The Sec of State suffers a petty delusion

From MiliEd:

This deal will also help speed up the clean-energy transition globally, which is, crucially, right for Britain because of what it offers in terms of investment and economic opportunity, including exports. For us and others around the world, taking advantage of this transition is the route to good jobs, economic growth and higher living standards.

To beat on an old drum. Jobs are a cost of doing something, not a benefit of the thing being done. Creating “good jobs” is therefore creating costs by whatever the plan is. So too is investment a cost, for exactly the same reason. So cheering about the investment the plan requires is just highlighting the costs of the plan.

As to exports, we’re unconvinced. If everyone and their as yet uneuthanised Granny is subsidising these new technologies - as the recent COP just agreed everyone would - we do tend to think that the opportunity for profitable exports is going to be limited.

But the biggie is that this isn’t going to raise living standards from where we are now. Think on it just for a moment. Think on what the base problem is.

We currently identify emissions as an externality. Something which we do not include in the prices and costs that everyone faces. We’re also demanding that all of those costs should indeed be faced and paid. It’s probably right that this is so too. By hauling those externalities into a priced part of the marketplace we will, by our current measures of the economy, produce economic growth. Simply because what we count is priced economic activity.

But that simply is not the same as increasing living standards. Quite the opposite. We’re now demanding - again possibly rightly - that people pay for, now, what they used to be able to do for free. They, we, must now divert economic resources from whatever else it was we were doing to cover the costs of these new and non-emittive technologies. It’s also not true that these are, overall, cheaper. Not in terms of what is internalised in the current economy that is - for if it were all cheaper then we’d not have a problem, we’d all be doing it already. It also most certainly wouldn’t require massive subsidy nor sending cheques to Mr. J Foreigner.

Dealing with climate change is going to cost real money. Therefore it’s not going to raise living standards. QED.

Tim Worstall

After the Subbotnik comes the Vosekresnik

One of those little echoes from the gloried Soviet years:

The French senate this week passed a law that will force everyone to work for one extra day a year, with everything they earn going directly to the government. With its vast bureaucracy and a tax system that already squeezes 45pc of GDP out of the economy – and yet still can’t come close to balancing the books – France is on what the economist and philosopher Friedrich Hayek would have described as the “road to serfdom”. It is a terrible warning of the fate that will befall all of us if we don’t change direction very soon.

Ah, yes, that echo:

Subbotnik and voskresnik (from Russian: суббо́та, IPA: [sʊˈbotə] for "Saturday" and воскресе́нье, IPA: [vəskrʲɪˈsʲenʲjɪ] for "Sunday") were days of volunteer unpaid work on weekends after the October Revolution,

Once the authorities, the bureaucracy, find that they can force you to work for a day and then take everything resulting from your one day of work then the demands will not stop with just the one day.

And, you know, are we entirely certain that going down that Soviet path is quite what we want for our free and liberal society? Forced, unpaid, labour?

Tim Worstall

WWII did not grow the economy - discuss

It’s a commonplace that it was only World War Two that finally pulled the United States out of the Great Depression. Everyone went to work and that produced the economic growth etc. What a startling vindication of Keynesian demand management that is. All we’ve got to do is do whatever - a job guarantee, run the economy hot, industrial policy with strict conditionality - that employs everyone and all will get richer. Economic growth see?

This always does run up against the thought that here in the UK we solved the Great Depression in 18 months. We had expansionary austerity. Significantly loosened monetary policy by coming off the gold standard, cut government spending, produced a budget surplus and triggered a house building boom. It’s that balance between monetary and fiscal policy which defines the overall stance - it’s possible to use so much monetary policy that it overcomes fiscal austerity. Britain in 1939 was definitely richer than in 1931.

There’s also that point about the American experience that if it really were true, that only WWII worked, then all that faffing about by Roosevelt didn’t, possibly even was counterproductive.

But, just as a tease, what if the US was not richer in 1945 than it had been in 1939 (or ‘41 maybe)? Even, possibly, than 1929?

Yes, yes, it’s entirely true that recorded GDP, also GDP per capita, was higher. But is that really true?

Think on it. By definition GDP equals all production, all incomes and or all consumption. Any one of the three, by definition, equals either of the other two.

So, err, was consumption by the average USian higher in 1945 than ‘41 (or ‘39, ‘33, or ‘29)? If consumption wasn’t then is it really true to say that real incomes were? Probably not actually.

Sure, sure, we’re all agreed that US production rose mightily. But producing what the government wants to be produced (even leaving aside that it was produced to then be blown up) doesn’t, necessarily, seem to produce growth for the people.

Which is an interesting thought, no? To us the aim and purpose of an economy, even a civilisation, is that we the people get more of what we the people want. There’s an awful lot going around at the moment of we the people would be best served by government deciding what should be made, how, by whom and when. It’s not entirely obvious that the last time government did all the planning, decided upon the investments, had strategic plans with strict conditionality, that that did actually make us the people richer.

So, umm, what’s different this time? If 1939 to 1945 meant we all worked longer hours, on worse diets, travelled less, had fewer clothes, colder houses and all that - what is that evidence that government grows the economy and makes us richer?

The solution to that production = consumption = income = GDP thing seems to be that government can indeed increase production, even create full employment. But also while doing so demand the production of a lot of things with negative value in terms of income and consumption.

Oh.

No, no, we agree, beating the Nazis was a good thing. A Good Thing. but it didn’t make us richer so we shouldn’t use the episode as an example of government action making us richer, right?

And next time, heck this time, how do we know that producing what government insists is going to make us, the people, richer?

Tim Worstall

It’s Time to Start Using Development Orders

Last week, Angela Rayner seized control of plans for a new “garden town” in Kent, preventing Swale Borough Council from torpedoing the proposal. Residents were “gobsmacked” and “disgusted” by this central government intrusion. But, I say, good for her! Ange’s unapologetic takedown of entrenched blockers is a sight to behold. But, she could, and should, do more.

Much ink has been spilt over the UK’s broken planning regime but it's a crucially important issue. Over the last few decades, house prices and rental costs have skyrocketed. All the while, we’re failing to build critical infrastructure like reservoirs, forcing providers to draft farcical contingency plans to tanker water from Norwegian fjords.

Burdened by local vetoes and rolls of red tape, the UK’s planning system has devolved into a tangled bureaucratic quagmire, hamstringing our economic potential.

Despite widespread acknowledgment of the system’s manifold flaws, successive governments have struggled to overhaul it. Time and again, MPs and local authorities have buckled under pressure from their constituents, preventing real change. This is hardly a surprise, the current system rewards short-termist politicians who block developments and prioritise the needs of existing residents.

Although sweeping reform of the disastrous Town and Country Planning Act remains the boldest solution, we must face up to political realities. The Labour government’s recent planning proposals, while well-intentioned, show that they’re not prepared to tackle this behemoth head-on.

But YIMBYs take heart! There’s a solution hiding in plain sight - Development Orders.

Introduced in the Town and Country Planning Act of 1990, somewhat less evil than its progenitor, Development Orders are a little-known but powerful tool with the potential to ramp-up housebuilding. They empower ministers to grant planning permission for specific projects or entire areas, bypassing local authorities. Though I’m usually hostile to such top-down interventions, Development Orders serve as a necessary counter measure to the restrictive, state-mandated planning system that’s currently wreaking havoc on our housing supply.

Development Orders have already seen some limited success - facilitating home extensions and the development of film studios. However, their real power lies in their untapped potential.

With Development Orders, the Secretary of State could sidestep local and regulatory roadblocks, fast-tracking essential development. So, rather than waiting for their designation of grey-belt land to filter through the sclerotic National Planning Policy Framework, ministers could simply greenlight new housing and infrastructure in areas that fit their criteria.

They could also be used to create a bespoke regime where house building would be approved within a 10 minutes’ walk of any railway station. Adam Smith Institute research demonstrates that this would stimulate the construction of staggering 1 million more homes within the Green Belt surrounding London alone, unlocking ugly, unproductive land ripe for development.

Of course, Development Orders aren't purely vehicles for more housebuilding, they also restore a much-needed sense of stability. If a project meets the set criteria, it can move forward without fear of a council veto, opening the door for smaller developers. Currently, the housing market is so wildly over regulated that building anything is effectively banned. Only big businesses are able to navigate the existing morass of red tape.

In the hands of a courageous politician, Development Orders could transform the UK’s housebuilding potential, liberalising planning through the back door. Instead of getting bogged down in neverending consultations, politicians could simply pull this lever and get Britain building.

The UK’s planning regime is at the heart of the housing crisis - and much of our broader economic malaise. Ramping up the use of Development Orders would be a great first step to tackling this prevailing problem. After all, the state created this mess, so why not use the power of the state to fix it?

We’re all going to get so rich, aren’t we?

We have a new government fund - we’ve forgotten what it’s called but we’re assured that it’s really exciting - which is going to invest our tax money in the industries of the future.

But on Thursday night, at a court in New York, Northvolt’s lawyers filed for bankruptcy protection amid a cash crisis for the European battery champion.

More than just investing in those businesses of the future that are obviously going to work - for, of course, even dumb and stupid capitalists operating in markets can achieve that, hunh! - our tax money is going to be invested in those strategic industries of the future. Even, alongside strict conditionality!

Despite raising more than $15bn (£12bn) from investors, bondholders, pension funds and European governments since it was founded in 2016, this week the company had less than one week’s cash remaining – $30m.

We’re all gonna get so, so rich, right?

Tim Worstall

Luring humans works better than lashing them

Kingsley Amis said it about higher education but it works for governance too: More means worse.

Almost 1m under-25s are not in work or studying, new figures show, underlining the scale of the worklessness crisis as the Government plots a crackdown on benefits.

The number of young people who are not in employment, education or training – Neets – climbed to 946,000 in the three months to September, according to the Office for National Statistics (ONS).

It marks the highest number of workless 16 to 24-year-olds since 2014, and is up by 9pc from 871,000 a year earlier. The number of young Neets has risen by almost one quarter since the pandemic.

Recently we’ve had the cost of employing youngsters pushed up by significantly raising that youth minimum wage. We’ve been insisting for some time now that large scale youth unemployment is the very sign we need to show that the youth minimum wage is already too high. The recent budget also significantly increased the employer tax burden of employing young people. We’ve also had, effectively, the recent nationalisation of apprenticeships. Which has, to no one’s surprise at all, led to fewer apprenticeships.

So much for industrial policy with strict conditionality then.

At which point we’re no doubt about to gain more of that industrial policy - with strict conditionality - to solve the problems caused by the last bolus of it. The lashings of employers will increase until morale improves.

We insist that luring people into employing snotty youth works better.

For example, say we abolished the minimum wage. Teens could go to work and learn stuff in return for a sandwich and a bottle of pop at lunchtime. Employers could try youths out at that same price. Taxes upon employing such tryouts could be zero. Apprenticeships could be freed from the dead hand of the bureaucracy and undertaken upon whatever terms anyone wanted. Finally, we could simply abolish all out of work benefits for those under 24. We’re not wholly sure that even we agree with each and every one of those ideas. But we really are sure that if that were done then youth unemployment would pretty much vanish. Vanish by luring employers into taking the chance rather than lashing them for not.

Or, a little less controversial. Youth unemployment is currently caused by what government has already done. Rather than then asking government to do more to solve the problems it has, itself, created why don’t we run with the idea that government should stop doing the things that cause the problems that require solving?

And once we put it that way around why would we stop at youth unemployment as an area requiring this as a policy stance?

No government isn’t the solution, we are not anarcho-capitalists. But less government has a definite ring to it.

Tim Worstall

Advice to Howard Lutnik: Policy design should start with reality

Just a little note to one of those likely to take office in January. Policy design - on whatever - should at least start from reality. This is true of the business taxation system. Therefore we’d recommend that Mr. Lutnik, likely the next Commerce Sec, start with what actually happens.

Apple….”they make the parts in China, they put the parts together in Taiwan, then they wave their magic wand and it floats over Ireland….and then it comes to America and there’s a 3% profit in America….” and, well, no.

It’s more that the parts are made in Taiwan - processor and so on, by value the parts are made outside China - and then put together in China. By a Taiwanese company, Foxconn, often enough. Then Ireland and America, well, no.

For Apple has been very clear over the years, it runs its business in two segments. Outside North America is indeed run through Ireland, inside North America does not. The business of selling iKit to North Americans operates in terms of cashflows, profits, taxation and so on, exactly as a domestic US company. It’s entirely true that some other tech companies have - how to put this delicately - more interestingly complex tax and value structures. But Apple does not.

The effect of Ireland in Apple’s system is that tax which would, or could, be paid in the UK, Germany, Indonesia and all the rest concentrates in Ireland. Ireland makes no difference at all to the tax paid by Apple on its domestic, US, business - because it’s not involved.

As a result of the changes to the US corporate income tax from the first Trump Administration those profits that pile up in Ireland are indeed now taxable in the US. With the usual insistence that foreign taxes paid reduce the US tax payable. That is, the more Apple reduces taxation paid in the UK, Germany, Indonesia and so on, by that use of Ireland, the more US corporate income tax is due.

It’s entirely possible that the US corporate income tax system should be reformed. Our preference would be abolished but that’s because we’re ideologues. But any reform or management really should start from an acknowledgement of the current reality. Apple’s Irish tax structure makes no difference at all to the amount of tax Apple pays on its North American business. They deliberately set it up so that it wouldn’t too.

As a more general point, one of the reasons that politics so often fails to change the world is that politics so often doesn’t grasp the current state of that world.

Tim Worstall

The Agricultural Weasel Problem

Farmers say that around 70,000 farms will be affected by the restrictions on inheritance tax relief in Rachel Reeves’ Budget. The government and their cheerleaders say it will only be a tiny minority, just a few hundred.

Who is right, and how do they get such widely different ‘facts’? The answer I think is a combination of the difficulty of trying to govern by statistics, a sadly too common lack of understanding of how the tax system works in practice, and a bit of abuse of language, especially a little weasel word that is being loaded (deliberately or otherwise) with more weight than it can support.

The Government Line

HMRC statistics suggest that only around 500 farms a year currently claim the Agricultural Property Relief (APR) exemption from inheritance tax on over £1 million of assets.

Since APR will still be given in full on the first £1 million, they assume that only those 500 will pay the tax once APR is restricted.

And, as has been pointed out by the government’s supporters, possibly not even all of them will have to pay, because some clever tax planning can reduce that number further.

That is the basis of the government’s claim, much repeated by its supporters. At first sight it looks like it has a sound basis in official statistics, but look more closely and it starts to look more dubious.

Generations

The first point is that inheritance tax happens roughly once a generation, so 500 a year means there are around 15,000 farms that can be expected to have to pay the tax.

For them it will be a huge problem. A viable farm needs a lot of land, and land values (on which inheritance tax will now be charged) are very high, but farms make very low profits. The inheritance tax bill can therefore be completely out of proportion to the profits generated by the farm to pay it. And this matters; 85% of farmers own all or some of their land, with purely rented farms only a small minority, so almost all farms will be having to pay inheritance tax on land that has a high value but which they cannot sell without harming the business.

On some calculations therefore, funding each inheritance tax bill could wipe out the entire future profits for that generation. That is unsustainable, and so farms will have to be broken up or sold.

And of course it is the real working family farms that will be hit by this, while the small uncommercial ‘hobby farms’ will mostly be protected by the £1 million exemption.

But 15,000 is still a lot fewer than the farmers’ estimate of 70,000. Where’s the difference?

Out of Date Statistics

One problem of trying to govern by statistics is that they are always out of date.

The government’s ‘500’ claim comes from HMRC’s inheritance tax statistics, which of course are for those farmers who have already died. But if the average farm size is growing (as economic pressures and increased mechanisation mean larger farms are needed to sustain a viable business), that is unlikely to have fed through yet to the older generation who have been dying off and appearing in HMRC’s statistics.

And the statistics (yes, another set of them) do suggest that this has happened; since 2000 the number of farms has fallen by about a third, while the total area farmed has remained fairly constant, in which case the average size of farm has grown substantially. This will mean that a much higher proportion of current farmers will be hit by inheritance tax than would have been the case for those, mostly older, farmers who have died in the last few years.

Complex Relief

Another problem is a lack of understanding (even, it seems, in the Treasury) of just how complicated these inheritance tax reliefs are.

Just because someone has a farm does not mean that it was exempt from inheritance tax. The definition of what qualified for Agricultural Property Relief is so convoluted that a lot of farm assets, and a lot of the value, did not qualify. However there is another inheritance tax relief, Business Relief (‘BPR’) which covers businesses in general, not just farms, and has a different definition of what assets qualify.

Some farm assets qualify for APR but not BPR, some qualify for both, some qualify for BPR but not APR, particularly since farms have been encouraged to diversify. Land used for grazing for a horse livery business, for example, or a barn used for non-free-range chickens, or rooms let for Bed & Breakfast, are common farm business assets that are unlikely to qualify for APR but might, depending on the circumstances, qualify for BPR. And there are complex valuation rules for APR that mean, even where a field qualifies, its full value might not. Also farm equipment does not qualify for APR but might for BPR, an important consideration when a combine harvester can cost £1 million.

On most farmers’ deaths therefore, the inheritance tax return is a hodgepodge of different reliefs – APR, BPR, the residence nil rate band, and others. But the Budget reforms restricted APR and BPR together, leaving just a single £1 million threshold to be shared between the two.

Farms with more than £1 million of assets therefore will not all show up in the statistics as claiming more than £1 million of APR. A farm claiming £900 thousand of APR and £900 thousand of BPR, for example, would not be one of the ‘500’, but at £1.8 million would be well over the new combined threshold and would see nearly half its value hit by a costly inheritance tax bill.

So from those same government statistics:

The roughly 400 farms a year claiming £500,000 to £1 million of APR are highly likely to be over the £1 million threshold, once BPR is included;

Of the roughly 400 other farms a year claiming £250,000 to £500,000 of APR, it is likely that many will be over the £1 million threshold once BPR is included, although this will depend on the type of farm (with some more machinery-intensive than others) and location (as to how much of the land value qualifies for APR).

Even some of the nearly 500 farms a year that claim under £250,000 of APR could actually be over the £1 million threshold, once BPR is included, particularly if they have followed government advice and diversified into related businesses that, although still rural and probably farming-related, do not meet the strict tax definition of ‘agricultural property’.

So the government’s ‘500 farms a year’ could easily be 1,200, at a rough guess. That would be something like 36,000 farms over a generation, which is over half way to the farmers’ estimate of 70,000. But where are the others?

The Weasel Word

I think the other affected farms are being hidden behind that little weasel word, “affected”.

A lot of commentators, and HM Treasury, calculate the number who might have to ‘pay’ the tax, but then switch to referring to that as the number who will be “affected” by it. But the two are not the same.

Even if only 15,000 farms a generation will have to pay inheritance tax (and, as we have seen above, it is likely to be more than that), many more still will be affected by it.

This is because anything handed on while the older generation are still alive isn’t subject to inheritance tax at the time. It only becomes taxable if the donor dies within seven years. So long as ‘grandad’ (or whoever) survives seven years, there is never any inheritance tax, with or without APR, and so those farms won’t show up in the much-quoted HMRC APR statistics.

But even if they still don’t have to pay any inheritance tax under the new rules, they will still be affected by it because of that 7-year rule.

Currently the younger generation doesn’t need to worry about inheritance tax, because even if there is a death in 7 years, most of the value will be exempted by APR. But it won’t be under the new rules. Instead the threat of inheritance tax hangs over the farm for seven years, in case the older generation dies within that time.

So what does the younger generation do, having been given the family farm? Worry for 7 years, knowing that everything you’re working for may be taken off you to pay a tax bill? Take out expensive life insurance that the farm can’t afford? Cut back on essential investment to keep money back to cover the potential tax?

Even if those families still don’t have to pay any inheritance tax under the new rules, they are still affected by it, and a death at the wrong time could flip them into a tax bill that, after the Budget, could lose them their farm, home and livelihood.

Yes, there is all sorts of planning that can be done, and it is interesting to hear government figures suggesting tax planning as a way to mitigate the harshness of their own reforms. Lifetime gifts are common (although they are difficult; thanks to the ‘gift with reservation of benefit’ rules, the older generation will often have to entirely give up their livelihood and home to qualify); husband-and-wife lifetime trust schemes were used in the past and may come back into fashion (but they are fiddly to operate, split up ownership of the farm, and of course rely on being married with a still-living spouse); partnerships can start to pass some of the value to the younger generation while also getting them more involved in running the farm (but that has to be a genuine partnership, and you don’t have to listen to The Archers to see the potential for intergenerational disagreements there); some farms incorporate and hand on shares in tranches (but the additional APR restrictions on farming companies makes that difficult); etc. etc. But tax planning is complicated and there are all sorts of traps that the ill-advised can fall into.

More importantly, all of that comes at a cost - not just professional and legal fees but also changing plans, awkward split ownership structures, and the time and effort to plan, implement and operate complex arrangements.

Who is affected

All of these seriously affect those farms, and their families, even if they still don’t actually have to pay the tax and so aren’t included in the government’s ‘500’ statistic.

For some, the result will be 7 years of stress and worry. For others, 7 years of underinvestment as they save to be able to cover an inheritance tax bill that might fall on them. For others it will be costly legal fees and the strain of operating a complex structure – with the risk of a huge tax bill if you get it wrong.

But in whatever way, all of these will be affected by the Budget’s tax changes, many significantly so. The government, and expert commentators, who should know better, should not be ignoring that.

500 or 70,000?

So how many farms will be affected by the Budget changes? Trying to put some rough figures on it:

the government’s much-quoted ‘500’ a year is really 15,000 a generation;

the APR/BPR split can easily take that up to something like 35,000;

ongoing farm consolidation, making HMRC’s statistics out of date, could add, say, 20% to that, taking it to 42,000 farms that are likely to have to pay the tax;

then the many others who, through lifetime gifts and tax planning, do not actually pay the tax but are still seriously affected by the costs of doing so and the hoops they have to jump through to escape it; if a third of farms are taking proper tax advice, that takes the total to 63,000 affected farms.

These are only rough figures, but they make the farmers’ estimate of 70,000 affected farms, arrived at from different but respectable data, look very reasonable. Certainly the true figure is much more likely to be around the 70,000 level than it is to be just 500.

===========================================================

Richard Teather is a chartered accountant who, along with twenty years’ academic experience in tax law and policy, has advised businesses, business organisations and governments around the world.

The opinions expressed here are his own and do not necessarily represent those of any firm or organisation with which he is connected.

This blog post concerns the possible effects of tax reform and policy; it is not and should not be regarded as advice. Tax planning is highly complex and carries many risks, so should not be undertaken without specific, personalised advice.

If there’s going to be a trade war why don’t we be on our side?

Apparently there’s going to be a trade war. In which we’ve got to pick sides:

Britain would side with the European Union over the US if Donald Trump sparked a trade war with China, the Business Secretary has suggested.

Jonathan Reynolds said the scale of the UK’s trading with the bloc meant the Government would be required to “weigh the consequences” of any action that would create an “adverse relationship” with Brussels.

Mr Reynolds’s comments suggest the Government will prioritise appeasing the EU if Britain finds itself in the middle of a heated trade war once Mr Trump re-enters the White House.

Now, yes, this is as reported and one minister only and so on. So take with that correct amount of salt.

It’s possible to think that if there are only two sides why would we go with the wrong one of course. But rather more important. If there is going to be this trade war and we do have to pick a side why not pick our side?

As economist Joan Robinson suggested in her Essays in the Theory of Employment (1947), protectionist retaliation looks like the decision “to dump rocks into our harbors because other nations have rocky coasts.” One’s own government’s trade policy should not depend on the restrictions that foreign countries impose on their own citizens.

It is always useful to remember that, from the viewpoint of a country (this collectivist way of speaking being just a shortcut), imports are the benefits, and exports are the cost, not the other way around.

Our side, here, would be to allow those others to get up to whatever they want and to take the actions which most benefit us. That is, declare unilateral free trade and the rest of you can b’ggr off.

Think on it, think on it properly. Imports, our imports, are the things that we consume. They are those things which Johnny Foreigner can do better, cheaper, in a more timely fashion, even just more fashionably, than we can. Even if they’re subsidised, subsidised illegally even, that’s a transfer from their taxpayers to us in making those things better, cheaper etc. That’s why we buy them, doing so makes us better off than having to put up with wine made by the use of walls and glasses in Scotland. We, for our benefit, therefore do not wish to put barriers in the way of those lovely things that we can gain from Bourdeaux or other groupings of J Foreigners labouring away to make our lives better. We certainly don’t want to tax our own consumption of them. Well, not any more than we tax domestic consumption with a VAT or sin taxes - we don’t want to preferentially tax those imports that is.

Given that we don’t want to do that we shouldn’t.

Now note how politics works. If Washington DC, or Brussels, says “We are going to make our own citizenry poorer by denying them access to lovely Marmite” the correct response is not “And we’ll make our citizens poorer by denying access to macademias or merlot.” The correct response is “You do that then, see if we care.”

That is, we do not threaten Mr. Foreigner by throwing rocks in our own harbours. But politics seems to think we do - which is why politics is such a lousy way of running a place of course.

We have, in the past, drawn up a draft trade treaty:

What Johnny Foreigner does about this is up to them. For the only rational trade stance is unilateral free trade. So, that’s what we should do. Whether there’s a trade war or not we should be on our side - free trade and the politics of it can go to b’ggry.

As that final Parthian Shot, who is it that benefits from such restrictions and taxes upon imports? Those who own the domestic producers of the worse and competing products, obviously. We’re really quite adamant that taxing consumers to benefit the local capitalists is not a valid function of political or economic policy.

Tim Worstall

How Industrial Strategy Killed British Industry

“He is … led by an invisible hand to promote an end which was no part of his intention”

Adam Smith, Wealth of Nations, IV:II, p.456

Industrial strategy is back.

Just weeks ago, the Government published its green paper on Invest 2035: the UK’s modern industrial strategy.

“He is … led by an invisible hand to promote an end which was no part of his intention”

Adam Smith, Wealth of Nations, IV:II, p.456

I: The Return of Industrial Strategy

Industrial strategy is back.

Just weeks ago, the Government published its green paper on Invest 2035: the UK’s modern industrial strategy - “a credible, 10-year plan to deliver the certainty and stability businesses need to invest in the high growth sectors that will drive our growth mission.” Promising to channel support to eight ‘growth-driving’ sectors, and to engage on ‘complex issues’ such as energy prices, infrastructure, and planning, Invest 2035 aims to provide a comprehensive industrial strategy that is both pro-business and pro-worker, ‘open for business’ while also ‘shaping markets’. A tall order indeed. The consultation closes on November 24th, with the industrial strategy itself set to be published in spring 2025.

The Government’s announcement responds to increasingly loud calls to revive Britain’s industrial economy from across the political spectrum.

In 2012, Liberal Democrat Business Secretary Vince Cable argued that “the government shapes the British economy with its decisions every day…we can have an industrial strategy by default or design.” Giles Wilkes, of the Institute for Government, has likewise argued that “business has been confused, incentives towards long-term investment undermined, and key economic capabilities allowed to wither” by the lack of an industrial strategy. According to manufacturing advocacy body Make UK, “a lack of a proper, planned industrial strategy is the UK’s Achilles heel - if we are to not only tackle our regional inequality, but also compete on a global stage, a national manufacturing plan is required.”

The Labour Party set out its own proposals for an industrial strategy in 2022, entitled Prosperity through partnership: Labour’s industrial strategy. These proposals pledged to create a coordinated, cross-sectoral approach to industrial strategy, to put the industrial strategy council on a statutory footing, and to build a ‘more resilient’ economy.

The idea of an industrial strategy has found increasing purchase amongst Conservative thinkers too. In April 2024, Onward published A Conservative Economy, their case for a new approach to political economy. The report makes the case for a new ‘conservative’ political economy, which “[focuses] on reindustrialisation” in order to “build a more productive, resilient, and fairer economy”. Amongst the recommendations in that paper are calls to use fiscal and regulatory policy to support high and mid-tech manufacturing output, reforms to corporate governance regulations to channel more capital into UK equities and ‘productive output in the real economy’, and greater public investment in renewable energy technology and infrastructure. Rice and Timothy call for new oversight bodies designed to direct public investment into reindustrialisation, with ‘place-based regional economic development’ objectives and greater worker representation in corporate governance. The influence of trust-busting muscular marketeers like Theodore Roosevelt and Joseph Chamberlain looms large in this analysis, which presents itself as a repudiation of the economic consensus of the late twentieth century.

From left to right, the case for a new and more muscular industrial strategy has gained a serious head of steam in recent years - finally culminating in the Government’s Invest 2035 green paper.

And looking at the figures, it’s easy to see why. According to 2023 figures, about 16.9% of the UK’s GDP was produced by the industrial sector. That’s lower than G7 countries like Germany (28.1%), Japan (26.9%), Italy (23.1%), Canada (22.5%), France (18.7%), and the United States (17.7%) - though notably, it is not significantly lower than the French or American figures. It is also lower than other developed economies such as the Netherlands (19.4%), New Zealand (19%), and even Singapore (22.4%).

Figure 1: Percentage increase in GDP contributions from 1990 by sector, ONS

In absolute terms, the UK is the world’s eleventh largest manufacturing economy, behind countries such as South Korea, Mexico, and Brazil. In 2023, it was responsible for about 1.8% of global manufacturing output, lower than the 2.2% that it contributed to world GDP. Our production of substantial consumer goods like cars is even lower; the UK is the world’s 18th largest manufacturer of motor vehicles, behind countries like Indonesia, Iran, and Slovakia. The UK has almost no production capacity for critical modern technologies, such as semiconductors.

Closer to home, the picture isn’t much rosier. Back in 1970, manufacturing made up a full 32% of GDP. Michael Kitson and Jonathan Michie of the Royal Economic Society argue that the stagnation of the British industrial economy began in the early 1970s - between 1973 and 1992, the total increase in manufacturing output in the UK was just 1.3%, compared to 16.5% in France, 32.1% in West Germany, 55.2% in the United States, 68.6% in Italy, and 68.9% in Japan. Between the cycles of 1964-73 and 1979-89, the UK lost 2.5 million manufacturing jobs - one-third of the total, compared to just 10-13% in France and Germany.

And this trend shows little sign of slowing. According to analysis from the trade union GMB, the UK has lost almost 200,000 manufacturing jobs since 2010, constituting nearly 7% of the UK’s total manufacturing jobs. As of September 2023, just 7.1% of British workers were employed in the manufacturing industry, with a further 6.1% employed in construction and building. As of 2022, manufacturing contributes just 9.3% to UK GDP, falling below the wholesale and retail sector (10.4%); this proportion has declined precipitously since 2002, when manufacturing contributed more than 13% of UK GDP.

For many commentators, these statistics provoke existential dread about the poor state of the British economy. Alongside high-profile cases, such as the end of traditional steelmaking in Port Talbot (September 2024) and the closure of Redcar steel in 2015, there is a pervasive sense in some circles that Britain’s loss of industrial productivity represents a potentially terminal challenge for the UK.

After all, weren’t we once the workshop of the world? Whatever happened to the golden age of British manufacturing, when we were a proper country that built things? In comparison to service sector jobs, perceived by some as vague and insubstantial, careers in industry are widely valued for their tangible nature. This sentiment is perhaps best expressed by commentators such as the Telegraph’s Andrew Orlowski, who recently argued that “industry means prosperity, security, and self-determination”, asking whether British parents would prefer to see their children working “for Renishaw, Dyson, and Airbus - or Bet365?”.

In the cultural imagination, industrial decline is also tied intimately to the issue of regional economic inequality. The loss of jobs in major 19th and 20th century manufacturing centres, in places such as Lancashire, Yorkshire, and the West Midlands, is often identified as one of the key drivers of the UK’s relatively uneven economic geography. In a rhetorical sense, the ‘levelling-up’ agenda of 2019 to 2024 focused primarily on communities which had been ‘left behind’ by the process of globalisation and subsequent deindustrialisation. The idea of ‘bringing back industrial jobs’ is often used as a proxy phrase for ‘restoring economic prosperity to the regions’ or ‘making the economy less London-centric’.

Of course, not all of the arguments for a more muscular industrial strategy are cultural-historical in character. The UK’s declining industrial capacity presents legitimate security challenges - without the capacity to domestically produce primary industrial goods such as steel, Britain could be left vulnerable to shocks in global markets, and to predatory behaviour from bad-faith actors. Though not strictly an industrial issue, the sudden energy price shock of early 2022 was, in part, a feature of the UK’s relative dependence on energy imports. It is also true that the UK’s economy cannot run on services alone without incurring significant cost and significant risk - British people still need cars for driving, steel for building, and microchips to power their phones and computers.

At a time when major economic blocs such as the United States, China, and the European Union are retreating from the free trade consensus of the late 20th century, there are considerable risks associated with relying on the import of strategic or essential goods; for advocates of industrial strategy, this is proof positive of the need to onshore domestic production of these goods, regardless of cost. After all, can the costs of subsidising inefficient production of steel today really be outweighed by the cost of losing access to steel tomorrow? Though this essay will examine the global dimension of industrial strategy in further detail, it bears noting at this juncture that these are the strongest arguments in favour of reindustrialisation. It also bears noting that these arguments do not imply a particular process by which the UK should aim to improve the security of its supply of key goods - it is not per se an argument in favour of industrial strategy, and could equally serve as an argument in favour of improving UK competitiveness. The UK does need to think more carefully about its supply chains, but this fact alone does not necessitate or justify an enormous state-led industrial strategy.

Some proponents of reindustrialisation also argue that industrial jobs are inherently preferable to services-sector careers, believing that industrial jobs are more productive for the ‘real economy’. Pointing to stagnant productivity in the UK over the past few decades, they argue that the concurrent decline in industrial jobs as a share of our economic output is inextricably linked to our malaise.

The data behind these arguments is decidedly mixed. As of 2019, manufacturing jobs were recorded as adding £39.10 to the economy per hour worked - significantly more than jobs in sectors such as education (£29.90), wholesale and retail trade (£26.70), and accommodation/food-service (£17.50). However, it should be noted at this stage that manufacturing jobs were significantly less productive per hour than jobs in real estate (£292.90), financial and insurance activities (£63.90), and IT (£50.40). The most productive industrial jobs were, in fact, in mining (£163.20) and electricity/gas supply (£98.90). According to its proponents, a successful industrial strategy would encourage the UK’s financial sector to reallocate capital more efficiently, pushing investment towards high-productivity industrial jobs rather than to low-productivity services businesses, or other areas of the financial economy.

Figure 2: UK economic structure and sector productivity - manually transferred from ‘The UK Innovation Report 2022’, Cambridge Industrial Innovation Policy, University of Cambridge

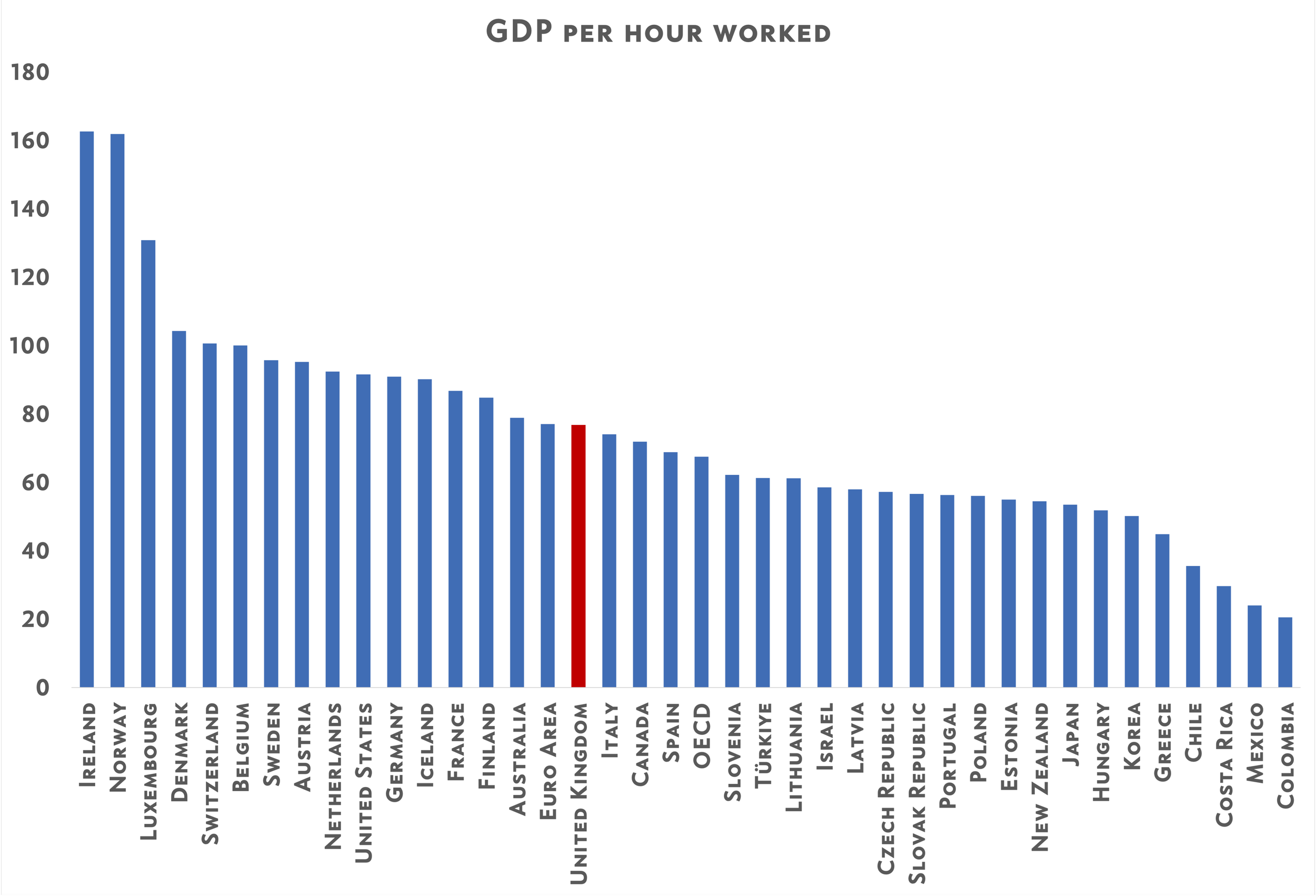

If this theory of productivity slowdown were true, we would expect to see a direct link between economic productivity and share of industrial jobs in our international competitors. In fact, there is no such link. The United States is comfortably the most productive G7 economy on a GDP per hour basis ($98), but its economy is sixth in the G7, in terms of proportional industrial employment. The UK is more productive than Italy, Canada, and Japan, despite having a lower proportion of industrial jobs. Labour productivity growth in the UK has not been significantly more sluggish than in other G7 countries, across a thirty or forty year timescale. Evidently, the Western productivity puzzle is about more than deindustrialisation.

Figure 3: GDP per hour worked (Productivity), OECD

Industrial strategy advocates also argue that, since industrial jobs are tied to production of tangible goods, they are inherently more secure or resilient - though it seems difficult to square this argument with the experience of mass industrial job losses in the 20th century. As this essay will subsequently demonstrate, industrial jobs are highly time-specific, and are disproportionately exposed to technological change.

Though the detailed prescriptions offered by advocates of industrial strategy vary widely, there are a number of core recommendations which unify these disparate calls. Most advocates of industrial strategy argue that, with or without a formal strategy, the UK Government’s policies will shape the fortunes of industrial businesses - and so a structured approach is preferable, affording more oversight and control to Government. Most argue that investment to the UK is both too low, and inefficiently distributed, generally as a result of uncertainty around government policy. Most argue that Britain should work to identify and promote industries in which it has some degree of competitive advantage, aiming to dominate or monopolise strategic parts of the global manufacturing supply chain. Most argue that industrial businesses and education providers are insufficiently aligned, meaning that the UK’s workforce is simply incapable of performing the kind of labour needed to sustain an industrial economy. Most argue that fixing all of these problems requires more state spending and more state intervention in the market.

Credit: Boris Johnson, Climate Ambition Summit 2020. Photo: Freddie Mitchell / No 10 Downing Street / Flickr / CC BY-NC-ND 2.0

Increasingly, proponents also argue that the process of achieving ‘net zero’ provides a ready-made pretext for reindustrialisation in the UK, arguing that a ‘net zero’ which relies upon imports from polluters such as China and India will necessarily be self-defeating. As such, the UK should, we are told, embrace the reindustrialisation possibilities presented by ‘net zero’s’ enormous infrastructural requirements, creating a raft of new ‘green’ jobs in the process. This is the logic which underpinned the ‘Green Industrial Revolution’ rhetoric of the Johnson Government, which pledged to create 250,000 ‘green jobs’ by investing in the UK’s domestic production capacity of goods such as wind turbines, solar panels, and electric vehicles.

II: UK Industrial Policy (2017-)

It is against this backdrop that the Government launched its consultation for Invest 2035: the UK’s modern industrial strategy.

Invest 2035 promises an “ambitious and targeted” industrial strategy, designed to drive growth by “enabling the UK’s world-leading sectors to adapt and grow, seizing opportunities to lead in new sectors with high-quality, well-paid jobs.” The green paper concedes outright that the Government will seek to shape the type of growth being pursued, and that the industrial strategy will also be used to “support net zero, regional growth, and economic security and resilience”, committing to both “long-term stability” and “reducing barriers to investment in the UK.”

It would be imprudent to rule on the success of the UK’s new industrial strategy at this early stage, but the terms of reference set out in the green paper should provoke concern.

Invest 2035 promises to focus on eight growth-driving sectors: advanced manufacturing, clean energy industries, creative industries, defence, digital and technologies, financial services, life sciences, and professional/business services. This is a curiously broad remit; few industrial strategies incorporate both financial services and advanced manufacturing. Its German equivalent, ‘A modern industrial strategy’ instead simply focuses on the country’s largest industrial sectors, as measured by turnover - automotive, mechanical engineering, metal processing, chemicals, electrical goods, and food processing.

Alongside Invest 2035’s focus on regional growth and net zero, there is a considerable risk that the resultant industrial strategy is unfocused and overly broad, shaped by political objectives as much as by sober economic analysis. It is nevertheless encouraging to see the green paper engage directly with planning and energy costs, as well as the importance of the private sector in shaping sustainable industrial growth. If it is to succeed, Invest 2035 should focus primarily on addressing the core economic barriers to industrial growth - explored later in this essay - remaining agnostic as to broader political objectives.

Those calling for a new industrial strategy might be surprised to learn that the UK has actually had an industrial strategy since 2017. In November 2017, Business Secretary Greg Clark unveiled ‘Industrial Strategy: building a Britain fit for the future’, a comprehensive industrial strategy designed to “drive growth across the United Kingdom, using major new investments in infrastructure and research to drive prosperity - creating more high-skilled, high-paid jobs and opportunities.”

Industrial Strategy 2017 pledged to make the UK “the world’s most innovative nation by 2030”, with £725 million of investment committed to the ‘Industrial Strategy Challenge Fund’, in order to address existential global trends. The plan identified four ‘Grand Challenges’; global trends which, it argued, would shape the future of the UK economy. These were, in no particular order, (i) the rise of artificial intelligence, (ii) the global shift to ‘clean growth’, (iii) the UK’s ageing society, and (iv) changing patterns in the way that people, goods, and services move.

It also committed to a series of ‘Sector Deals’ - ‘strategic, long-term’ partnerships between the government and industrial actors on sector-specific issues, “backed by private sector co-investment.” To take just a single example, the Government launched its Aerospace Sector Deal in 2019, designed to support the UK’s civil aerospace industry. The deal involved a £125 million subsidy for the industry via the Industrial Strategy Challenge Fund, the expansion of the National Aerospace Technology Exploitation Programme (with joint funding from both public and private sector), support for UK SMEs in the aerospace supply chain, and closer relationships between the aerospace industry and education providers, to ensure a pipeline of skilled labour for the industry in the years to come. Similar deals were struck on Artificial Intelligence (with the government document being co-signed by US-based tech firm, Facebook), the automotive industry, construction, creative industries, life sciences, the nuclear sector, offshore wind, rail, and tourism.

It promised to create a National Retraining Scheme - later integrated into the £2.5 billion National Skills Fund of the Johnson Government - designed to help people re-skill, alongside a £406 million investment into maths, digital, and technical education. Additional subsidies were pledged for the National Productivity Investment Fund, with plans to support electric vehicles, improve full-fibre broadband, and to create a new ‘transforming cities’ subsidy, designed to provide £1.7 billion of subsidies for intra-city transport.

Industrial Strategy 2017 is broadly in-keeping with most of the recommendations made by prominent industrial strategy advocates. It saw the Government identify high-growth-potential sectors, and design funding mechanisms designed to reflect their sector-specific needs. It involved creating closer links between education providers and industrial businesses. It saw the Government commit to long-term planning on supply chains, while working to drive R&D investment towards productive areas of the industrial economy. It provided a mixture of infrastructure investment, ‘skills’ investment, and direct capital investment, most of which was targeted at SMEs and gated behind competitive bidding rounds. At the time, the strategy was heralded as an example of how a more muscular state could shape the British economy post-Brexit.

And yet, seven years on, it would be difficult to argue that the UK has experienced an industrial renaissance since 2017. The broader political context around this must be acknowledged - the 2017-19 Parliament was dominated by discussions of the UK’s protracted exit from the European Union. Nevertheless, even as many of the key provisions of the strategy were implemented, the UK’s industrial economy continued to stagnate and decline.

In its election-winning 2019 manifesto, the Conservative Party pledged to “focus our efforts on areas where the UK can generate a commanding lead in the industries of the future - life sciences, clean energy, space, design, computing, robotics and artificial intelligence”, with reform of the Government R&D budget, support for the automotive industry, and investment in ‘skills’. Industrial Strategy 2017 was not mentioned.

By February 2020, a report from the Industrial Strategy Council accused the Government of neglecting the strategy - though the same report also acknowledged that the £45 billion in funding allocated to implementing Industrial Strategy 2017 was equivalent to 2 percent of GDP.

In November 2020, the ‘clean growth’ elements of Industrial Strategy 2017 were supplemented by Boris Johnson’s aforementioned £12 billion ‘Green Industrial Revolution’ plan, which promised to create 250,000 high-quality industrial jobs, “particularly in the Midlands, North East, and North Wales”, with investment into new renewable technologies.

And in March 2021, Industrial Strategy 2017 was folded into the Government’s ‘Build Back Better’ plan, which aimed to support economic growth “through significant investment in infrastructure, skills, and innovation”. Build Back Better was founded on much of the same logic as Industrial Strategy 2017, aiming to stimulate the economy through investment in skills and training, a new £375 million Future Fund, and two new schemes for SMEs. The biggest departure from the earlier strategy was Build Back Better’s emphasis on infrastructure investment, with promises of capital spending plans worth £100 billion. Like Industrial Strategy 2017 before it, Build Back Better promised to use this renewed industrial strategy to “level up the whole of the UK”, “support the transition to Net Zero”, and “support our vision for Global Britain”, putting these political objectives at the heart of an ostensibly economic strategy. The Build Back Better includes the UK’s decarbonisation strategy - ‘Build Back Greener’, which itself pledges billions in subsidies for ‘green industries’.

Once again, external events frustrated the implementation of this plan - namely the Covid-19 pandemic and subsequent lockdowns.

Credit: Prime Minister Rishi Sunak meets Secretary of State for Business, Energy and Industrial Strategy Grant Shapps, 2022. Photo: UK Government/ No 10 Downing Street / Wikimedia/ CC BY 2.0

In May 2023, the Sunak Government launched its National Semiconductor Strategy, which promised to grow the UK’s domestic semiconductor sector, safeguard the UK against supply chain disruption, and protect the UK against security risks associated with semiconductor technologies. The language should, by now, be familiar - ‘research and development’, ‘investing in skills’, ‘support for SMEs’. In November 2023, the Government followed the National Semiconductor Strategy with its Advanced Manufacturing Plan, pledging over £4.5 billion “in targeted funding to back the long-term future of the UK’s world-leading manufacturing industries - automotive, aerospace, clean energy and life sciences.” Presumably, the policies which comprise these two strategies will either be incorporated into Invest 2035, revised, or scrapped entirely.

Clearly then, the terms of references laid out in Invest 2035 are nothing new. This litany of part-implemented half-measures is by no means exclusive to the post-Brexit years, either. In fact, half-baked attempts to inject industrial jobs back into the British economy have been a feature of political life since the previous Labour Government (1997-2010).

In early 2010, Harvard’s Dani Rodrik declared that ‘industrial policy is back’, citing then-Prime Minister Gordon Brown’s openness to industrial strategy as “a vehicle for creating high-skill jobs”. In November 2012, then-Prime Minister David Cameron called for a “modern industrial strategy”; by September 2013, the Coalition Government was boasting that it had committed over £4 billion to industrial strategy, most of which was allocated through bidding rounds or invested in ‘skills’.

Time and time again, the same ideas have resurfaced, often prompted by lobbying from established businesses who stand to benefit from renewed political interest in providing material support to industry.

Previous industrial strategies have largely failed because they have asked the wrong questions; rather than trying to create an environment in which industry can flourish organically, they have tried to synthesise a Potemkin version of the imagined industrial landscapes of the early 20th century. They have been driven more by political considerations than by economic rationale. The scope of these strategies has consistently failed to encompass the root causes of the UK’s industrial decline, while the solutions offered have taken insufficient account of changing economic dynamics, both globally and domestically.

Too often, the Government has tried to pick winners (and losers) and direct capital, making short-term investments in individual enterprises rather than long-term investments in the UK’s business landscape. Certain core issues - energy costs, planning, regulation - have been largely ignored, in favour of a misguided economic orthodoxy which argues that successful industrial development simply requires more capital investment, whether public or private. Decisions have been unduly shaped by second-order political priorities, such as regional inequality or climate policy, and by poorly-understood buzzwords, such as ‘skills’ and ‘data’. All too often, rent-seeking for established industrial businesses has driven funding allocation.

It is an unassailable truth that the UK’s industrial economy has declined over the past few decades - but attempts to grapple with the core drivers of this decline have been few and far between. This failure has partly been driven by pervasive cultural-political narratives about industry. Too often, politicians have believed that reindustrialisation is a silver bullet, a straightforward way to address flagging productivity growth in the regions and win thousands of new voters in one fell swoop. For Conservatives in particular, industrial strategy and reindustrialisation prevent an attractive means to winning back disaffected voters in ‘Red Wall’ areas, many of whom are believed to distrust the Party due to Margaret Thatcher’s perceived role in 20th century deindustrialisation. According to 2019 polling conducted by YouGov, 34 percent of Britons believe that ‘overseeing the decline of mining and manufacturing’ was amongst Thatcher’s worst failings as Prime Minister.

Figure 4: Margaret Thatcher’s Greatest Failures, YouGov, May 3, 2019.

In fact, a sober consideration of Britain’s real industrial history demonstrates that attempts to direct industrial growth have typically failed miserably; our industrial economy has been at its strongest when it has been allowed to flourish organically, without reference to second-order political objectives. Despite what some commentators would have you believe, industrial strategy is not the remedy to Britain’s industrial decline - in fact, it almost certainly accelerated the process of decline in the first place.

III: A Brief History of British Industry

According to the prevailing cultural narrative, British deindustrialisation was set in train by Margaret Thatcher and her Conservative government (1979-1990). The narrative proceeds as follows: Thatcher’s Government withdrew support for flagship British manufacturers such as British Steel and British Leyland, and went to war with trade unionists who nobly tried to protect Britain’s industrial jobs. In some quarters, there is a belief that Thatcher and her government sought to reorder the British economy around the services industry for ideological reasons; in others, there is a belief that this process was largely a feature of globalisation and free trade, pursued fervently in the late 20th century and now regretted in the 21st.

Amongst most good-faith commentators, there is a broad acceptance that the status quo of the 1970s was unacceptable - but this acceptance is accompanied by a countervailing belief that the process of 20th century deindustrialisation was too deep, too sudden, and too harsh, damaging communities and unfairly punishing individuals employed in subsidised industries. Whoever is telling the story, the popular cultural understanding is that industrial decline was a deliberate policy aim, pursued in the late 20th century, and driven by a preference - whether pragmatic or ideological - for a more services-heavy economy.

In fact, the history of British industrial decline is far more complicated.

Far from beginning in the late 20th century, Britain’s relative industrial decline arguably began in the late 19th. After the boom years of the mid-19th century, Britain’s annual GDP per capita growth slumped to little more than one percent between 1873 and 1899, slowing to 0.84 percent up to 1914. Total factor productivity growth fell by two thirds between 1871 and 1914. This broader economic slowdown was accompanied by creeping anxiety about the risk of falling behind the United States and Germany, particularly where heavy industry was concerned.

Figure 5: US and Great British GDP per Capita (2011 International Dollars), Maddison Project 2022 Data Set

In 1903, the English economist Alfred Marshall wrote that “sixty years ago, England had leadership in most branches of industry. It was inevitable that she should cede much to the great land [the United States] which attracts alert minds of all nations to sharpen their incentive and resourceful faculties by impact on one another. It was not inevitable that she should yield a little of it to that land of great industrial traditions which yoked science in the service of man with unrivalled energy [Germany]. It was not inevitable that she should lose so much of it as she has done.”

Marshall, like many of his contemporaries, believed that Britain’s relative industrial decline in the late 19th century was the result of entrepreneurial failure - the sons of manufacturers had simply failed to innovate in the way that their fathers once had. Others, such as John Maynard Keynes, argued that capital markets had allocated resources inefficiently, investing excessively overseas. In 1913, 32 percent of British wealth was invested in overseas assets, particularly in the railway and utility bonds of emerging markets like the United States and Argentina. More recent economic historians, such as David Landes, have concluded that British education was at fault - unlike the United States and Germany, the story goes, British education was elitist, conformist, and insufficiently adaptable.

Failure to innovate, inefficient capital investment, insufficient investment in skills - sound familiar? The explanations offered for Victorian Britain’s relative industrial decline mirror exactly those advanced by contemporary writers reflecting on the failure of British industry to renew itself in the wake of late 20th century deindustrialisation.

In fact, these arguments have been roundly debunked. Writing in 1970’s ‘Did Victorian Britain Fail?’, the economic historian Deridre McCloskey hit back at the declinists. She demonstrated that financiers had no strong bias towards foreign investment (when taking into consideration dividends and returns), and that British firms did make efficient technical choices, with a competitive domestic market forcing out firms which failed to innovate. British education, meanwhile, was becoming more progressive and forward-facing rather than less, at the time of relative industrial decline; the Education Acts of 1870 and 1880 closed the primary education gap with the United States, and surpassed that of Germany. Britain had a flourishing system of apprenticeships and an expanding system of technical education.

So why did British industry lag behind the Germans and Americans? According to McCloskey, the answer was simple - by the early 20th century, industrial production was shifting to a system of vertically and horizontally integrated mass production, which suited the unique material endowments of the United States. Unlike Britain, the US had abundant natural resources and space, with reserves of petroleum, coal, iron, and copper which far outstripped those found in Britain. Even when accounting for Britain’s access to goods produced within the Empire, American production of these goods had outstripped British production by the end of the 19th century - and in any case, access to imported Imperial goods drove up production costs. However, despite the size and resources available to industrial businesses in the United States, the labour pool was relatively small, meaning that firms spent heavily on labour costs.

Analysis from economic historian Gavin Wright identified that, by 1913, the US had a comparative advantage in resource-heavy manufacturing; it was the world’s biggest producer of natural gas, petroleum, copper, phosphate, coal, and iron by this time, and its production of secondary and tertiary goods was reliant upon extensive, often inefficient, use of these deep reserves. Wright argues that the combination of abundant natural resources and a large, growing domestic market made the United States uniquely well-suited to the mass production culture of the early 20th century.

Britain, meanwhile, had fewer natural resources and a more elastic supply of skilled workers; her industry specialised around skill-intensive sectors reliant on the flexible production of customised outputs, such as shipbuilding, which relied upon high levels of experience, training, and expertise. With the largest and most cutting-edge industrial firms now overseas, British firms were slower to incorporate new technologies, and the positive effects of agglomeration declined.

The Great Depression was particularly punishing for British heavy industry. According to H.W. Richardson’s The Economic Significance of the Depression in Britain, Britain’s world trade fell by half between 1929 and 1933, while heavy industry fell by a third. From the beginning of 1929 until the end of 1930, unemployment had more than doubled, from 1 million to 2.5 million.

But the effect of the depression was uneven. The flagship industrial areas of the late Victorian era were hit hardest; in 1933, 30 percent of Glaswegians were unemployed, due to a severe decline in the city’s shipbuilding industry. Stephen Constantine’s Social Conditions in Britain: 1918-1939 estimates an unemployment rate of more than 25 percent in coal-producing areas of South Wales.

The production of export-oriented goods like coal, textiles, and steel fell steeply; in 1935, coal production in Lancashire was 43 percent less than it had been in 1913. In South Wales, this decline was 38 percent, in County Durham 27 percent, and in Scotland 26 percent. Between 1929 and 1932, ship production in the north-east of England declined by 90 percent; this, in turn, impacted supply industries such as coal and steel.

This severe industrial decline also provoked population decline, with cities across the north of England falling backwards from their early 20th century peaks. Liverpool’s population reached its zenith at the census of 1931, with 846,302 people living in the city. By 1961, the city’s population had fallen to 745,000. Changing population dynamics were prompted by a decline in demand for industrial labour, and government policy which aimed to clear the worst of the slums which had emerged in the urban areas of Victorian Britain.

The South and the Midlands, even in areas which relied upon industry, fared better. Industrial expansion in these areas focused on new developing industries, such as household electrical products and automobiles. The relatively strong performance of industry in these areas was also powered by a house-building boom which expanded the size of the available labour force in London and the south-east; the number of houses built by the private sector rose from 133,000 in 1931-32 to 293,000 in 1934-35, remaining steady until the Second World War.

Constantine estimates that, between 1932 and 1937, nearly half of all new factories that opened in Britain were in the Greater London area, as a result of both the city’s growing population and its increasing specialisation in robust, emergent industries. Cities with an established automotive manufacturing industry, such as Birmingham, Coventry, and Oxford, fared better than their northern counterparts, where production focused on more traditional industrial goods.

The Second World War prompted a complete reordering of the British industrial economy, around the needs of the wartime economy. In the post-war period, conceptions of British industry changed. In light of changes to the shape of the global economy, there was an acceptance in most quarters that British heavy industry and manufacturing should focus on quality rather than quantity. While Britain might not be able to compete with the sheer scale of American production, it had the capacity to produce high-quality, skill-intensive products in emergent industries. Combined with the formidable capital reserves of the City, and Britain’s prowess in other services industries such as shipping, British industry looked set for a modest revival.

Credit: Clement Attlee, 1945. Photo: Presumably Yousuf Karsh/ Wikimedia Commons/ Public domain

However, the acceptance of this new reality was complicated by politics, and particularly by the post-war Labour governments of Clement Attlee and Harold Wilson. The interventionist industrial strategies pursued by post-war Labour governments frustrated this revival. Instead, enormous resources were expended on sustaining failing, uncompetitive industries, and directing new development towards traditional industrial areas at the expense of emergent industrial centres.

To this end, the example of Birmingham is instructive; policy developments around the city’s mid-20th century growth tell the story of post-war British industrial policy in microcosm. As with other industrial centres mentioned previously in this essay, Birmingham grew rapidly, from just 8,000 people in 1700 to over a million in 1931. It was described by Harper’s Magazine in the 1890s as “the best-governed city in the world”, and by guidebooks of the 1930s as “the cradle of England’s industrial greatness.” Between 1923 and 1937, the city’s formal working population grew nearly twice as fast as the country as a whole, powered almost entirely by domestic migration.

The Greater Birmingham region was central to the Industrial Revolution, playing host to many of the period’s key innovations, including Watt and Boulton’s commercial steam engine. Between 1911 and 1954, the West Midlands grew its real output per person faster than any other region. Between 1954 and 1964, services businesses around Birmingham grew faster than in any other part of the country while in 1961, West Midlands households earned more on average than those in any other British region, including London and the South East.

Even as other industrial centres, in the North of England, South Wales, and Scotland, fell into decline, Birmingham remained strong. The city’s enduring success was partly driven by its adaptability, and its embrace of new industries. It was also driven by the city’s well-developed infrastructure, which included strong rail links to the rest of the country, and a developed network of canals.

Nearby cities in the Midlands fared similarly. A 1936 report from the League of Nations identified Leicester as the second-richest city in Europe, thanks to its diversified industrial base and lack of dependence on primary industries. Coventry was the fastest growing city anywhere in Britain from 1950 to 1965; in the 1930s, nearly two-fifths of its residents were from other parts of the country. In 1953, the city had an unemployment rate of just 0.8 percent.

Yet the Attlee Government saw the success of the Midlands as damaging to other regions. In 1945, it passed the Distribution of Industry Act, which aimed to push industrial development away from ‘congested’ areas in the Midlands, East Anglia, and the South East, and towards declining ‘development areas’ in the North, Wales, and Scotland. The Government took charge of the management of industrial estates, and required that the site for any factory of a certain size should be decided on by the Board of Trade.

Speaking in the debate on the Act, Walter Higgs (Conservative MP for Birmingham West) offered the following foresighted commentary: “We have recently had the experience of the aluminium industry being artificially diverted from the Midlands by the Board of Trade. It originally gravitated there because the machinery and the skill were there to produce what was wanted; diversion adds to the cost of production…the Bill may not have any detrimental effect immediately on such industries as we have in Birmingham and in the Midlands. That may come many years ahead. But we are probably sowing the seed for making them derelict areas in the future.”

In 1946, the Government commissioned the West Midlands Plan, which attempted to constrain Birmingham’s growth - local government was obliged to achieve a population target of 990,000, lower than the city’s actual 1951 population of 1,113,000. The Government was not only deliberately constraining the development of heavy industry in the city, but it was actively pursuing policies designed to make Birmingham shrink.

In 1947, the Town and Country Planning Act created the ‘Industrial Development Certificates’ system. Companies were required to obtain an IDC if they wanted to expand any industrial plant beyond 5,000sq ft in size; this gave central government further control over where industry could and could not be built. It in essence nationalised new growth in the economy. All of these controls made it difficult to regenerate businesses, or to add new ones; the Midlands economy became less diverse, focusing heavily on the motor industry - in turn leaving it vulnerable to the economic downturn of the early 1980s.

Credit: The home of Fox's Glacier Mints, 2015. Photo: John Welford/ Wikimedia Commons/ CC BY-SA 2.0

High-profile cases of Westminster refusing to permit the development of new factories in the Midlands were many and varied. In 1960, the Board of Trade refused Fox’s Confectionery permission for a new glacier mints factory in Leicester; the firm had been based in Leicester since 1880, and aimed to replace its existing factory, which faced demolition due to the Government’s plans to construct a ring road. Justifying the decision to Parliament, John Rodgers MP, the Parliamentary Secretary to the Board of Trade, argued that the planned move “could well take place elsewhere” and that potential expansion in Leicester “might tip the balance in favour of this city from Fox’s other factory in Belfast.”

Rodgers also conceded that, by 1960, the Government received very few requests for IDCs in London and Birmingham, “as it is well known by now that these will not be granted, not even extensions, save in the most exceptional circumstances.” He concluded that “wild statements by the Leicester Chamber of Commerce that Board of Trade policy will soon turn Leicester into a distressed area are ridiculous.”

It is perhaps worth reiterating that Leicester was recorded as the second-richest city in Europe, in 1936. Today, its unemployment rate is nearly double the national average (6.7 percent versus 3.4 percent), gross disposable household income is 28.5 percent lower than the national average and gross median weekly pay is 19.7 percent lower than the national average. Fox’s finally closed their operations in Leicester in 2019.

A 1981 study concluded that the Certificates had failed to work as intended. Of the certificate applications refused by the Board of Trade, only 18 percent relocated to a ‘development area’. Half of the refused projects were just reduced in size to avoid IDC control, while 31 percent of refusals led to closure, reorganisation, or abandonment. For every job successfully relocated by the IDC scheme, several more were destroyed or prevented.