Fire NIMBYs into the Sun

It has been reported that Liz Truss and the environment secretary, Ranil Jayawardena are going to end the distinction between 3A and 3B farmland— effectively banning solar panels from 58% of farmland in the UK. For someone who models herself on ‘growth growth growth’, this decision can only be described as bizarre.

There are several reasons why this policy is damaging to the UK’s growth prospects. When left to the free market, the decision between the use of farmland for solar or agriculture comes down to which option provides the farmer with greater profit. By removing this choice, the government is introducing inefficiencies. In some circumstances, farmers are forced into the choice which provides a lower return. Ultimately, this means the decision to effectively ban solar has a net negative impact on the productive capacity of the UK economy.

In the recent Mini Budget the most expensive policy was by far the ‘Energy Price Guarantee’, which in extreme scenarios could cost up to £140 billion. This works by capping the unit price consumers have to pay, while the government covers the difference. As such, a decrease in the market price of energy could have a significant impact on the price of the EPG and as a result the overall affordability of the Government’s (not so mini) mini budget.

With demand for energy likely to rise through the winter months and uncertainty about the situation in 2023, any boost to supply (putting downward pressure on the price of energy) could be a saving grace for the Government. Solar is quick to build, generally only taking a few months, and by some estimates is nine times cheaper than gas, although that figure is slightly inflated due to government price guarantees. Unlocking investment into solar energy should be near the top of the Government's priority list.

The cost of this policy suggestion goes further than the economics though. The Conservative Government committed to a fully decarbonised power sector by 2035 - requiring significant investment to replace the energy currently coming from gas, and other low carbon energy sources.

However it was estimated by the Financial Times that this policy would threaten £20 billion in investment from the private sector, corresponding with lost production of 30 GW of solar energy which could have reduced carbon emissions by 12 million tonnes. This is incredibly damaging to the environmental goals set by the Government as their initial forecast of a 5 fold increase to 70 GW now appears unlikely.

The policy also poses significant threats to the UK’s energy security. It was estimated by the Carbon Brief that 5 GW of new domestic energy supply could mean that the Government could cut UK gas imports by 2%. When adjusted to the 30 GW which is currently at risk, the UK could therefore cut gas imports by 12%.

So why does Liz Truss and the current Conservative Government wish to do this? The official line is that it would protect the UK’s food security. But 80% of the UK's food is already imported. It is estimated that even if solar is scaled up in line with the Government’s net zero target, it would still only cover 0.3% of the UK's land area, or 0.5% of farmland, less than the amount of land used for golf courses.

Solar panels can also be used simultaneously with agricultural practices creating agrivoltaic systems: shade provided by the panels can contribute to create a kind of microclimate, resulting in lower water requirements due to protection from evaporation, as such helping protect farmland from the biggest threat - climate change. Such systems have seen great success in Japan where there are nearly 2,000, growing more than 120 different types of crops. All things considered the Government's reasoning seems questionable at best and a tactical misdirection at worst.

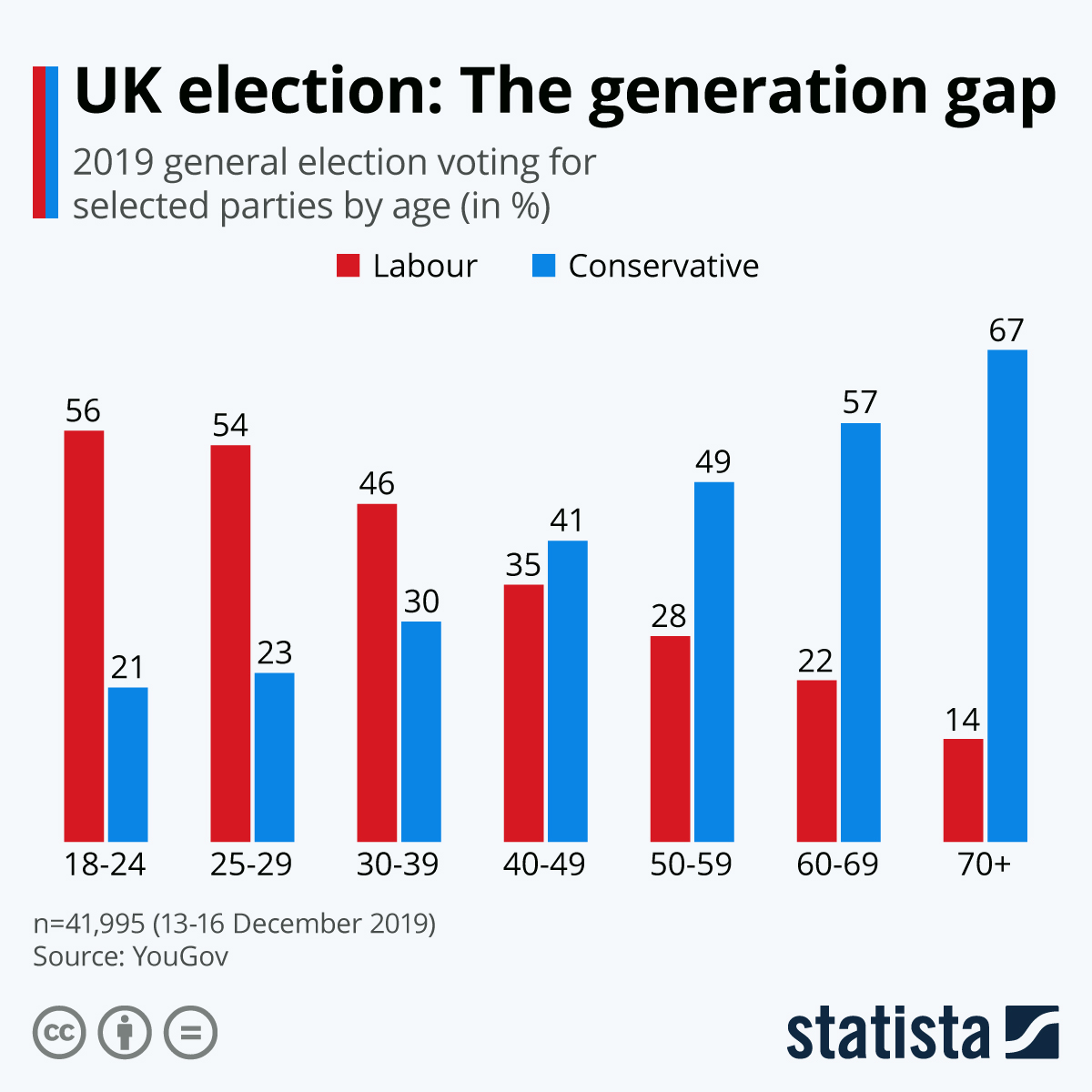

So why else would the Tories decide to ‘effectively ban’ solar panels across much of the British farmland? The problem is that a lot of the public find them unsightly: particularly older generations, who vote at higher rates and, more importantly, vote Conservative at higher rates. So this, as it often does, boils down to politics trumping economics. The Government is making decisions to try to appease their core voting base rather than taking decisions which are the best for the UK’s future energy security and economy. How pleased will pensioners be if they can't heat their homes because energy supply was curtailed in the name of pretty fields ?

{kind=link}

The Conservatives need to to throw out the silly notion that policy decisions should be based on trying to protect specific voter bases, and instead focus on trying to make economically sound decisions that benefit us all in the long-run.

There's a very, very, simple solution here

It could be that research and development is not concentrated in the right sectors, says Roger McKinlay, head of the government’s Quantum Technologies programme. “We need an industrial strategy, not just targets,” he says.

No, that’s not it, that’s idiocy. People who can’t choose who should be Prime Minister this week are not to be put in charge of what technologies should be developed over the next decade.

The Office for National Statistics has just admitted it has wildly underestimated private sector R&D spending, which it now reckons was £43 billion in 2020, almost 60 per cent more than thought. If true, this paints a very different picture. No longer a woeful laggard in this area, the UK is roughly average and slightly ahead of France.

But is it true? The ONS thinks its original numbers, derived from surveys, are less accurate than Treasury figures from R&D tax credit claims. Some economists are sceptical, suspecting that the Treasury numbers are too high because companies over-claimed.

We’d just remind of that Hayekian point, that the economy is really complicated, the centre never is going to know what’s happening so detailed planning is impossible.

But there is more here:

Many economists point to the weakness of all business investment, not only R&D. Spending on plant and machinery has been anaemic, despite the cut in corporation tax over the past decade. Yet for Britain’s services-heavy economy it is investment in intangibles that is increasingly key. And here too the figures are dodgy. The Bank of England said the “puzzling” weakness of UK investment data may be due to underestimates of spending on intangibles.

Investment is, by definition, spending that is amortised over more than one accounting period. That’s just what it is. Whatever is a simple cost in this period, right now, is a simple cost and current spending. Whatever is the buying of something that will be used over time is investment.

Which leads to two different observations.

Heard of SaaS? Software as a service? Microsoft Office or Microsoft 365? Same software, same usage, same producer same customer list- people have been migrating. Office is investment, you buy a licence and wait for the next upgrade cycle - a couple of years - to buy another. That’s amortised over the usage period, it’s investment. 365 is a monthly subscription fee. That’s current spending.

There’s more than just this Office thing as well. SaaS seems to be about $10 billion a year in revenue from the UK. $10 billion is an important number when we’re talking of £45 billion in investment. Yes, of course they’re slightly different things, the point is that measuring what is investment is difficult because it’s actually a rather arbitrary definition and tech is moving things across that divide.

This also being true in another sense. Write code these days and it’s considered very odd indeed to capitalise that. The cost of writing the code is - almost always - treated as a current expense, not an investment to be amortised.

That is, the more we invest in such intangibles then the less investment is actually counted as being investment. Again, this is not a perfect mapping, software and intangibles, but the point still stands.

The real answer here is not that the UK invests enough, too little, too much, is inefficient or efficient at doing so. It’s that we’ve no idea of even the number, let alone what it should be. Therefore we should stop faffing around with trying to tweak the number. On the very sensible basis that even all those really clever people who know how to kiss babies have no damn clue.

That’s the solution.

Is the UK in a Sovereign Debt Crisis?

The dramatic political reaction to former Chancellor Kwasi Kwarteng’s ‘fiscal event’ on 23 September was entirely predictable. Less predictable, however, was the scale of the fallout in the UK’s sovereign bond market.

Yields on gilts of every maturity jumped frenetically, with 10-year and 30-year borrowing rates rising by 0.7 and over 1 percentage points, respectively, in the wake of the announcements. The size of these moves led many financial and economic commentators to interpret them as a sign that asset managers and capital markets more generally were losing faith in the British government’s ability or inclination to continue paying its debt.

This view held that the size of Downing Street’s tax cuts – combined with the lack of any corresponding spending reductions, the existing borrowing commitments and the hollowness of the government’s growth strategy – had prompted investors to seriously reassess the default risk of UK government bonds.

Other observers, like Steven Major, head of fixed income research at HSBC, writes that the spike in yields was “not because there are serious questions about the creditworthiness of the UK government.”

Because the UK’s underlying borrowing capacity depends on a range of deeply uncertain factors, it is impossible to say with certainty whether perceived default risk is part of what initially drove investors to revalue UK debt. However, a key data point, as Bank of England veteran and National Institute of Economic and Social Research president Paul Tucker noted, is the change in the spread between yields on nominal and inflation-indexed or real bonds. Or rather, the lack of any discernible change.

For an investor to forgo protection from the possibility of unanticipated inflation eroding the real value of their bond before it reaches maturity, they’ll insist on a higher rate of return. This makes the gap between nominal and real yields a reliable measure of the bond market’s inflation expectations.

Under conventional assumptions about productivity growth, demographics and interest rates, the current path of UK fiscal policy is unsustainable over the long run. This makes a future debt default distinctly possible. Such a scenario would take one of two forms.

First, a future government might engage in a legal default, meaning it officially refuses to comply with the terms it agreed to when it initially issued its debts. Second, it could force the Bank of England to break from its 2% inflation mandate and engineer a period of unexpectedly rapid inflation, reducing the real value of the government’s liabilities and thereby transferring resources from bondholders to taxpayers.

This scenario, sometimes known as an economic or inflationary default, involves ‘fiscal dominance’, wherein monetary objectives become subordinate to fiscal objectives. It occurs when the debt-to-GDP ratio grows large enough that two of the government’s core macroeconomic objectives – low inflation, i.e. stability in the value of government liabilities, and debt sustainability, i.e. full nominal repayment of those liabilities – are no longer compatible.

The legal route is likely to be messier, more abrupt and significantly more damaging to the UK’s long-term economic prospects. As a result, a future government is much more likely to opt for the inflationary route. The implication is that if investors begin to lose faith in the treasury’s credit-worthiness, the initial signal will be a rise in inflation expectations.

An investor demanding a default-risk premium on nominal bonds without simultaneously raising their inflation expectations is one expressing near certainty that a future government would opt for the more economically and politically costly type of default. Such investors might well exist, given the recent rise in UK sovereign credit default swap rates, but they are rare.

Another important data point is the nature and effect of the intervention launched by the Bank of England on 28 September. For many, unconventional monetary policy operations, as Ricardo Reis puts it, possess a certain mystique. Central banks are sometimes seen as a sort of angel investor, able to draw on separate and perhaps deeper pockets than other parts of the government.

Central bankers have been in no rush to dispel this perception, and most of the time it’s not relevant. But when financial markets suddenly seize up, it can obscure the underlying accounting. Put simply, when a government’s borrowing costs rise because of an increase in perceived default risk, its central bank can’t ‘bail-out’ its treasury. The government’s budget constraint jointly limits both institutions’ financial capabilities; the central bank can purchase the treasury’s debt, but the Monetary Policy Committee borrows from commercial banks to fund these operations, by issuing interest-bearing reserves.

This matters, of course, because in a situation where a spike in bond yields reflects larger default risk, the Bank of England couldn’t reduce that risk simply by buying more of them. The only way to reduce default risk is for the treasury to succeed in altering market expectations about the size of future expenditures relative to tax revenues.

In the eurozone the European Central Bank represents member states collectively, and so its asset purchases can affect an individual member state’s default risk. But in a country like the UK with its own central bank, although the average maturity is important, the division of liabilities between the treasury and the central bank is irrelevant for debt dynamics.

Now, when the Bank of England announced its willingness to purchase long-term bonds on September 28, its role was that of a market-maker of last resort, as Walter Bagehot famously advocated in the mid 19th century. When the news broke, the reason yields immediately fell was that the spike was being greatly amplified by a serious liquidity shortage on the part of some of the largest holders of UK bonds.

The FT has some great reporting on this, but simplifying a little, the basic issue is that the pension fund sector relies on a pile of interest rate swaps to hedge against the risk that falling interest rates would raise the present value of their mostly long-term liabilities over their assets, some of which are much less sensitive to rate changes.

The former Chancellor’s announcements on 23 September raised market expectations about the path of the Bank of England’s policy rate due to higher expected aggregate demand, and more importantly, injected a lot of uncertainty into the trajectory of fiscal policy.

The ensuing rise in yields meant that pension schemes had to keep their swap positions collateralised, in the case of those operating through centralised clearing houses, using cash. To generate it, schemes began selling gilts.

Because the wave of selling was both sudden and sector-wide, this rapidly drove prices further down, which meant more collateral had to be posted, necessitating more selling. Liability-driven investment (LDI) strategies are nothing new, but their fragility pushed much of the UK’s pension industry into a doom loop, hugely amplifying the initial spike in yields.

Meanwhile, the widening of the bid-ask spread eroded some of the liquidity or ‘convenience yield’ on UK bonds, a significant factor behind many investor’s appetite for sovereign debt.

So, while the Bank of England’s offer was simply to swap one form of government liability for another, cash was what the pension sector needed to meet its margin calls.

Of course, a no less striking feature of the market reaction was the fall in sterling’s exchange rate against both a generally buoyant dollar and against the euro. Rising interest rate expectations, in isolation, would have appreciated the pound, but that effect was overwhelmed by the enormous uncertainty that the former Chancellor’s announcements had injected into fiscal and therefore monetary policy, sparking a flight into foreign currencies.

Other aspects of the market shifts since 23 September remain somewhat mysterious. The gap that has opened up between long-run government bond yields and long-run OIS forward rates, for example, has not yet been explained. Overall, however, from an investor’s perspective, the key thing the new Chancellor has to ‘deliver’ in his expedited announcements is concrete forward guidance on the trajectory of fiscal policy.

It's not the subsidies that are the problem, it's the lobbying for them

We are not, in general, in favour of subsidies. This is probably fairly generally known too. What is possibly less understood is why we’re not.

Yes, of course, subsidies are the government picking losers. Things that would not happen without baby kissing champions lavishing them with cash are things that probably shouldn’t happen. But what truly harms and costs is the competition to receive those subsidies:

The great hydrogen gamble: hot air or net zero’s holy grail?

An army of lobbyists is trying to persuade the government of the case for the combustible gas as a valuable weapon in the climate crisis, but questions remain

That army of lobbyists.

There are at least 120 paid lobbyists for hydrogen operating in parliament at present, according to estimates from the MCS Charitable Foundation. In the EU, a vast network of fossil fuel companies, trade associations and other interested parties are putting the case for hydrogen.

That vast effort to put the case.

Precisely and exactly because government has taken upon itself that power to subsidise - to pick losers - therefore there is this negative sum competition to capture those subsidies. Even, the permissions.

As it happens we’re very much in favour of hydrogen as part of the energy mix. If - and agreed, it’s an if - green hydrogen does become cheap then we’ve that climate change problem largely licked. Renewables through electrolysis to hydrogen to fuel cells solves the storage and battery problem. Green hydrogen combined with atmospheric CO2 then also solves - to the extent that fuel cells don’t - the automobile challenge, by producing synthetic petrol. And synthetic jetfuel entirely solves flying. That last already around and about economic as it happens. Cheap green hydrogen also entirely solves steel making emissions via DRI.

Sounds like a plan - except it shouldn’t be a plan at all of course. Not from government at least. For the government plan should be that here’s the problem - CO2 emissions - therefore any technology that solves that problem is to be treated equally. We would prefer by not being treated by government at all but at a minimum it should be that any method is treated the same. That is, it’s the result that matters, not the method by which it is achieved.

Because this process of submitting everything to politics as to method does indeed lead to the picking of losers - wood chip burning, E15 and all the other horrors - while also loading society with the costs of the scramble for those choices and subsidies.

We think hydrogen will in fact work for all the opinion of a few wonks matters. What we insist upon is that we must stop using political favour to either calculate that or encourage it. Instead use the one system we have that is absolutely and wholly fact based. If it works in the market then it works - so, leave the market to do the calculating. Any tipping one way or the other is by technology neutral and simple actions, not detailed planning.

The added advantage of this being that all those lobbyists would have to go get a real job, one that adds, not subtracts, societal value. Shame, eh?

We do not, for a moment, believe these wealth figures

The admirable Timothy Taylor has a piece looking at the racial wealth gap in the United States. We disagree, vehemently, with it. Not with what Taylor is saying, he’s outlining the current accepted wisdom. But with that current accepted wisdom. We’d probably want to mutter something about single parent incidence being an obvious enough thing to look at when considering inherited wealth for example. Something that none of this literature, to our knowledge at least, does do. Children who inherit from two parents are likely to have more wealth than those who inherit from one.

But our real disagreement is in the definition of wealth that is used in all of this literature. Which means that we disagree, vehemently, with this conclusion:

There’s a lot that can be said about all this, but I’ll limit myself to the obvious: Four decades–call it two generations–of no progress on the white-to-black wealth ratio is a long, long time.

We disagree that that is true.

Now, given what is measured it is true. But our disagreement is that what is measured isn’t the correct thing to be measuring. Wealth is measured as the stock of what can be sold off, for cash, over and above any associated debt. So, housing equity, private pensions provision and the two very much smaller categories of financial investments and personal possessions. That’s pretty much what does make up the wealth being considered. Those are, after all, the four groups that household wealth is normally broken up into.

We insist this is the wrong measure. The policy important - assuming that we are trying to craft some policy here - measure is a wider definition of wealth. Which we’d put at something like the ability to consume without having an income. No job, no labour income, yet still being able to consume - that’s wealth.

Now to be naughty and switch to UK figures - just because the Office for National Statistics does calculate this, in a way that Census, BEA and BLS seem not to.

Taxes and benefits lead to income being shared more equally in financial year ending 2021

In the financial year ending (FYE) 2021 which covered the first year of the coronavirus (COVID-19) pandemic, the median household income in the UK before taxes and benefits was £34,000, increasing to £37,600 after taxes and benefits. The richest fifth had an average income before taxes and benefits of £107,600, over 13 times larger than the poorest fifth (£8,200).

After cash benefits and direct taxes, the richest fifth of people had an average disposable income of £78,100, 5.9 times larger than the poorest fifth (£13,200). After considering all taxes and benefits, this gap reduced to 3.7, with average final income of £79,200 and £21,400 for richest and poorest people, respectively.

We often do calculate (as the Americans often do not) income inequality after taxes and those cash benefits. The point we insist upon is that it needs to be after all benefits. The NHS may not be the finest health care system in the world but the access of all to its ministrations is worth something. State schooling isn’t - Lord Knows - perfect but free at the point of use is worth something.

Given that those two - and many other things - are the ability to consume without a labour income then those are also wealth. Wealth being a stock which allows consumption without a labour income. So, given that healthcare, education - and many other things - can be consumed in the absence of a labour income thanks to the Welfare State then the Welfare State is a source of wealth.

Having made the point using UK figures we’d go on to point out that yes, the US does have a welfare state. They spend $trillions a year on it in fact. Everyone in the US does get healthcare treatment, for example. It’s healthcare insurance that’s patchy and even there the poor do get that too - Medicaid and CHIPS. It’s the poor to middling who fall into the insurance gap, even as turning up at any hospital in the country gains treatment. American schools are indeed free at the point of use. There’re Section 8 vouchers (largely equivalent to Housing Benefit) and on and on to including free cellphones for some - all the ability to consume without the possession of a labour income. They’re wealth that is.

Now, that the black part of the population relies more on the welfare state part of that wealth than the white does could indeed be an historical crime calling out for reparatory vengeance. But, we insist, it’s not actually a wealth inequality. Or, at least, wealth inequality isn’t as wide as portrayed, simply because things are already done to lower both income and wealth inequality.

To put this all another way. There are those who insist that we must plan society in order to make it better. Could be, could be, although we’d be willing to have a stand-up screaming match about even that assertion. But if we are to plan society hadn’t we best understand how it currently works, first? Work out how much actual income and wealth inequality there is before trying to change it?

And a third way to make the point. If we don’t include the effects of government policy upon the wealth distribution then how can we employ government policy to change the wealth distribution?

Solving budget problems - Cancel HS2 now

As has long, long, been pointed out the basic cost benefit analysis of HS2 is fatally flawed. The benefit is that those business class - first class - passengers get to their destination faster. That time saved is valued at their pay rate. An entirely normal manner of calculation by the way.

But that case contains the terrible flaw that we’ve invented mobile internet. Therefore time spent on a train is not valueless in terms of work done, the assumption made. In fact, given the interruptions of modern office life the time lost to Gavin announcing that the train will be departing soon is less, umm, interrupting than being in said office. Given the dependence of the HS2 numbers on that value of first class passengers’ time this blows that hole in that cost benefit analysis.

We can also do something entirely different and look elsewhere for guidance. Given that so many things do start in California, to then spread, their experience:

The infamous, $113-billion-and-counting California high-speed rail line between San Francisco and Los Angeles, which was supposed to be completed by 2020 for a cost of $33 billion yet has only begun tinkering on a 171-mile stretch in the Central Valley, is not really "an existing project," says former California High-Speed Rail Authority (CHSRA) Chair Quentin Kopp. "It is a loser."

Added ex-chair Michael Tennenbaum: "I don't know how they can build it now." And California State Assembly Speaker Anthony Rendon (D–Lakewood): "There is nothing but problems on the project."

Quite. Given that California is indeed providing that experience of the future to us we really should be taking note.

Government needs - so it says - to find significant savings in spending currently. Great, cancel HS2. It always was a dog of an idea and it’s time to put it down.

We can even approach this in a third manner, one that’s wholly, exactly and entirely conclusive. Back 12 years George Monbiot was able to spot the economic flaw in the plan. And let’s be serious about this, wholly, exactly and entirely. If even George Monbiot can spot the error in your economics then you’re really howling at the Moon.

Save money, kill a train set today.

No, a public information campaign is not 'nanny-statism'

There seems to be a common misconception that free-market neoliberals must be firmly against the idea of a public information campaign on saving energy, on the basis that this is pure nanny-statism. In fairness, this is a view which has been propagated by our Prime Minister, who is said to be ‘ideologically opposed’ to the idea, and the Minister for Climate, who reminded Sky News that they are ‘not a nanny-state government.’

It’s worth quickly setting out here why they are wrong- and why Liz Truss’ announcement at PMQs this week that BEIS will be looking into a public information campaign after all is welcome news.

Information Campaigns are not a symptom of a nanny-state

It’s hardly a secret that the Adam Smith Institute is no fan of the nanny-state. Fundamentally, the nanny state materially impacts the ability of individuals to make choices. However, it is not nanny-statism to offer public advice. In fact, one of the central principles of a free market economy is that consumers should be fully informed in order to make decisions which are most appropriate to their individual needs.

2. It makes economic sense

Another criticism of the proposed information campaign is that £15 million is a waste of taxpayer’s money, which could be better spent during a cost of living crisis, a view exemplified here by Maria Caulfied. Whilst it is fair to question where taxpayer money is going, this misses a key point. Household energy bills are being subsidised by just under a third, at cost of approximately £150 billion. The public would not have to reduce their energy consumption by much in order for the information campaign to save the Government money. Anyway, compared to £150 billion, £15 million is hardly a small drop in the ocean.

3. It will help people to reduce their energy bills

There are surely few people who believe that Brits aren’t sensible enough to cut back down on their energy consumption. However, the Government’s communications around the energy price guarantee have been woeful. On her now infamous local radio round, Liz Truss asserted that no-one will be paying over £2,500 for their energy bills- when in fact the energy price guarantee is simply a price cap by another name, meaning that the typical household bill will come to around £2,500. At the end of September, polls suggested that two in five households thought that the guarantee prevented bills from going over £2,500 and the Government has done little work to correct this.

4. It is necessary to prevent blackouts

As many free-marketeers have been at pains to point out, one of the principal problems with Liz Truss’ energy subsidy scheme is that it has distorted the price signal. Freezing energy bills at a lower rate has created an artificial price signal for users, reducing the incentive to reduce consumption to a level optimal to prevent energy blackouts this winter. Moreover, considering that well-off households will be getting the largest subsidy and will be using the most energy, reminding them that, even if they are financially cushioned from the energy price rises, they still have a part to play in preventing blackouts is surely sensible.

Tsk, see, we can't rely upon altruism

Not that we’d want this to be taken entirely and wholly seriously:

Hospitals have been told to cancel thousands of operations as blood supplies threaten to run dry.

After years of rejecting donors, NHS Blood and Transplant (NHSBT) issued its first ever amber alert status on Wednesday - meaning there are just two days of some types of blood supplies across hospitals in England.

The agency asked all existing donors who are types O negative or O positive to come forward and book an appointment to give blood.

But if this were a paid market - say, energy, food, trains, housing - then you can imagine the calls that this must be removed from being a paid market and made something different, reliant upon government or altruism or summat.

Because any stutter in a paid market always does lead to such calls. So, here we've an altruistic market which has a stutter - logical fairness requires us to insist that it can no longer be an altruistic market, right?

The not seriousness of the comment - except as a logical point - is that we've actually tried paid and altruistic markets here. At least, the US has. And the voluntary donations vastly outcompete the paid ones for whole blood. The consumer preference is overwhelming. So, altruism in whole blood it is then.

Not because there's any a priori proof that this should be so. Or that paying for whole blood is immoral - despite what many will say. But because we used the market system properly. To test, try out and find out which arrangements do work.

That is, we use that free part of free markets to find out whether cash on the nail markets work here. That use leading us to the finest solution we have in these specific circumstances. Which is the part that does need to be taken entirely and wholly seriously. This whole concept of free markets is, in one way of looking at it, a method of evidence gathering and decision making. At the start we don’t know. So, what is our method of finding out?

The value of using this method rather than - say - some insistence that money and body parts must not be mixed is that a purely altruistic system for blood products does not work. Certainly, as the continuing scandal over haemophiliacs and HIV infections shows, a paid market can have its problems here. But there is no country that successfully relies upon an altruism only collection system for blood products like plasma. Everyone, but everyone, relies at least in part upon a payment to the donors system - largely the US one.

That is, without the cash based collection system people die for lack of plasma. We can even go on to think that this is less effective than an altruism based system. Or that voluntary donations of plasma lead to higher quality - as with whole blood. Even, that it’s still immoral, money for bits of humans - as long as we’re willing to accept the cost of that moral imposition, death for some.

Again, this is the value of the free part of free market. We’ve two very closely related products and markets here, whole blood and plasma (or blood products, if preferred). In one altruism outperforms cash. In the other cash creates the supply that altruism doesn’t. And that’s the value of that free part. Without actually trying this out we’d not know that, would we? And we’re now able to manage our world because we do know.

Having plucked the logically important part out of this of course the lesson is of wider import. Only one country in the world has payment for kidney donation. Only one country doesn’t have a queue of people dying while awaiting a kidney. It’s possible to supply a part of your liver and recover just fine - as is the person it’s implanted into likely to recover just fine. Gametes, surrogacy, can be both donated and bought - well, which system actually works, in the sense of producing the optimal, even maximal, amount of bouncing babies?

Shouldn’t we find out, rather than allowing the self-appointed to determine our morals for us? After all, once we have found out then at least we’d know what those morals are costing us. Or even, what their morals are costing us.

It's too little free market, not too much

That perennial whine, housing and rentals. We’re told that:

It’s the crisis Thatcher built. It started with the “right to buy” in 1979, which eviscerated the country’s social housing stock. It was followed by Tony Blair’s private finance initiatives, or PFIs, which fragmented local services. And it has been compounded by austerity, which finished local services off. The result of 40 years of free-market extremism is visible all around us: in tent cities, food banks and record-breaking numbers of homeless deaths, which continue to rise every year. Meanwhile, private landlords swim in cash.

The problem here is not enough free market extremism, not too much. We have a national plan for how much housing should be built. We have very strict limitations on who may build what where. We’ve lines on the map insisting that no one at all can build houses Britons want to live in - the absurd idea of minimum density at 30 per hectare - anywhere near where Britons actually want to live - the Green Belt.

These are the reasons that housing is expensive in Britain. For the cost of building a house is very much the same as it is anywhere else. In the £120k to £150,000 for a nice little 3-bedder. All of the rest of the price - and this can be checked by looking at how much the insurance company will pay out if your house were to suffer a sudden dematerialisation event - is the scarcity value not of the land even, but of the pieces of paper that allow you to build a house on a specific piece of land.

So, the solution is to issue more pieces of paper. As with the way government issues money itself: print more, each piece is worth less.

The Conservative party are already subsidising people’s housing costs through housing benefit, much of which is paid into the pockets of private landlords. Wouldn’t it be more efficient to spend that money on building long-term, affordable social housing, rather than empowering landlords who have no interest in meeting the needs of the poorest renters?

It would in fact be more sensible to go all free market in a properly vicious and regulation slashing sense. Blow up the Town and Country Planning Acts 1947 and successors. Proper blow up, kablooie.

Force suppliers - landlords - to chase consumers - renters - just as Tesco, Morrisons, Waitrose, Aldi and the rest have to chase our custom for their baked beans. A proper free market will have prices at around the cost of production of the marginal unit or so. Because that’s how markets work. Second hand will be cheaper as that’s also how markets work.

The solution to the fundamental problem in the British housing market is, at bottom, not to try and tone it a bit with some twerking here and there, it’s to get all Adam Smith on its arse. Viciously so.

Kablooie.

The Department for Health Insanity

We all know how profligate the government can be with our money but this item coming right after a mini-budget calling for spending cuts is not without irony. The Department for Health and Social Care has just announced it will finance £50M on research into health inequalities. £50M on doing something about them might be excusable but giving £50M to academics to find the answers we already have is just throwing our money away. For starters, the DHSC could look at Scambler (2011) and Thomson et al. (2006)

Don’t get me wrong. Many local councils are impoverished and bunging them the occasional £50M is no bad thing, especially as the DHSC does not seem to need it. But they should be sent the money to spend on what they are good at – social care for example – not something for which they have no relevant skills whatever. No less than 13 local authorities will get about £4M each to do their own things: there will no learning from each other. Instead “every collaboration will be set up in partnership between universities and local government, capitalising on the world-leading experience and skills of the academic community.” We do not know how the 13 were chosen but it seems unlikely that the 13 universities in question are all “world-leading” in this particular field.

Of course, when they have spent the £50M on research, there will be no money left to do anything about the findings. Another £50M on adult social care or persuading NHS doctors to remain in post would have been money really well spent.

The announcement is unclear whether the £50M comes from the National Institute for Health Research (NIHR) or the DHSC itself. The NIHR has not got around to publishing an annual report since their 2019/20 one. They spent over £1bn on a miscellany of UK research projects plus £120M overseas. In addition, the Medical Research Council spent £886M, including £19M overseas, in 2021/22.

I have no idea how much the UK, or England, should spend in total on medical academic research nor how they make their decisions nor what methodology for decision-making has been shown to be the most productive. I am pretty sure the NIHR and MRC do not know the answers either because, if they did, they would tell us.

I was once involved in an application to the MRC for research support. About a year later they turned us down on the basis that the research could not possibly work, i.e. it could not be done. Luckily, we had got the money from somewhere else and it had all worked out fine.

These two bodies should be merged and introduced to the real world.