compensation from the government.

Villagers aren't entitled to compensation if their kin die in the reserve.

Depending upon how large the compensation is this could be bizarre or not. Put a sufficient number on the head of dead grannies anywhere and elderly women are going to be at risk from their kin. But it is, allegedly at least, not the youngsters offing the elderly in the hops of a payout:

Locals, however, say family elders were willing participants in the whole affair. "They think that since they can't get resources from the forest, this is the only way their families can escape poverty," farmer Jarnail Singh, 60, told TOI.

We also have reasonable evidence that changes in tax law regarding estates can change the timing of death.

The lesson from this being perhaps uncomfortable for the more radical egalitarians among us. Assuming that tiger story is true some people are willing to quite literally sacrifice themselves for their children in just economic terms. Which means that it's really going to be very difficult indeed to reach a society in which parents do not actively conspire to privilege their own children over those of others. Even radical measures like 100% death taxes, a pure insistence upon absolutely equal schooling for everyone, we're still going to have people working to create that inequality.

A society without any form of inherited privilege just isn't going to work because humans ourselves just don't seem to work that way.

As Gary Becker pointed out, prejudice has costs for those who are prejudiced

Gary Becker pointed out that prejudice was costly to the person who was prejudiced. By refusing to hire perfectly reasonable workers just because of the colour of their skin this leaves the employer with less profit than they could have had. In time the knowledge will spread, that these now cheaper because of the discrimination workers are just fine and they will be hired by others less prejudiced. Again, in time for nothing is immediate in a market economy, the prejudiced will find themselves out competed and thus does that prejudice disappear from the workings of the economy even if not the minds of men.

It's worth noting that this was the reason for the Jim Crow laws. The prejudiced used the state to enforce what they knew the market would not.

This applies not just to race of course, it applies to any form of taste discrimination. Which brings us to something fun about the Venture Capital industry:

The vast majority of venture capitalists in the United States are men. But the distribution of women partners across VC firms is not uniform. It turns out that companies whose male senior partners have daughters are more likely to hire women as partners. And according to research published earlier this month by Paul Gompers and Sophie Wang, those companies secure superior investment returns — strong evidence that an irrational opposition to hiring women partners is holding VC firms back.

It is possible to devise reasoning as to why men are just going to be better at being a VC than women. It also seems that such reasoning would be wrong. So, why hasn't this been outcompeted then?

The answer being that "it takes time" bit. The market is a pretty wondrous human institution but it's only in the pages of the wilder textbooks that information is perfect or that things happen instantaneously. This is new information--and we know from the efficient markets hypothesis that markets are indeed efficient at incorporating new information into prices. We should thus expect rather more hiring of female VC partners and executives and thus the diminution of that prejudice.

Assuming the study itself is correct those that don't will lose out. And what the hell do we care about that? This is capitalism, recall, and people are entirely allowed to waste their money their own way. Those who continue in prejudice, once it has been pointed out to us all so that we react, will lose money. And what better way to punish a capitalist than that?

That is, we don't actually need to do anything other than to prove this very point, that this is taste discrimination, not rational. Once that is known we can confidently expect it to disappear--for exactly the same reason those Jim Crow laws enforcing discrimination existed. Once people know they're losing money they stop doing silly things if only the law will allow them.

Why post-truth Corbyn is wrong about tuition fees

Labour’s pledge to abolish tuition fees was the most memorable and (regrettably) popular policy of the last General Election. Unfortunately, it didn’t receive anywhere near the level of scrutiny it deserved, many outright falsehoods went unchallenged with Theresa May relying on the old ‘Magic Money Tree’ trope that might have worked at the past two elections, but clearly wasn’t enough here.

At Jeremy Corbyn’s post-election rally, he claimed that “fewer working class young people are applying to university. Let's end the debt burden and scrap tuition fees!”. Now I do not know if Corbyn is a cynical liar or merely incompetent – it’s entirely possible he’s both – but what he said was simply not true.

Since tuition fees were brought in the number of disadvantaged students, as measured by eligibility for free school meals, applying to university has actually increased. As Jo Johnson, the Minister for Universities, points out – disadvantaged young people are actually 40% more likely to apply to university now than in 2010.

Of course, you might wonder whether we’d have even more disadvantaged young people going to university if we’d abolished tuition fees altogether. That’s a perfectly reasonable claim. It just so happens to be false.

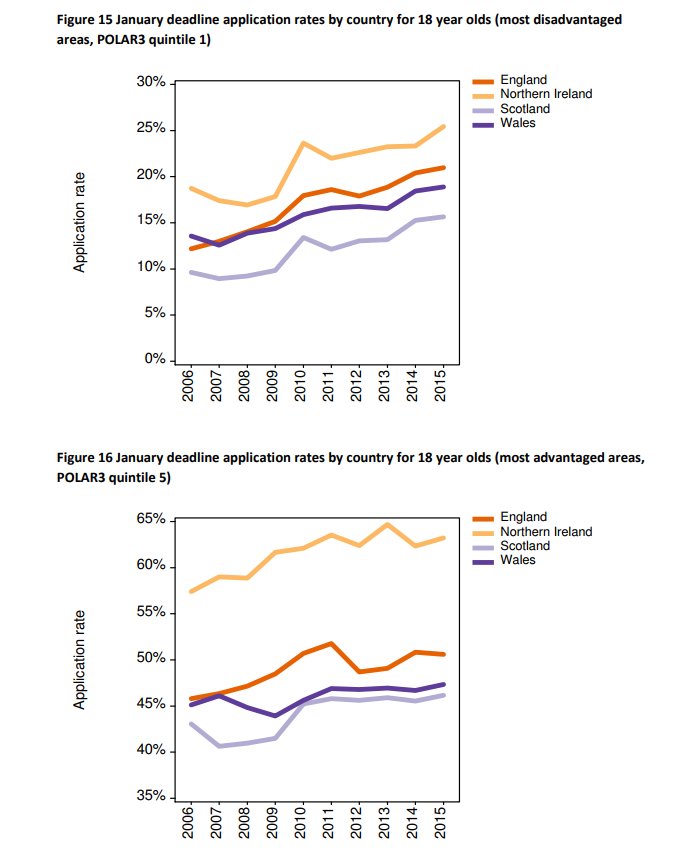

Scotland, where tuition fees have been abolished since 2007, provides us with an excellent natural experiment. Are we more likely to make progress on getting disadvantaged young people to apply to university with fees abolished? The answer is no.

In 2007, Scotland used to do about as well as England at getting young people from disadvantaged areas to university. But if you track a graph from 2007 to 2015, you see that both nations get better at encouraging students from poorer areas to apply but England does substantially better and the gap between England and Scotland is larger today than it was before fees were abolished.

{kind=link}

Interestingly, if you take the same graph but look at young people from advantaged areas instead, you get a very different result. Applications rates for the well-off fell since tuition fees were tripled in England, while they increased for the well-off in Scotland.

If your goal is ensuring that anyone who wants to can go to university then abolishing tuition fees simply won’t work.

Advocates of free tuition typically ignore this evidence and instead frame their arguments in terms of fairness. But there’s nothing fair about free tuition.

Abolishing tuition fees would cost £11bn coming out of general taxation. In other words, people who didn’t benefit from receiving a university education and will most likely earn less than graduates will be forced to pay more in tax to fund well-off graduates. At a time, when we have a £50bn deficit, funding pressures on the NHS, schools and social care, and the highest tax burden in decades, is it really wise to fund a cash transfer that well-off graduates will benefit from the most?

But that’s not the only way it’s unfair. Privately-educated children are much more likely to attend university than children on free school meals. Abolishing fees doesn’t change that (as the evidence from Scotland shows), but it does mean that a greater share of public money will be spent on the children of the well-off.

Another argument that usually crops head up is the ‘public good’ argument. Now when someone says education is a public good they don’t mean it in the traditional economic sense, they mean it in the same way this confused Vox writer does. Essentially, they think that education is a good thing and it’d be better if we saw more of it because it benefits not just the individual but society as a whole. But that’s not an argument for higher education to be fully funded by the state. In fact, tuition fees were originally introduced to increase university funding allowing them to expand the number of spaces on offer. And raising fees to £9,250 a year enabled the government to lift the cap on university places allowing more people than ever to go. The ‘public good’ argument just doesn’t hold water.

The status quo isn’t perfect. We need to ensure that students really are getting value for money. That means equipping them with all the facts. Prospective students should have good quality information about how much they can expect to earn (and to repay) not just a few years on from university but 10-15 years down the line.

The 23 universities where graduates earn less than non-graduates should be named and shamed.

We should also look into broadening the options available to young people. Why not encourage universities to offer two-year degrees to attract students who don't want to pay full fees but still get a quality education?

Abolishing fees would be expensive and unfair, but it'd do nothing to resolve the real problems in higher education.